Marina Lubimova

Marina Lubimova

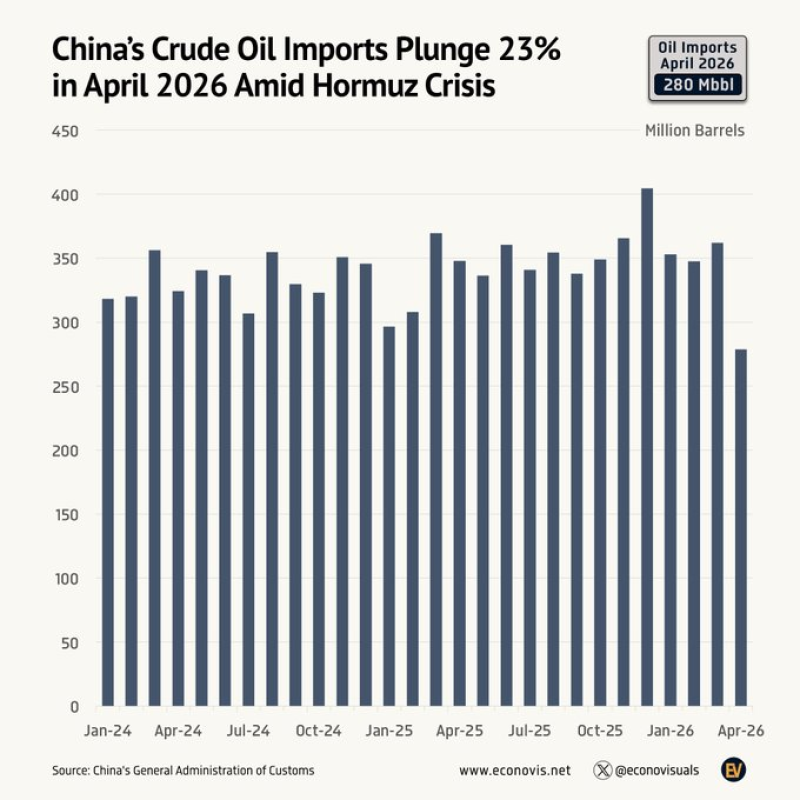

China’s crude oil imports fell to roughly 280 million barrels in April 2026, marking a sharp 23% decline during the Hormuz crisis and one of the weakest monthly readings in more than two years. At first glance, the explanation looks straightforward: geopolitical disruption, shipping uncertainty and temporary trade dislocation. But the scale of the drop suggests something larger may be happening underneath the surface.

Demand Is Starting to Matter More Than Supply

China’s imports stayed relatively stable despite slowing property markets, uneven industrial recovery and weak consumer demand. Monthly volumes largely remained between 320 and 370 million barrels, with occasional spikes above 400 million.

April broke that pattern.

The decline came during one of the most geopolitically sensitive periods for global energy markets. The Hormuz crisis raised fears around shipping security, freight costs and potential supply disruptions across one of the world’s most critical oil corridors.

Historically, that kind of environment pushes countries toward precautionary buying and stockpiling. China did the opposite. That creates an uncomfortable question for commodity markets: what if weak demand is starting to matter more than supply risk?

Oil traders focused primarily on OPEC+ production policy, sanctions and geopolitical instability. Demand assumptions remained relatively resilient because markets expected China to eventually absorb excess supply through industrial recovery and infrastructure spending.

The April numbers complicate that thesis.

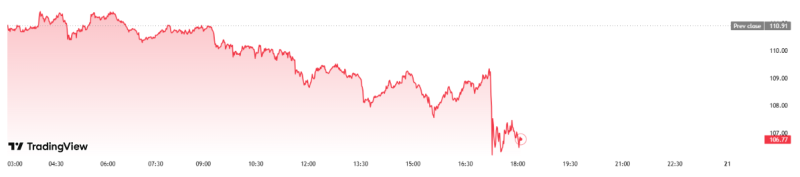

Despite the geopolitical shock surrounding Hormuz, oil prices failed to sustain upside momentum. Instead of rallying on supply fears, crude moved lower as markets increasingly focused on weakening demand signals.

The Market May Be Pricing the Wrong Risk

If Chinese refiners are cutting imports even during elevated geopolitical tension, the market may be facing a broader demand recalibration than current oil pricing fully reflects.

Key signals markets will watch next:

- Chinese refinery activity

- Industrial demand recovery

- Shipping volumes through Hormuz

- OPEC+ supply response

- Freight and insurance costs

That does not necessarily imply an immediate collapse in crude prices, but it weakens one of the market’s core assumptions, that China will continue acting as the world’s demand stabilizer during supply shocks. The implications extend beyond oil.

Lower Chinese import demand pressures shipping activity, industrial commodities and export-heavy economies tied to the global manufacturing cycle. It also reinforces concerns that parts of the post-pandemic commodity trade may have relied too heavily on expectations of a stronger Chinese recovery.

Right now, markets still treat the April collapse as a temporary geopolitical distortion. But if import weakness continues through the summer, investors may have to confront a more difficult possibility: the bigger risk to commodity markets may no longer be supply instability in the Middle East, but slowing demand inside the world’s largest commodity-consuming economy.

Marina Lubimova

Marina Lubimova