Marina Lubimova

Marina Lubimova

The target is less about where the index could trade than about the assumptions behind it. After two years of AI-driven gains, higher prices alone are no longer enough. The next stage requires faster earnings growth, broader productivity gains and stronger returns on capital.

Without those fundamentals, another meaningful expansion in market multiples becomes increasingly difficult.

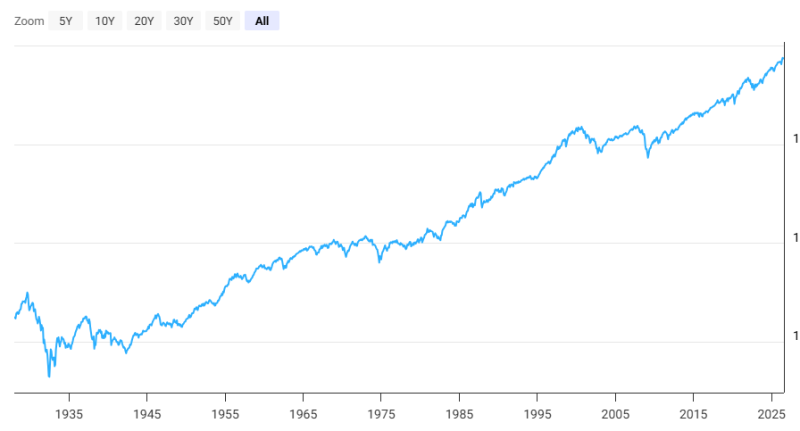

A Long-Term Trend Built on Recovery

Every major market decline eventually became part of a longer-term expansion.

The first chart covers almost a century of market history. It includes the Great Depression, the inflation shock of the 1970s, the dot-com collapse, the Global Financial Crisis and the pandemic. Each episode interrupted the trend, but none changed its direction.

Long-term equity returns have been driven by one recurring factor: corporate earnings continued to expand after every crisis. The same pattern explains why firms remain willing to publish aggressive multi-year targets. It does not eliminate volatility. Every secular bull market included corrections that reset valuations before growth resumed. A move toward 8,325 would almost certainly follow the same path.

Investment Has to Become Profit

The AI cycle has already transformed corporate spending. Capital is flowing into semiconductor manufacturing, hyperscale data centers, enterprise software, cloud infrastructure, and power networks at a pace rarely seen outside previous industrial shifts.

Financial markets have already priced in much of that investment. The next question is whether those expenditures increase productivity quickly enough to lift revenue growth, operating margins and free cash flow across a much larger group of companies. If they do, earnings, not valuation expansion, become the primary driver of the next leg higher.

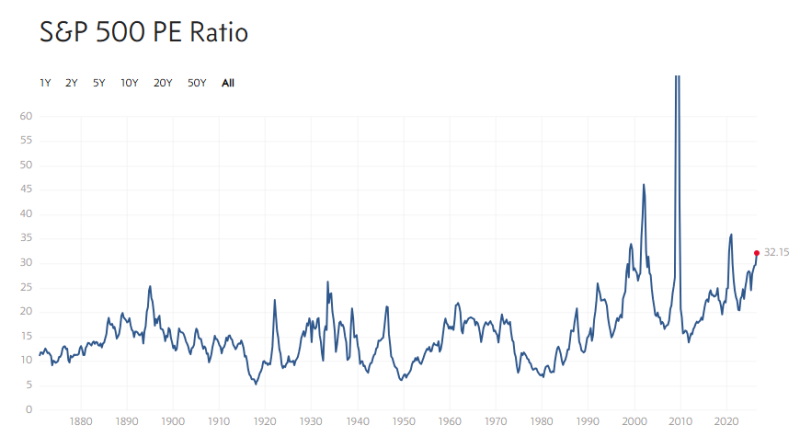

Valuation Leaves Little Margin for Error

The S&P 500 currently trades at approximately 32.15x earnings, well above its long-term average.

The valuation backdrop is difficult to ignore. The S&P 500 traded between 15x and 20x earnings. The current multiple of 32.15x ranks among the highest sustained levels outside periods of exceptional monetary support or speculative excess.

High valuations do not automatically signal an overvalued market. They reduce tolerance for weaker execution. Future returns therefore depend less on investors accepting even higher multiples and more on companies delivering the earnings already embedded in today's prices.

The Next Earnings Cycle Cannot Be Concentrated

The first phase of the AI rally was led by a small group of mega-cap technology companies. The next phase requires broader participation. Industrial automation, utilities, cybersecurity, enterprise software, healthcare technology, financial services and energy infrastructure all stand to benefit if AI adoption improves efficiency throughout the economy rather than inside the technology sector alone. A wider earnings base would make the bull market more durable and reduce dependence on a handful of companies.

Expectations Are Now the Main Risk

Higher markets raise the standard for future performance. Corporate earnings must continue growing despite elevated interest rates. AI investment must generate measurable returns. Productivity gains must offset higher capital spending instead of simply increasing costs. Missing any one of those conditions would make current valuations more difficult to sustain. At today's multiples, execution matters more than sentiment.

Productivity Will Decide Whether the Forecast Holds

Artificial intelligence has already changed investment behavior. The remaining question is whether it changes economic output. Sustainable gains require higher revenue per employee, lower operating costs, faster product development, and stronger returns on invested capital. Those improvements would justify today's valuations and support additional upside. Without them, earnings growth is unlikely to keep pace with market expectations.

Marina Lubimova

Marina Lubimova