Artem Voloskovets

Artem Voloskovets

The latest US macroeconomic release delivered a mixed but critical signal for markets, as inflation data diverged across key indicators while income and spending remained resilient.

According to data from the U.S. Bureau of Economic Analysis, which publishes both GDP and PCE reports, the GDP Price Index came in at 3.6%, below the 3.9% forecast and slightly down from 3.7% previously. This suggests broader price pressures across the economy are easing marginally. However, the more important inflation gauge for the Federal Reserve tells a different story.

Core inflation accelerates again

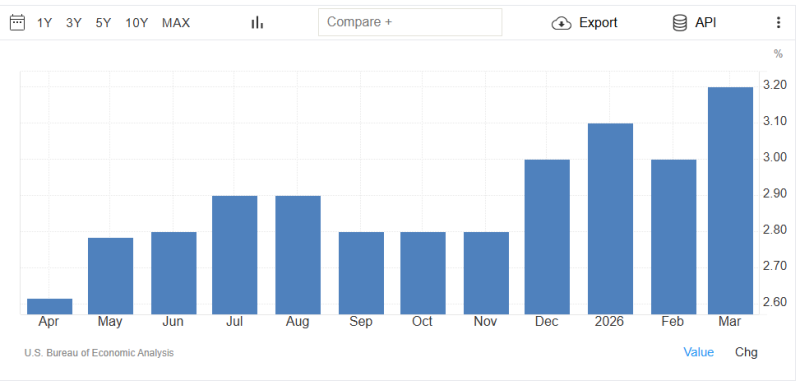

Core PCE Prices (Advance) - the Fed’s preferred inflation metric - rose 4.3%, exceeding the 4.1% forecast and sharply higher than the 2.7% previous reading.

This is significant because core PCE strips out volatile food and energy prices and is considered the most reliable signal of underlying inflation trends.

At the same time:

- Headline PCE Prices (Advance): 4.5% (vs 2.9% prior)

- Indicates broad-based price pressure is re-accelerating

- Confirms inflation persistence despite prior cooling trends

Historically, the Federal Reserve targets 2% inflation, meaning current levels remain well above policy comfort.

Consumer remains stable - but not strong

On the demand side, the data shows a more balanced picture:

- Real Personal Consumption (MoM): +0.2% (below 0.3% forecast, but above 0.1% prior)

- Personal Income (MoM): +0.6% (double the 0.3% forecast, strong rebound from -0.1%)

This combination suggests:

- Consumers still have income support

- Spending is growing, but not accelerating aggressively

- Demand is stable rather than overheating

How markets are likely to interpret this shift

The key takeaway is divergence:

- Inflation (core PCE) → accelerating again

- Growth (GDP price index) → slightly cooling

- Consumer → holding steady

This creates a difficult setup for the Federal Reserve.

Core PCE is widely considered the Fed’s primary inflation gauge, meaning stronger-than-expected data reduces the likelihood of near-term rate cuts. Reuters previously noted that persistent core PCE pressure can delay policy easing.

At the same time, the lack of strong consumption growth suggests the economy is not overheating - pointing toward a “higher for longer” rate environment rather than aggressive tightening.

Bottom line

Instead of presenting this as a separate summary block, the takeaway from the data points to a clear shift in the macro narrative. Inflation pressures, particularly in core metrics, are no longer consistently trending lower, while consumer activity remains stable but not strong enough to signal overheating.

This combination suggests that the Federal Reserve is unlikely to move toward rate cuts in the near term and may instead maintain a restrictive stance for longer than markets previously anticipated. As a result, expectations around monetary policy are becoming more sensitive to incoming inflation data, increasing the likelihood of volatility across risk assets as investors reassess the path of rates, liquidity conditions, and broader economic momentum.

Artem Voloskovets

Artem Voloskovets