Alex Dudov

Alex Dudov

Pandemic disruptions, inflation, aggressive Federal Reserve tightening and repeated recession forecasts all failed to derail spending. Households kept buying, traveling and borrowing, helping sustain economic growth even as financing conditions deteriorated. Now the numbers behind that resilience are becoming harder to ignore.

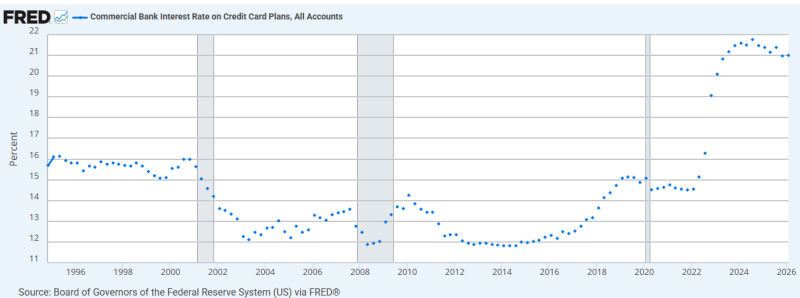

Outstanding U.S. credit card balances have climbed to roughly $1.3 trillion, while average credit card interest rates hover near 21%–22%, the highest levels in modern data series. At the same time, indicators of repayment stress have moved to their weakest levels since the aftermath of the global financial crisis. Taken separately, none of those figures signals an imminent crisis. Together, they suggest a consumer sector increasingly reliant on expensive debt to maintain spending power.

Borrowing Has Replaced the Pandemic Savings Cushion

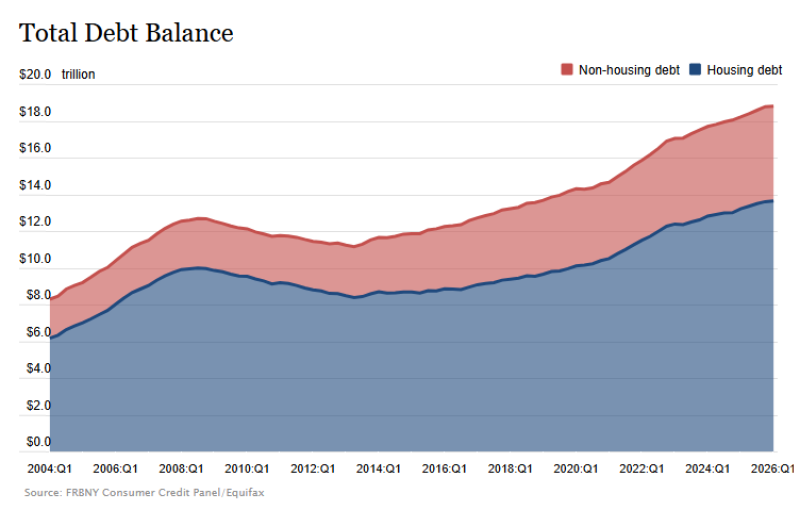

During 2020 and 2021, American households accumulated an unusually large cash buffer thanks to stimulus payments, reduced discretionary spending and strong wage growth.

That cushion has largely disappeared.

Housing costs, insurance premiums, healthcare expenses and everyday necessities have continued to outpace many household budgets, pushing more consumers toward revolving credit. Credit cards have increasingly become a bridge between income and expenses rather than merely a payment tool.

The result is a steady rise in balances even as borrowing costs reach record levels.

For a household carrying a $15,000 balance, a 22% annual percentage rate translates into roughly $3,300 in yearly interest charges before a single dollar of principal is repaid.

The pressure is no longer coming solely from debt accumulation. It is coming from the price of carrying that debt.

This Is Not 2008 - Yet

References to the financial crisis inevitably emerge whenever consumer credit stress rises. The comparison, however, deserves context.

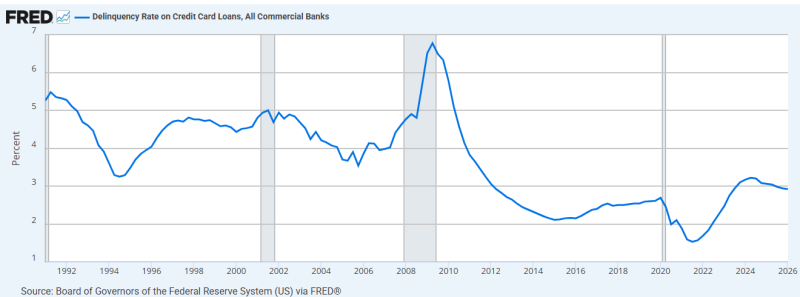

Credit card delinquency rates have been moving higher since 2022, but current readings remain well below the levels recorded during the recession of 2008–2009. At their peak, delinquency rates approached 7%. Today they stand closer to 3%.

The current environment is not defined by a wave of defaults. It is defined by the increasing cost of servicing debt. Average credit card rates spent much of the decade following the financial crisis between 11% and 15%. Over the last several years they surged above 20%, effectively doubling the financing burden for many revolving borrowers.

In other words, consumers are not necessarily failing in large numbers. They are paying substantially more to avoid failing.

Why the Market Should Care

The importance of credit card data extends beyond household finances. Consumer spending accounts for roughly two-thirds of U.S. economic activity. When a growing share of disposable income is redirected toward interest payments, discretionary purchases become increasingly vulnerable.

The effects rarely appear immediately. Consumers often maintain spending by drawing down savings, using existing credit lines or refinancing obligations. Eventually, however, higher debt-servicing costs begin to compete with travel, entertainment, retail purchases and other non-essential spending categories. That dynamic is particularly relevant for investors following consumer-facing businesses.

A slowdown in discretionary spending would affect retailers, travel operators, restaurants and subscription-based services long before it becomes visible in headline GDP data. Rising delinquencies could also pressure lenders through higher charge-offs and increased loan-loss provisions.

Banks have already started preparing for that possibility by tightening lending standards and increasing reserves against potential future losses.

The Signal Beneath the Headlines

The headline figures - $1.3 trillion in credit card balances and interest rates above 20%—are eye-catching on their own. But the broader picture is more nuanced than comparisons to 2008 suggest. Household debt has reached record levels, yet repayment performance remains far stronger than during the financial crisis. The more important shift is that debt has become dramatically more expensive to carry.

For now, employment remains solid and consumer spending continues to support economic growth. The question is not whether Americans can still borrow. The question is how much longer they can afford to.

Alex Dudov

Alex Dudov