Artem Voloskovets

Artem Voloskovets

Aluminum is becoming one of the most tightly supplied industrial commodities in the global economy. Exchange inventories tracked by the London Metal Exchange, Shanghai Futures Exchange, and CME-linked warehouses now cover less than five days of worldwide consumption. At the same time, aluminum prices have climbed to approximately $3,675 per ton, up roughly 50% from levels seen a year ago.

The combination of shrinking inventories and rising prices suggests that supply concerns are no longer confined to warehouse data. They are beginning to show up in the market itself.

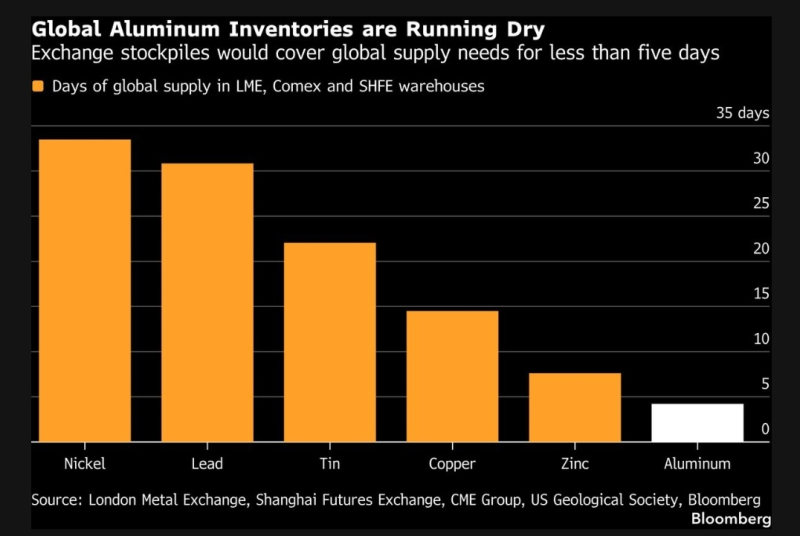

Aluminum inventories now represent less than five days of global demand, the lowest coverage among major industrial metals.

Aluminum Has the Smallest Inventory Buffer Among Major Metals

Inventory coverage across industrial metals varies widely. Nickel stockpiles are equivalent to roughly 31 days of global demand, while lead inventories cover about 29 days. Tin stands near 21 days and copper around 13 days. Zinc inventories represent approximately six days of consumption.

Aluminum is the clear outlier. With less than five days of visible supply available through major exchanges, the market has a much smaller buffer against unexpected disruptions than most other industrial metals.

That matters because aluminum sits at the center of multiple industries simultaneously. It is used in transportation, packaging, construction, electrical infrastructure, renewable energy systems, and data-center equipment.

Prices Are Already Moving Higher

The inventory squeeze is occurring alongside a strong rally in aluminum prices. Over the past year, aluminum has climbed from roughly $2,450 per ton to around $3,675 per ton. The move has pushed the metal close to the highest levels seen in years.

Aluminum prices have risen roughly 50% over the past year, reaching around $3,675 per ton.

The timing is difficult to ignore. As inventories have continued to decline, buyers have been willing to pay increasingly higher prices to secure supply. This contrasts with previous periods when slowing economic growth offset concerns about physical availability. The latest price action suggests traders are paying closer attention to supply conditions than they were a year ago.

China's Role Makes the Market More Fragile

China accounts for roughly 60% of world aluminum output. That concentration means decisions made by Chinese producers, regulators, and energy authorities can influence supply conditions far beyond the country's borders. A reduction in smelter output, higher electricity costs, environmental restrictions, or export policy changes could quickly tighten an already constrained market. Unlike commodities with more diversified production networks, aluminum remains heavily dependent on a limited number of regions and producers.

Demand Growth Is Coming From Multiple Directions

The demand story extends well beyond traditional construction activity. Electric vehicles require large amounts of lightweight metal to improve efficiency. Power grids need aluminum-intensive transmission infrastructure. Renewable energy projects depend on aluminum components, while the rapid buildout of data centers is creating another source of industrial demand.

Many of these trends are structural rather than cyclical. At the same time, expanding aluminum production is neither quick nor inexpensive. New smelters require large capital investments, significant energy supplies, and years of development before reaching full capacity. That makes supply less responsive just as consumption continues to expand.

A Market With Little Margin for Error

The aluminum market is not facing an immediate shortage. However, visible inventories have fallen to levels that leave little flexibility if production or transportation problems emerge. With exchange stockpiles covering less than a week of global demand and prices already moving higher, the market appears increasingly sensitive to supply-side shocks.

The risk is not simply higher prices. It is the possibility that disruptions which would have been manageable several years ago could now have a much larger impact on costs, procurement, and delivery schedules.

The shrinking inventory cushion suggests aluminum may become one of the key industrial metals to watch as electrification, infrastructure investment, and data-center expansion continue reshaping global commodity demand.

Artem Voloskovets

Artem Voloskovets