Artem Voloskovets

Artem Voloskovets

Inflation faded from the list of market concerns over the past year. Growth, AI spending, and rate-cut expectations took center stage instead. The PMI survey is pointing in a different direction.

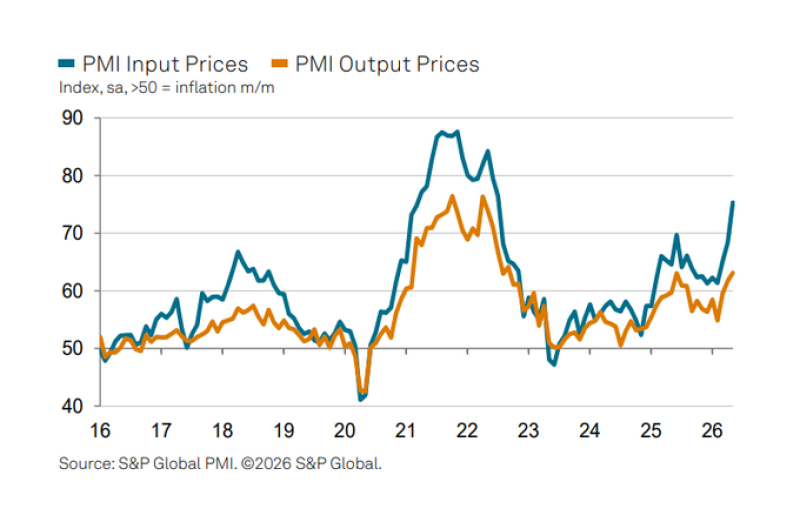

S&P Global's Input Prices Index has surged to around 75, while the Output Prices Index has climbed to roughly 63. Both indicate rising prices, but the gap between them is becoming increasingly difficult to ignore.

The Gap Between Costs and Prices Is Widening Again

One detail stands out. Input Prices have returned to levels last seen during the inflation spike of 2021–2022. Output Prices have also moved higher, but not nearly as fast.

That creates a difficult environment for companies. Every increase in labor, transportation, energy, or raw-material costs has to be absorbed somewhere. Businesses can raise prices, accept lower margins, or try to cut costs elsewhere. The spread between the two PMI measures is now approaching levels that historically appeared when inflation was becoming a larger concern for policymakers and investors.

During 2021 and 2022, businesses eventually passed much of those higher costs to customers. The question is whether the same process is beginning again.

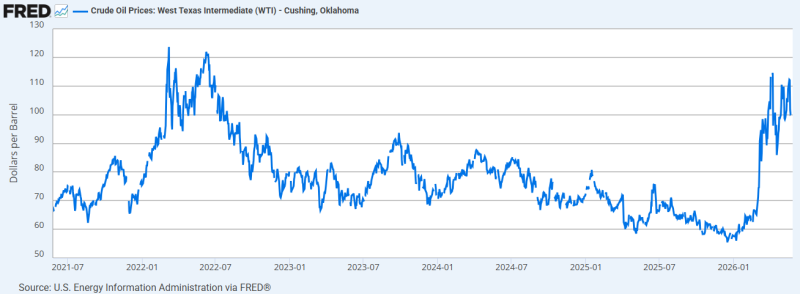

Oil's Return Above $100 Is Showing Up in Business Surveys

A likely explanation can be found in energy markets.

WTI crude traded near $55 per barrel at the start of 2026. By spring, prices had moved above $100 and briefly approached $110. That represents an increase of roughly 80% to 100% in only a few months.

A move of that magnitude rarely stays confined to oil producers. Fuel affects shipping costs, manufacturing expenses, chemicals, packaging, agriculture, and logistics. Higher energy prices tend to work their way through supply chains long before they appear in official inflation reports.

Oil began moving higher early in the year. PMI input costs followed shortly afterward. The relationship does not prove causation, but the timing is difficult to dismiss. Businesses are reporting stronger cost pressures at the same moment energy markets are experiencing one of their sharpest rallies in years.

The Market Is Still Pricing a Disinflation Story

Investor positioning continues to reflect expectations that inflation will remain contained and that monetary policy will gradually become less restrictive.

The PMI data points to a different risk. If businesses continue facing higher costs, they will eventually attempt to recover those expenses through higher prices. If consumers resist, margins become vulnerable. If companies succeed, inflation may stop cooling as quickly as markets expect.

Either outcome challenges the assumption that the path toward lower inflation will remain smooth. This is particularly relevant because many equity valuations have expanded alongside expectations for easier policy and stable earnings growth. A renewed rise in inflation pressure would complicate both assumptions.

The question now is whether the recent jump turns into a trend. One month of survey data is not enough to declare the return of inflation. Commodity markets can reverse quickly, and temporary disruptions can produce short-term distortions.

Still, the combination of a PMI Input Prices Index near 75, Output Prices moving above 60, and oil rising from roughly $55 to more than $100 presents a set of signals that investors cannot easily ignore.

Artem Voloskovets

Artem Voloskovets