Geopolitical oil shocks have a long track record of rattling equity markets, and the current episode is no exception. With the S&P 500 already down around 6% since the latest Iran-related conflict escalated, investors are watching closely to see whether history repeats itself, and which version of history that turns out to be.

Oil Shocks Have Pushed the S&P 500 to Extremes: -30% or +30%

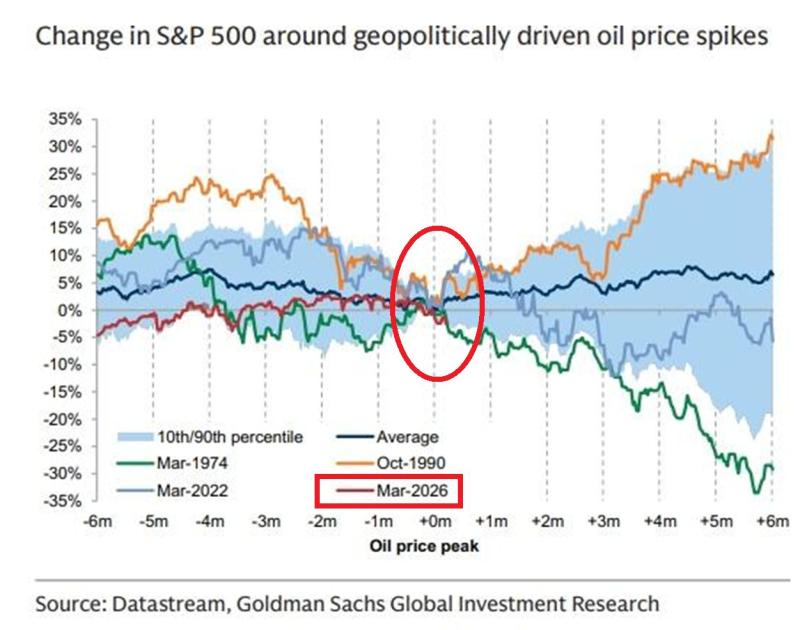

The current move tracks near the historical average for geopolitically driven oil shocks, but the range of possible outcomes is wide. The S&P 500 is down roughly 6% since the conflict began, landing close to the midpoint of past cycles. That average, however, masks dramatically different scenarios. During the 1974 oil embargo, the index dropped close to 30% over six months as stagflation embedded itself into the economy. The 1990 Gulf War produced the opposite result, with equities rallying nearly 30% once oil prices normalized.

Why the 2022 Russia-Ukraine Conflict Still Matters for Today's Outlook

The 2022 Russia-Ukraine war offers a more nuanced parallel. The S&P 500 initially held its ground but eventually declined as inflation proved stickier than expected. That episode reinforced a key lesson: it is not the oil shock itself that drives long-term equity damage, but how long elevated prices persist and how deeply they feed into broader inflation data.

Today, the S&P 500 sits near its historical average response to oil price peaks, suggesting the market has not yet committed to a directional break. A rapid pullback in crude would likely stabilize equities, while a sustained elevation in energy costs could reignite inflation fears and push the index into more negative historical territory. The resolution of current geopolitical tensions and their effect on global energy flows remains the central variable for the months ahead.