Alex Dudov

Alex Dudov

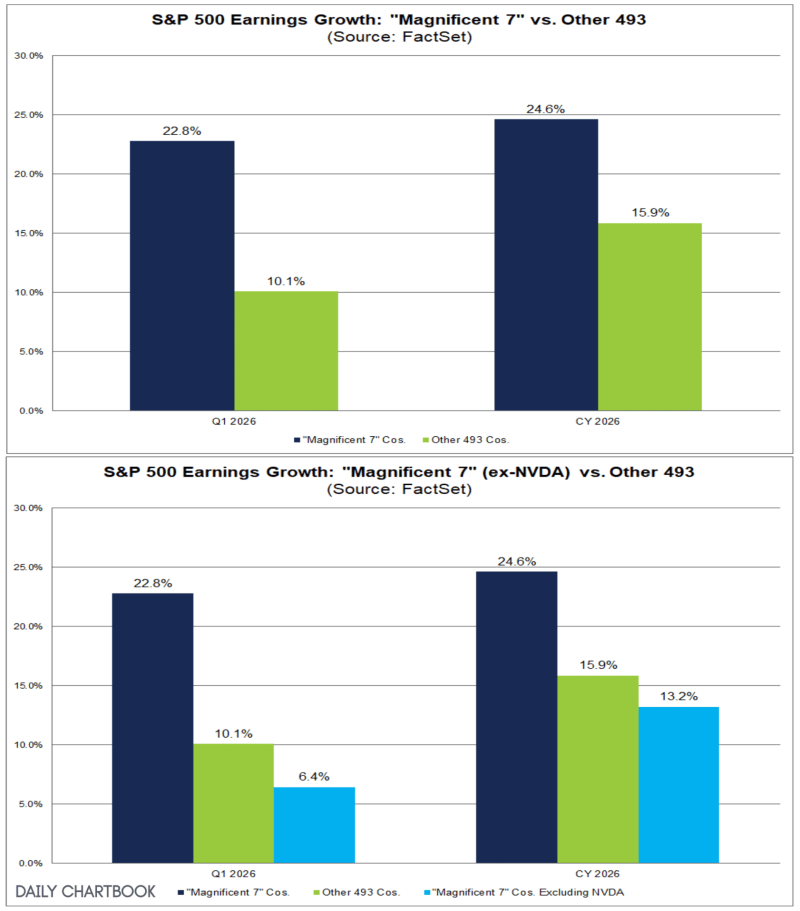

As the new period for financial reporting begins, people who invest are observing if the highest financial performance stays within the largest technology companies or moves to more companies in the index. Due to new forecasts, it is possible that the distribution of growth is changing.

With earnings season just around the corner, I was struck by these charts: MAG7 excluding Nvidia is what Bernt Berg Nielsen stated.

According to Bernt Berg-Nielsen, there is an expectation that the other 493 companies in the index will have a higher rate of profit growth than the group of seven large technology companies when Nvidia is not included.

The remaining 493 companies (in the S&P 500) are expected to deliver stronger earnings growth than the MAG7 group excluding Nvidia in the first quarter (10.1% vs. 6.4%).

And this pattern continues past the first three months of the year. “The same applies to calendar year 2026 (15.9% vs. 13.2%)”.

In those statistics, it is visible that the extra growth associated with large technology companies is much smaller or non existent if Nvidia is excluded. By observing this, it is possible to see that profit growth is spreading to many parts of the market instead of staying within a small number of very large companies.

Alex Dudov

Alex Dudov