Artem Voloskovets

Artem Voloskovets

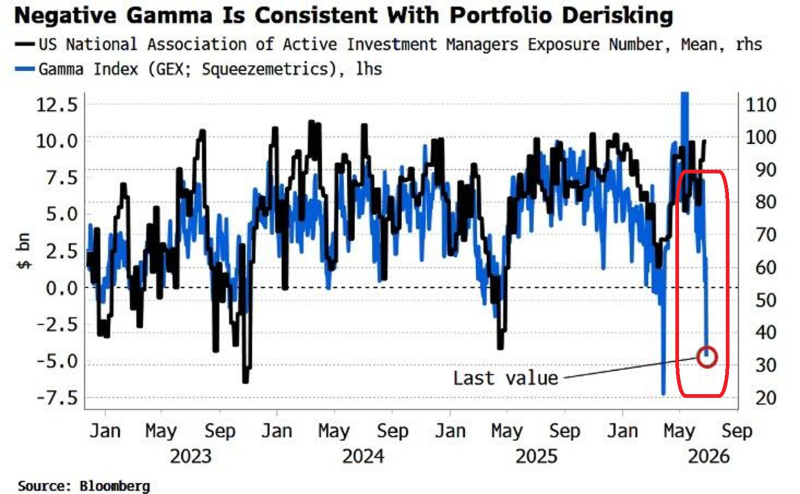

One chart captures a shift that isn't obvious from headline index performance. The NAAIM Exposure Index climbed to 98.59 on June 24, showing that active managers have largely rebuilt equity positions after the spring pullback. At the same time, Gamma Exposure (GEX) has fallen back to roughly -$5 billion, moving dealer positioning into negative territory.

The market is no longer driven by a single story. Investors remain heavily invested, while the options market is becoming structurally less stable. That divergence matters because positioning and market mechanics now point in opposite directions.

Investors Are Already Near Maximum Risk

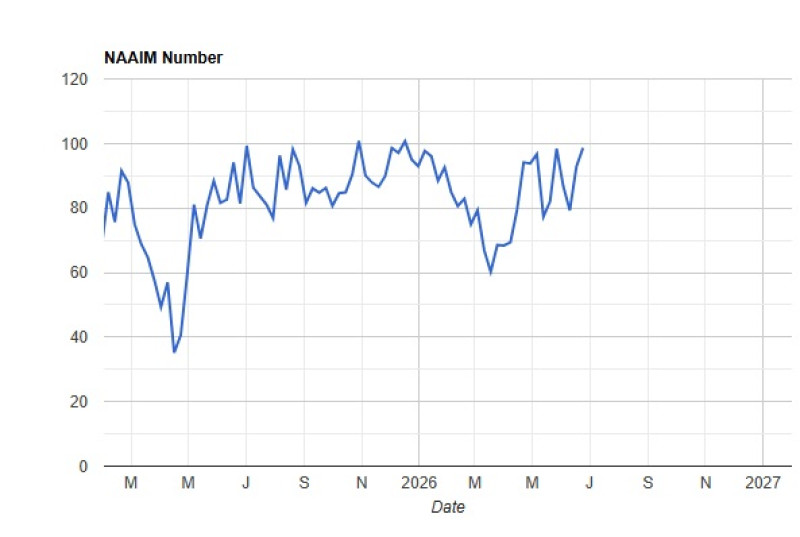

The NAAIM data tells a straightforward story. Managers briefly reduced exposure during the March-April correction before steadily adding risk back into portfolios.

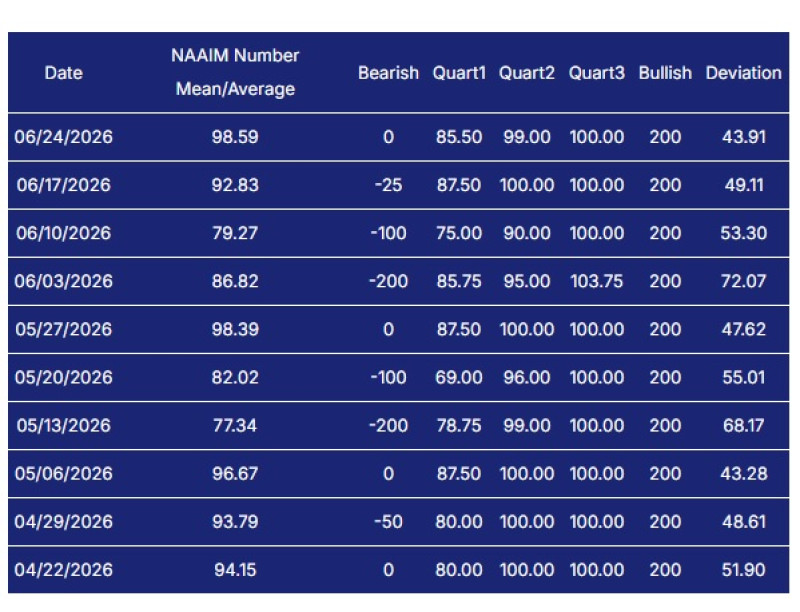

| Date | NAAIM Exposure |

| May 13 | 77.34 |

| May 20 | 82.02 |

| May 27 | 98.39 |

| June 3 | 86.82 |

| June 10 | 79.27 |

| June 17 | 92.83 |

| June 24 | 98.59 |

Exposure has returned to levels typically associated with strong conviction.

That does not imply excessive optimism, but it does suggest that much of the buying has already occurred. Future gains will increasingly depend on new capital entering the market rather than existing investors increasing exposure.

The Options Market Is Sending a Different Signal

Dealer positioning has moved in the opposite direction. Gamma has slipped back below zero, reaching roughly -$5 billion.

Unlike discretionary investors, dealers continuously adjust hedges as prices move. In a positive-gamma environment, those adjustments absorb volatility. Once gamma turns negative, the same hedging activity begins reinforcing price moves instead. The change does not determine market direction. It changes how efficiently the market absorbs shocks.

Why This Combination Is Different

Neither indicator is unusual by itself. Professional managers frequently run high exposure during sustained rallies. Negative gamma also appears several times each year. The current setup is different because both conditions exist simultaneously. One side of the market has already committed capital. The other has become increasingly sensitive to price movement. That leaves less room for additional buying and more potential for selling to accelerate if volatility begins to rise.

Small Catalysts Can Produce Large Moves

Markets rarely require dramatic news when positioning becomes one-sided. An inflation surprise. A weaker earnings report. Higher Treasury yields. An unexpected geopolitical headline. Under positive gamma, these events often produce temporary volatility before stabilizing. Under negative gamma, they can trigger a sequence of dealer hedging, volatility targeting, and portfolio de-risking that extends well beyond the original catalyst. The headline starts the move. Market structure determines its size.

What The Data Suggests

The charts are not forecasting an imminent correction. They describe a market that has become less resilient. Professional managers remain close to fully invested, with NAAIM at 98.59. Dealer positioning, meanwhile, has shifted toward negative gamma near -$5 billion. If markets continue climbing, neither statistic will attract much attention. If volatility returns, however, the combination suggests price swings may become larger and faster than investors have become accustomed to over the past year.

Artem Voloskovets

Artem Voloskovets