Artem Voloskovets

Artem Voloskovets

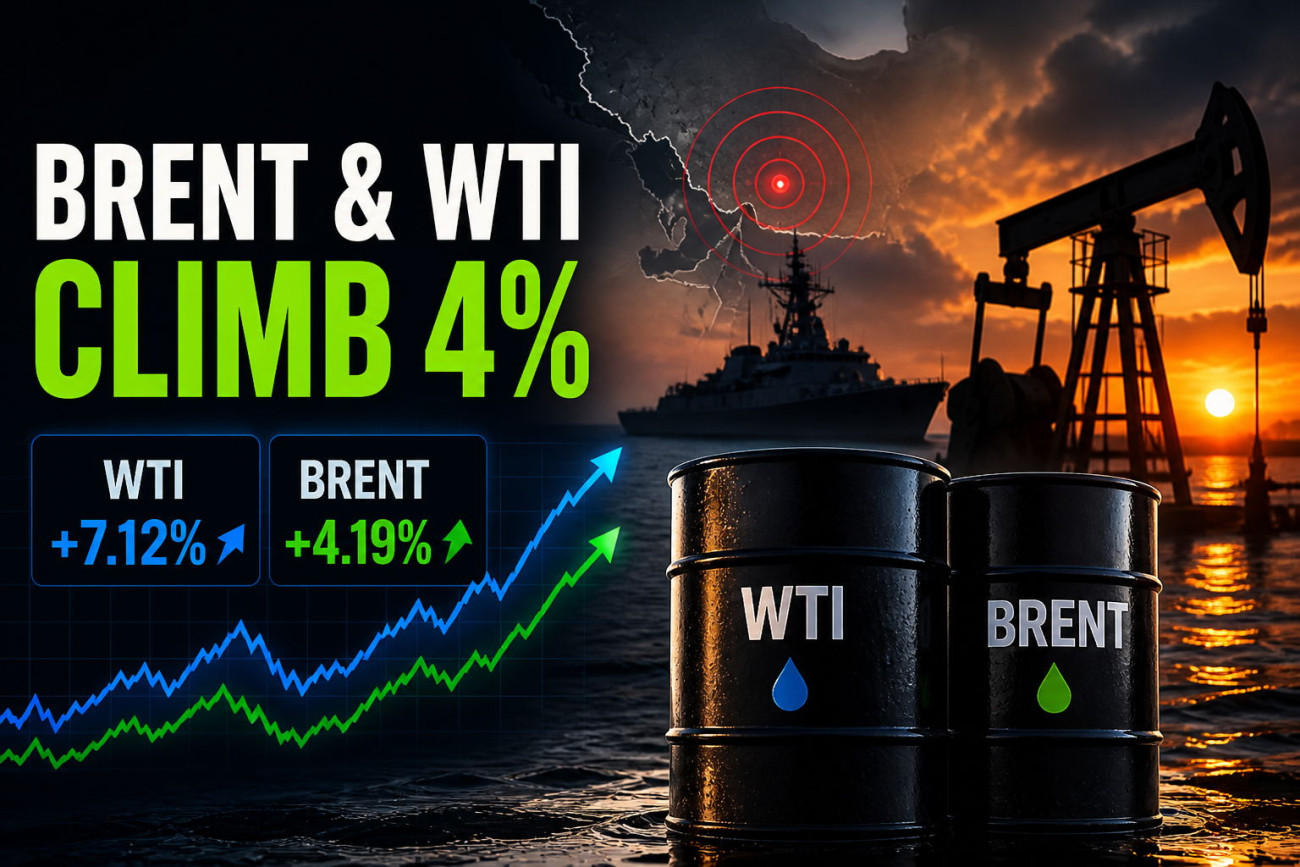

If you look at the raw data alone, the move is already significant. U.S. gasoline has climbed to $4.46 per gallon, up from $2.98 before the conflict, while diesel has surged to extreme levels, reaching over $6 in some regions. According to recent reporting on fuel price trends, the current price environment reflects both supply concerns and rising market anxiety.

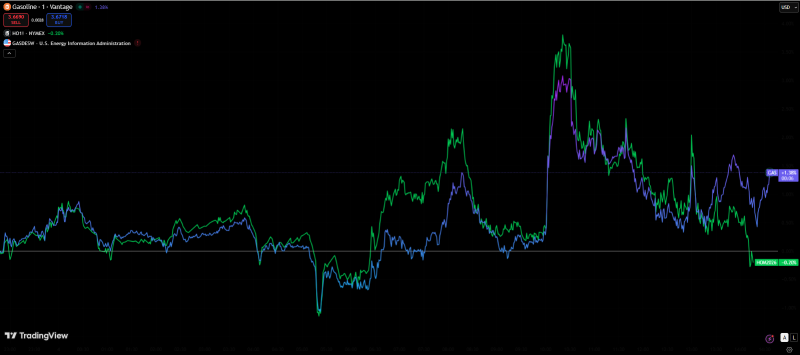

But those numbers don’t fully explain what matters most right now - how sustainable this move is. That’s where the chart becomes critical.

What the price action shows is not a slow, steady climb. Instead, we see sharp, almost vertical spikes higher, followed by unstable consolidation rather than full retracements. Prices don’t return to previous levels - they pause, fluctuate, and then attempt to push higher again. This kind of structure typically appears in the middle of a move, not at the end. It signals a market that is still searching for a new equilibrium, but already accepts that the old pricing regime no longer applies.

That dynamic makes sense in the context of Hormuz. The strait is not just another geopolitical headline - it’s a physical bottleneck through which roughly 20% of global oil flows. Any credible threat to its operation immediately adds a risk premium to energy prices. Markets don’t wait for actual supply shortages; they move on the probability that disruptions could occur. As highlighted in coverage of the Strait of Hormuz risk scenario, even partial disruption is enough to move global oil benchmarks sharply.

This is exactly what we’re seeing. Even after pullbacks, prices are holding higher levels, and dips are being bought. That behavior suggests participants are pricing in a scenario where the disruption is not resolved quickly. Efforts to stabilize the situation, including initiatives to secure shipping routes, have so far failed to shift that expectation. The market simply isn’t convinced yet.

Diesel’s outperformance reinforces this view. Unlike gasoline, diesel is tightly linked to freight, agriculture, and industrial activity. When diesel prices rise, the effects ripple through supply chains almost immediately, pushing up the cost of goods and services. In that sense, current diesel levels are not just a fuel story - they are an early signal of broader inflation pressure.

When you combine the data with the chart structure, the conclusion becomes clearer. The $5 per gallon level, which marked the peak in 2022, is no longer an outlier scenario. It is increasingly becoming a realistic target if current conditions persist. Analysts have already warned that prices could revisit or exceed that level if the Strait remains constrained, as noted in analysis on potential $5 gasoline scenarios.

What happens next depends less on traditional supply-demand metrics and more on timing. If the situation in the Strait resolves quickly, prices could unwind sharply, just as they rose. But if uncertainty lingers for weeks, the current trajectory makes a move toward $5 gasoline highly likely.

The key takeaway is simple: the market is not trading facts - it is trading scenarios. And right now, the dominant scenario is one where higher energy prices are not temporary, but part of a new baseline.

Artem Voloskovets

Artem Voloskovets