Artem Voloskovets

Artem Voloskovets

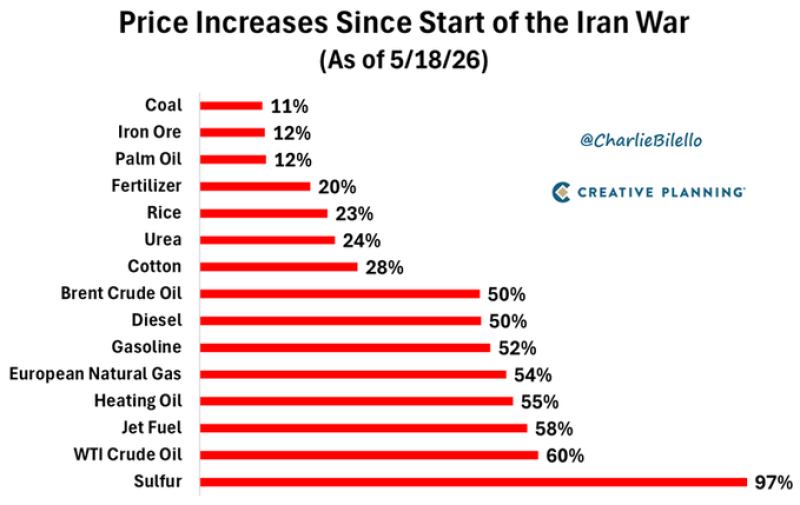

The market reaction to the Iran war is spreading across the entire commodity chain, not just oil.

Sulfur, fuel, fertilizer, and natural gas prices have all surged since the start of the Iran conflict.

The scale of the move is becoming difficult to ignore. Since the start of the conflict, sulfur prices are up 97%, WTI crude 60%, gasoline 52%, European natural gas 54%, and fertilizer 20%. This is no longer a simple oil rally.

Sulfur is the most important signal in the chart. It is deeply tied to fertilizer production, refining, chemicals, and industrial manufacturing. A near-100% spike suggests pressure is moving through supply chains rather than staying isolated inside energy markets. That changes the inflation picture.

Markets entered 2026 expecting disinflation, weaker demand, and eventually lower rates. Instead, energy-linked input costs are rising again across transportation, agriculture, and industrial production simultaneously. The issue is not whether oil prices are rising.

The issue is how broadly the shock spreads.

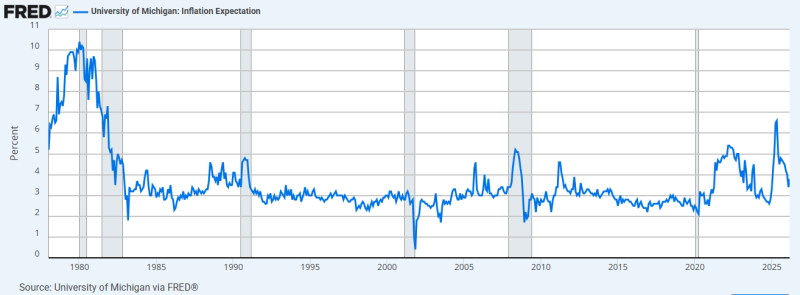

Inflation expectations remain elevated relative to the pre-2020 era.

The inflation backdrop is already unstable. University of Michigan data shows inflation expectations remain structurally above the pre-2020 regime after the post-pandemic inflation shock.

That makes markets more sensitive to commodity disruptions than they were a decade ago.

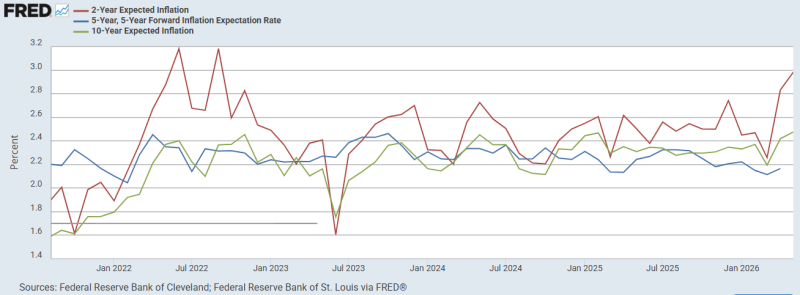

Short-term inflation expectations are rising faster than long-term expectations.

The latest Cleveland Fed data shows 2-year expected inflation approaching 3% again in 2026, while longer-term expectations remain closer to 2.1%–2.3%. That divergence matters.

Markets are increasingly pricing near-term inflation pressure from commodities, logistics, and energy without fully abandoning the idea that central banks can eventually regain control.

European natural gas is another critical signal. A 54% surge suggests energy markets remain fragile despite years of post-2022 adjustments. Any prolonged Middle East disruption immediately affects LNG competition, shipping, and refining economics.

Fertilizer prices rising alongside fuel also raises the risk of delayed food inflation later in the cycle. This is why the current move looks larger than a temporary geopolitical spike. Multiple supply chains are repricing at the same time, while inflation expectations are already elevated. Historically, those conditions rarely stay contained to oil alone.

Artem Voloskovets

Artem Voloskovets