Marina Lubimova

Marina Lubimova

While markets remain obsessed with artificial intelligence, rate cuts, and mega-cap technology stocks, another trend is quietly developing beneath the surface of the U.S. economy: America’s federal workforce is shrinking at one of the fastest rates in decades.

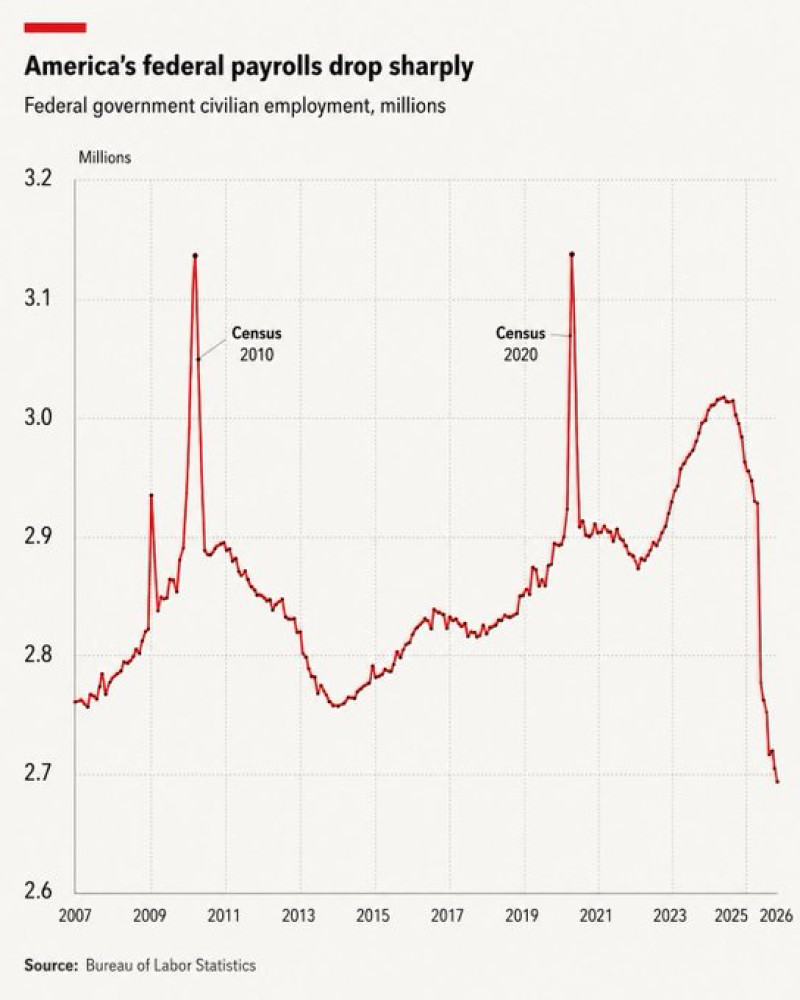

Federal Payrolls Are Falling Fast

The latest data shows federal civilian employment falling below 2.7 million workers after peaking above 3 million only a few years ago. Outside temporary Census-related spikes in 2010 and 2020, the decline now looks unusually aggressive - and potentially far more important than most investors realize.

Most analysts interpret government job cuts as a sign of discipline and fiscal responsibility. Contrarian investors see a different possibility: Washington may be cutting because financial pressure is becoming unavoidable.

Historically, sharp reductions in federal employment often emerge during periods of:

- rising debt burdens

- budget tightening

- slowing economic growth

- increasing political pressure over deficits

In the short term, markets usually welcome these moves because reduced spending can ease inflation concerns and stabilize bond yields. But the longer-term consequences may be less bullish.

Federal jobs traditionally act as an economic stabilizer. Unlike cyclical private-sector employment, government payrolls tend to remain relatively steady during downturns, supporting local economies and consumer demand.

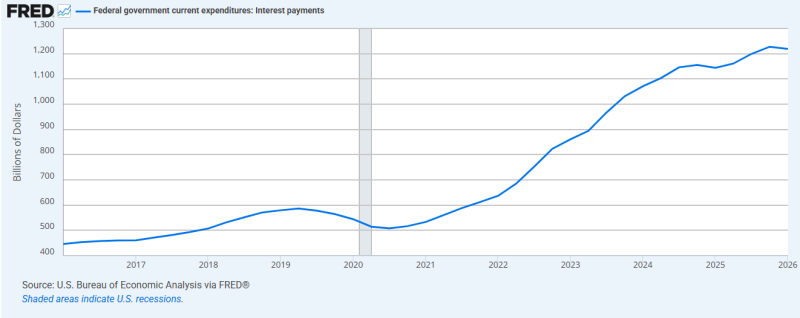

America’s Debt Costs Are Quietly Exploding

The deeper issue may not be employment itself, but what is forcing these cuts to happen. America’s interest payments on federal debt have surged dramatically since 2022, climbing toward record highs above $1 trillion annually. The government is now spending enormous amounts simply to service existing debt.

That changes the narrative completely.

Instead of asking whether Washington wants a smaller workforce, investors may soon begin asking whether it can still afford the old one. For contrarian traders, this matters because markets remain overwhelmingly focused on AI optimism while ignoring mounting fiscal strain underneath the surface.

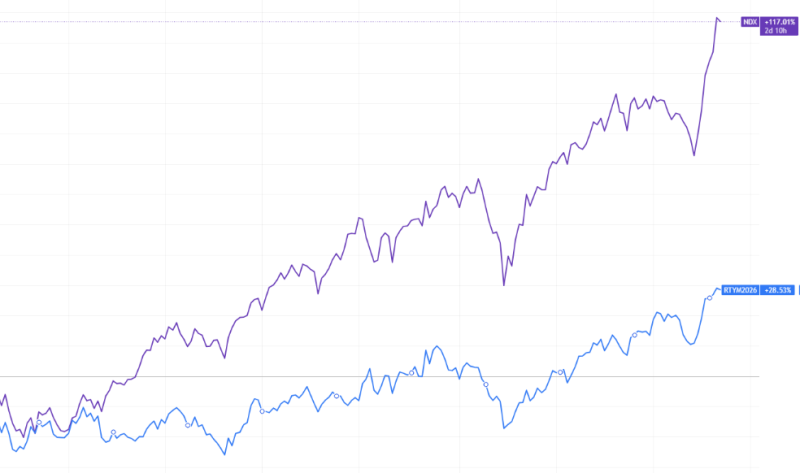

The Stock Market Looks Strong - But Only at the Top

The divergence between mega-cap technology stocks and the broader market tells another important story. While the Nasdaq continues pushing higher, smaller U.S. companies have struggled to keep pace. Much of the market’s strength is now concentrated inside a relatively small group of AI-related companies.

That creates several risks:

- excessive market concentration

- overdependence on AI spending

- weak participation from smaller businesses

- rising vulnerability to sentiment shifts

History shows this type of concentration rarely lasts forever. During previous market cycles, including the dot-com era and the “Nifty Fifty” period, investors also believed a handful of dominant companies could indefinitely outperform the broader economy. Eventually, expectations became too extreme.

Labor Market Cracks May Already Be Forming

Meanwhile, labor market stress may already be quietly building beneath the surface. Continuing unemployment claims remain elevated compared to post-pandemic lows, suggesting displaced workers are taking longer to find new employment. The trend does not yet point to a full recession, but it challenges the market’s belief that the economy remains exceptionally resilient.

For contrarian investors, this contradiction is becoming increasingly important:

- government payrolls are shrinking

- debt servicing costs are exploding

- labor market stress is slowly rising

- yet investors remain concentrated in high-growth technology stocks

That combination could eventually create a very different market environment from the one Wall Street currently expects.

Why Ignored Sectors Could Become the Next Contrarian Trade

If economic momentum weakens further, some of today’s least popular sectors may suddenly regain investor attention. Potential beneficiaries could include:

- utilities

- healthcare

- consumer staples

- dividend-paying value stocks

- energy producers

Ironically, the market’s obsession with AI may be distracting investors from deeper macroeconomic shifts already underway.

The charts may appear disconnected at first glance. Together, however, they tell a much larger story about fiscal pressure, market concentration, and the possibility that the U.S. economy is becoming far more fragile beneath the surface than headline indexes suggest.

Marina Lubimova

Marina Lubimova