Marina Lubimova

Marina Lubimova

The pandemic exposed how vulnerable global supply chains had become to disruptions. In response, governments and corporations launched diversification strategies, reshoring programs, and industrial investment plans aimed at reducing dependence on foreign suppliers. Yet the latest data indicate that many of those risks remain deeply embedded in the U.S. import structure.

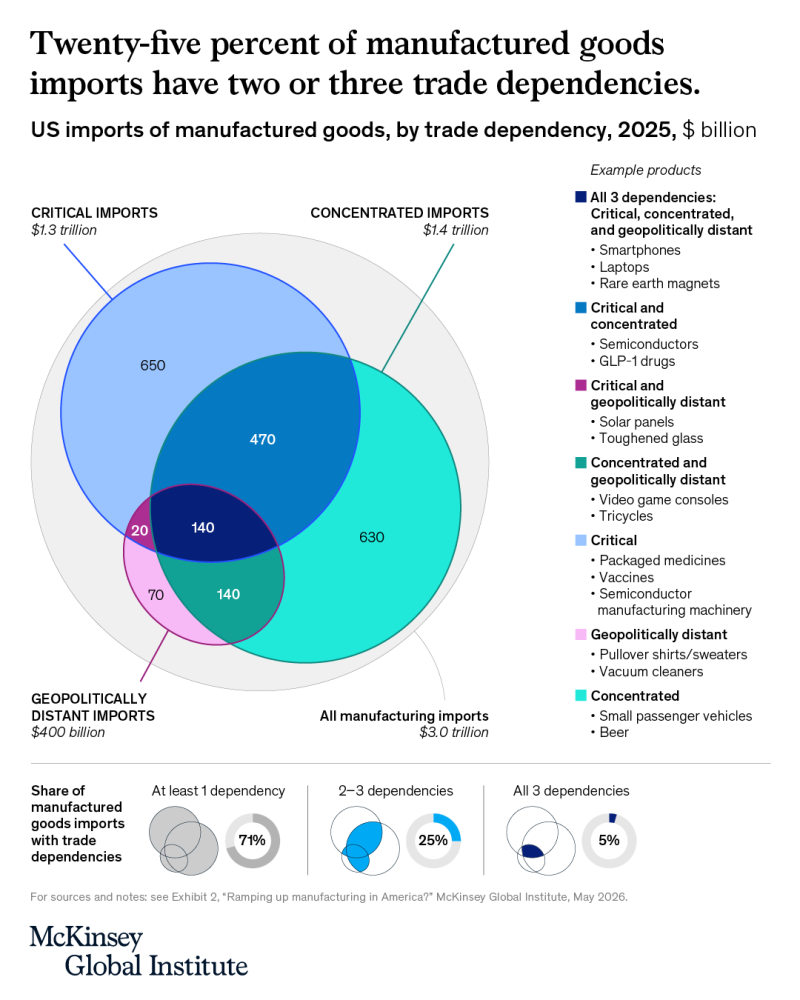

According to McKinsey Global Institute, 71% of U.S. manufactured goods imports in 2025 are exposed to at least one major trade dependency, while 25% face two or three dependencies simultaneously. Most notably, 5% of imported manufactured goods are classified as critical, concentrated, and geopolitically distant at the same time.

Critical Products Often Depend on Multiple Vulnerabilities

McKinsey identifies three main sources of risk.

The first is critical imports - products considered essential for economic activity, healthcare, or national security. These imports account for approximately $1.3 trillion annually and include medicines, vaccines, and semiconductor manufacturing equipment.

The second category is concentrated imports, where supply depends on a limited number of countries or producers. These imports total roughly $1.4 trillion and include products such as consumer electronics and passenger vehicles. The third category consists of geopolitically distant imports, representing approximately $400 billion of annual imports from countries whose political and economic relationships with the United States may introduce additional supply-chain risks.

The greatest vulnerabilities emerge where these categories overlap. Approximately $470 billion of imports are both critical and concentrated, while another $140 billion are both concentrated and geopolitically distant. Around $140 billion of imports, including smartphones, laptops, and rare-earth magnets, fall into all three categories simultaneously.

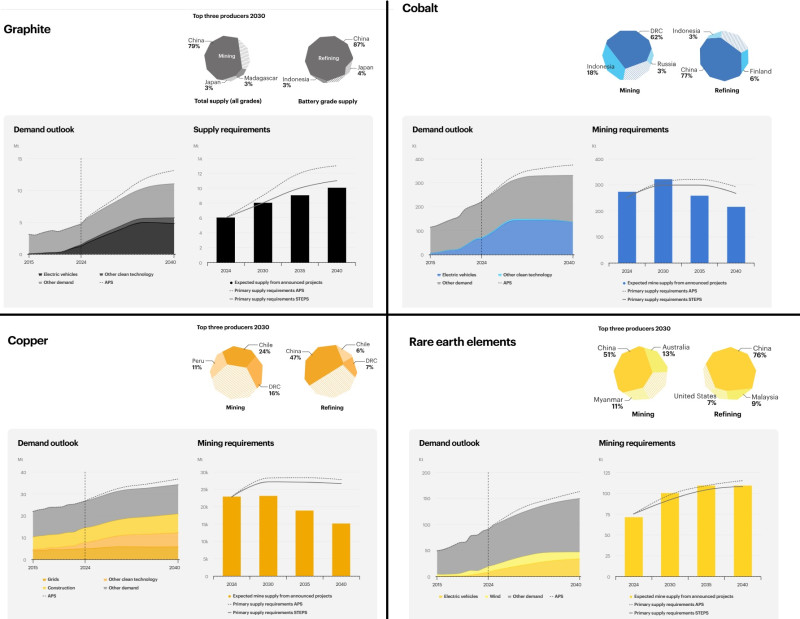

China Still Dominates Critical Material Supply Chains

The concentration challenge extends far beyond finished products. According to International Energy Agency projections for 2030, China is expected to dominate the processing of several materials that underpin modern manufacturing and clean-energy technologies.

China is projected to account for:

- 87% of battery-grade graphite refining

- 77% of cobalt refining

- 76% of rare-earth refining

- 47% of copper refining

These materials are essential for batteries, electric vehicles, semiconductors, power infrastructure, defense systems, and advanced manufacturing. While mining operations may be geographically diversified, refining and processing capacity remains highly concentrated, creating bottlenecks that are difficult to replicate elsewhere.

The challenge is particularly visible in rare-earth elements, where China is expected to control more than three-quarters of global refining capacity by 2030. Similar patterns appear across graphite and cobalt supply chains, both of which play a central role in battery production.

Demand for Critical Materials Continues to Grow

The dependence issue is becoming more significant because demand for many critical materials is expected to rise sharply over the next decade. IEA forecasts show continued growth in demand for copper, graphite, rare-earth elements, and cobalt, driven by electric vehicles, renewable energy infrastructure, battery storage systems, and power-grid expansion.

For example, copper demand linked to power grids, construction, and clean-energy technologies is projected to expand steadily through 2040. Rare-earth demand is also expected to increase as wind power installations and electric vehicle production continue to scale globally. As demand grows faster than supply diversification, concentrated supply chains become increasingly important from both an economic and geopolitical perspective.

America Is Investing Heavily in Manufacturing

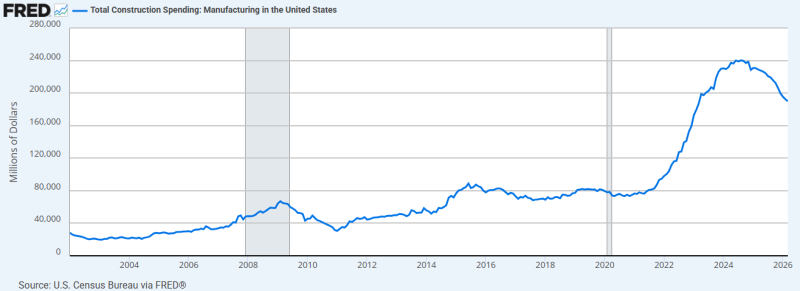

The United States has responded with a historic industrial investment cycle. According to Federal Reserve data, manufacturing construction spending surged from roughly $70–80 billion annually before the pandemic to more than $230 billion at its peak during 2024–2025.

The increase reflects investment linked to reshoring initiatives, semiconductor manufacturing projects, clean-energy incentives, and broader efforts to strengthen domestic production capacity.

However, the McKinsey analysis suggests that building factories is only one part of the equation. Many critical supply chains rely on mining, processing, specialized equipment, and industrial ecosystems that have developed over decades. Recreating those networks requires significant capital, skilled labor, infrastructure, and time.

The Real Challenge Is Replacing Dependencies

The latest data suggest that the debate is no longer about whether supply-chain vulnerabilities exist, but how difficult they will be to eliminate.

Despite unprecedented investment in domestic manufacturing, the United States remains heavily exposed to concentrated and geopolitically sensitive supply chains across a wide range of critical products. At the same time, demand for the underlying materials continues to rise, increasing the strategic importance of refining capacity and industrial infrastructure.

The result is a complex reality: America is building more factories than it has in decades, yet many of the materials and components those factories require remain tied to a small number of global suppliers. Reducing those dependencies may ultimately prove far more difficult than identifying them.

Marina Lubimova

Marina Lubimova