Alex Dudov

Alex Dudov

According to the chart, the index erased roughly $262 billion in 15 minutes, added $405 billion in 11 minutes, lost another $248 billion in 7 minutes, then regained over $210 billion again within minutes. That is not normal price discovery.

It reflects how modern markets increasingly operate through liquidity flows, derivatives positioning, and automated execution rather than traditional investing behavior.

Hundreds of billions of dollars rotated through the S&P 500 within minutes as algorithmic and derivatives-driven flows accelerated volatility.

For decades, markets were driven primarily by:

- earnings;

- macroeconomic expectations;

- valuation models;

- long-term positioning.

Those factors still matter.

But intraday price action increasingly reflects:

- systematic trading;

- ETF flows;

- volatility targeting;

- dealer hedging;

- machine-driven execution.

The market increasingly reacts to liquidity conditions before humans fully process the narrative.

Markets are becoming reflexive

A growing percentage of equity volume is now driven by systems reacting automatically to:

- volatility thresholds;

- options positioning;

- liquidity shifts;

- momentum signals.

That creates feedback loops. Large flows trigger volatility. Volatility forces repositioning. Repositioning creates more flows. Prices move again before narratives stabilize. The result is a market increasingly reacting to itself.

Passive investing changed market structure

Index funds and ETFs improved liquidity efficiency but also increased correlation across markets. Capital now moves through baskets rather than individual stocks. That means positioning shifts affect entire indices simultaneously through:

- ETF inflows and outflows;

- index rebalancing;

- options hedging;

- macro positioning.

This is one reason large intraday moves increasingly feel disconnected from company fundamentals. Many moves are mechanically flow-driven.

Derivatives are reshaping equity markets

Options markets now heavily influence underlying equities. Dealer hedging forces market makers to rapidly buy or sell exposure as volatility changes. That amplifies short-term price movements. Price moves trigger hedging. Hedging accelerates price moves. The system becomes reflexive.

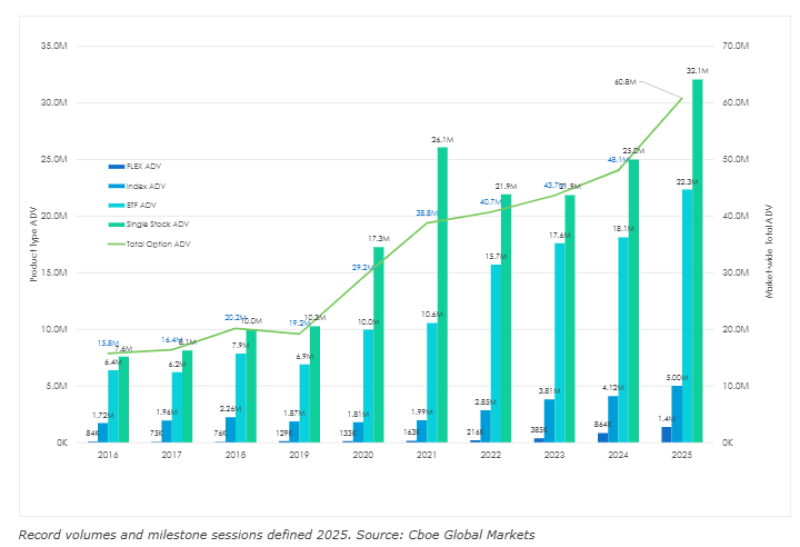

Options trading volume has exploded over the last decade, increasing the influence of derivatives on underlying equity markets. The second chart shows how quickly derivatives activity expanded.

Total options ADV rose from roughly 15.8 million contracts in 2016 to more than 60 million by 2025. Single-stock and index options volume surged at the same time, increasing the impact of dealer positioning and short-term flows on equity prices themselves. Fundamentals still matter. But market structure increasingly determines how fundamentals are expressed through price action.

AI and automation may accelerate this further

AI-driven systems are compressing reaction speed even more.

Modern trading systems can process in real time:

- news;

- positioning data;

- sentiment;

- volatility;

- cross-market flows;

As more capital becomes machine-assisted, markets become increasingly sensitive to liquidity imbalances and positioning reflexes.

That creates an environment where:

- volatility spreads faster;

- liquidity disappears faster during stress;

- discretionary investors lose influence.

Markets can appear highly liquid while becoming structurally fragile underneath.

The bigger shift is structural

Markets have always been volatile. The difference now is that volatility increasingly originates from liquidity mechanics rather than economic information alone. Many large intraday moves now begin with flows and positioning first, while narratives arrive afterward. That changes how modern market risk behaves. The chart may look like a volatile trading session. In reality, it reflects a market increasingly functioning as an automated liquidity system.

Alex Dudov

Alex Dudov