Marina Lubimova

Marina Lubimova

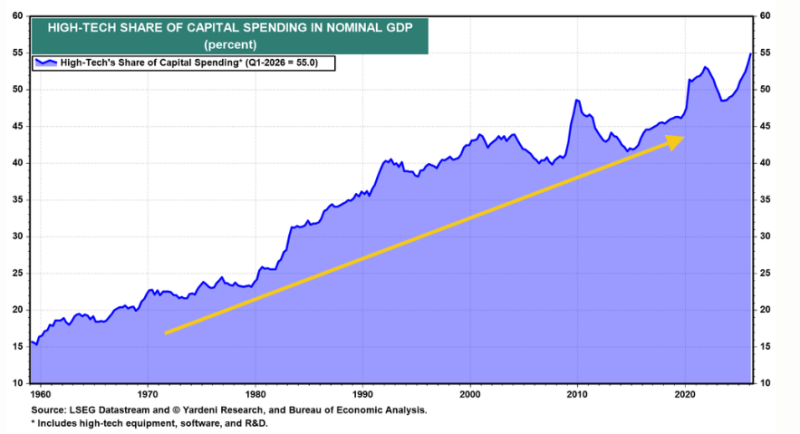

Technology's role in the U.S. economy is no longer measured only by stock market valuations. New data from Yardeni Research shows that high-tech industries represented 55% of capital spending relative to nominal GDP in the first quarter of 2026, the highest reading in the dataset going back to 1960.

High-tech industries accounted for 55% of capital spending relative to GDP in Q1 2026.

The Economy Is Allocating Capital Differently

In 1960, technology-related investment represented roughly 15% of total capital spending. The share climbed gradually during the PC era, accelerated during the internet buildout of the 1990s, and continued rising through the cloud computing boom. The latest AI cycle has pushed the trend into new territory.

Unlike earlier software waves, generative AI requires large-scale physical investment. Data centers, advanced chips, networking equipment, cooling systems, transformers, and power infrastructure have become essential inputs for growth.

The spending required to train and operate AI models is creating demand far beyond the technology sector itself. Utilities, industrial suppliers, construction firms, and equipment manufacturers are increasingly tied to the same investment cycle.

The AI Buildout Is Becoming Visible in the Real Economy

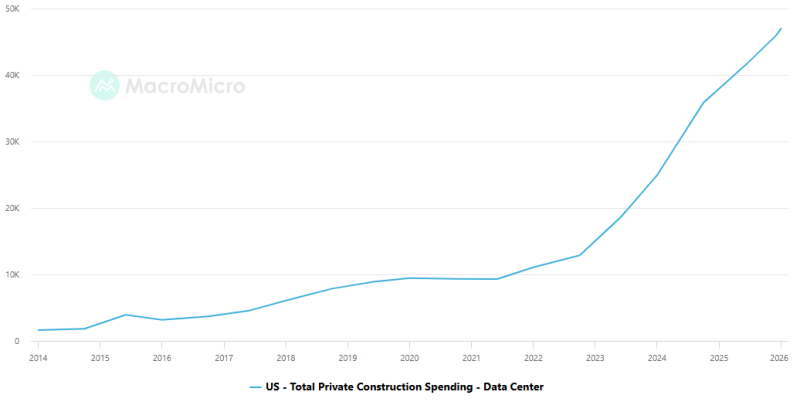

The rise in technology's share of capital spending is no longer confined to corporate budgets or earnings reports. It is increasingly visible in physical construction activity across the United States.

Spending on U.S. data center construction has accelerated sharply since 2023 as companies expand AI infrastructure capacity.

Data center construction spending remained below $1 billion per month for most of the last decade. That changed rapidly after the launch of generative AI systems and the race to secure computing capacity.

The second chart shows how investment accelerated between 2023 and 2026, with spending climbing to record levels as cloud providers, technology companies, and infrastructure operators expanded their footprints. Monthly spending has more than doubled in just a few years, underscoring the scale of the buildout underway.

Unlike previous software cycles, AI requires physical assets that cannot be scaled instantly. New facilities need advanced semiconductors, networking equipment, cooling systems, backup power, and reliable access to electricity. The result is a spending wave that extends well beyond Silicon Valley and into energy, construction, and industrial supply chains.

Capital Is Following Expected Productivity Gains

Corporate spending decisions often reveal where executives expect future returns.

The rise from roughly 40% a decade ago to 55% today suggests companies are directing a growing share of investment budgets toward technologies expected to improve productivity, automate workflows, and expand computing capacity.

That helps explain why semiconductor manufacturers, cloud providers, and AI infrastructure companies have captured an increasing share of global market value. The capital allocation trend visible in the chart appeared years before many of the valuation gains seen across AI-related equities.

Capital Is Concentrating Around AI Infrastructure

The combination of the two charts reveals a broader shift in capital allocation. The first shows where investment is flowing at the macroeconomic level. The second shows how that capital is being deployed in practice.

Together, they suggest that AI is becoming an infrastructure investment cycle rather than a traditional software cycle. The distinction matters because infrastructure booms tend to last longer, involve more sectors of the economy, and generate larger downstream effects on employment, energy demand, and industrial activity.

The concentration of spending also raises the stakes. When more than half of capital investment is linked to technology, the trajectory of economic growth becomes increasingly tied to the success of AI-related projects. Continued expansion could support productivity growth across multiple industries. A slowdown would likely be felt far beyond the technology sector itself.

The record 55% reading therefore represents more than a milestone for the technology industry. It reflects a fundamental shift in how capital is being allocated across the U.S. economy and the scale of the AI infrastructure buildout suggests that shift is still unfolding.

Marina Lubimova

Marina Lubimova