Peter Smith

Peter Smith

Markets keep talking about slowdown risks, weakening consumers, and delayed rate cuts. Corporate revenue forecasts are telling a very different story.

Revenue Expectations Still Look Expansionary

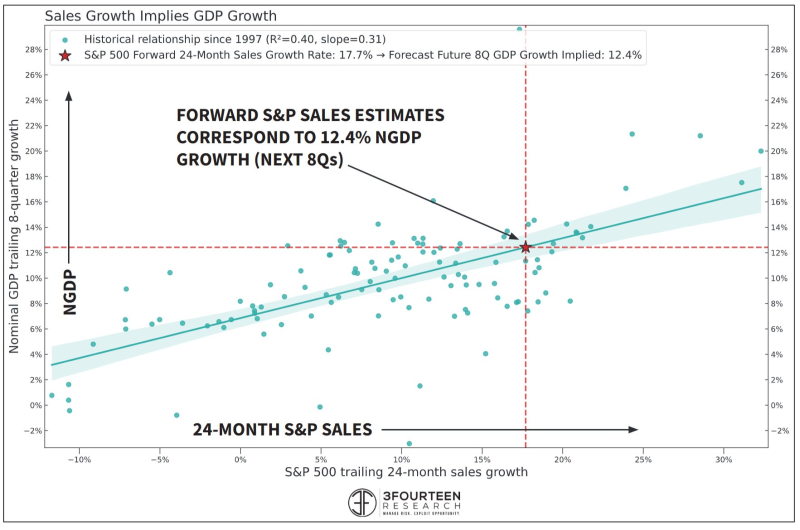

A chart from 3Fourteen Research shows a long-term relationship between S&P 500 sales growth and nominal GDP growth. Based on current forward sales estimates, the market is effectively pricing roughly 12.4% nominal GDP growth over the next eight quarters.

S&P 500 forward sales growth historically tracks nominal GDP growth. Current sales estimates imply roughly 12.4% nominal GDP growth over the next eight quarters.

That level of nominal growth does not usually happen in a weak economy. It typically requires:

- strong consumption;

- elevated fiscal spending;

- persistent inflation;

- aggressive capital investment;

- rising corporate pricing power.

Yet bond markets continue swinging between recession fears and disinflation expectations. Equities are signaling something different. Large-cap stocks still carry revenue assumptions consistent with an expansionary macro environment rather than an imminent contraction.

Markets Are Still Pricing Nominal Growth

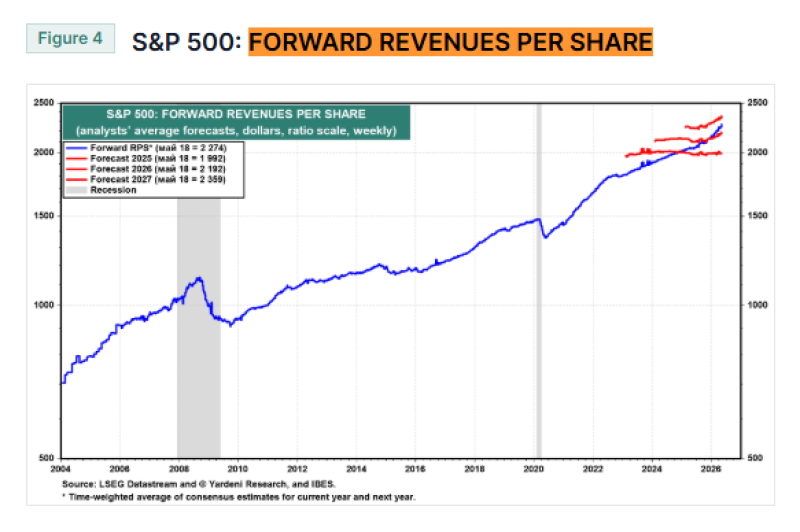

Forward S&P 500 revenue estimates continue pushing toward record highs despite persistent slowdown concerns.

The revenue estimates themselves reinforce the point. Yardeni Research data shows forward S&P 500 revenues per share continuing to rise into 2026 and 2027 forecasts, with consensus estimates approaching roughly 2,274 for 2026 and 2,359 for 2027.

That is not recession pricing. Even after aggressive Fed tightening and years of slowdown warnings, analysts are still modeling revenue growth instead of contraction. The reason nominal growth matters is simple: companies report dollars, not inflation-adjusted output.

That dynamic became increasingly important after 2020, when inflation, fiscal spending, and asset appreciation pushed nominal activity much higher even as real economic conditions became less stable underneath. The charts suggest markets still believe that environment remains intact.

The Economy May Be Running Hotter Than Macro Narratives Admit

Part of that resilience comes from the structure of the U.S. economy itself. Fiscal deficits remain historically large. Industrial policy spending continues expanding. Capital-intensive sectors tied to infrastructure, semiconductors, energy systems, and automation are still absorbing enormous amounts of investment.

The AI infrastructure cycle is now large enough to influence construction activity, electricity demand, industrial production, and corporate capex simultaneously. That does not guarantee the economy avoids slowdown. But it helps explain why equity markets continue pricing stronger nominal activity than much of the macro narrative currently admits.

The deeper implication is that markets may no longer be operating inside the low-growth, low-rate regime that defined most of the 2010s. If nominal GDP remains structurally higher, then bond yields, equity valuations, and corporate pricing power may all need to be repriced around a different macro environment.

Peter Smith

Peter Smith