Sergey Diakov

Sergey Diakov

The headline numbers alone are unusually extreme. Goldman’s latest session finished roughly 9% skewed toward net selling - a level sitting in the 91st percentile versus the past year. Hedge fund activity was even more aggressive, with net supply reaching negative 18%, while long-only managers were also active sellers across Tech, Industrials, and Energy.

When hedge funds reduce exposure on their own, markets often absorb the move as tactical positioning. When long-only accounts begin cutting risk alongside fast money, the market structure itself starts to look more fragile.

That distinction matters because modern equity rallies increasingly depend on concentrated liquidity rather than broad participation.

Wall Street’s Rally Became a Single Trade

Over the past year, U.S. equity performance became heavily concentrated within a relatively small group of AI-linked mega-cap stocks. The rally stopped behaving like a normal thematic allocation months ago. It evolved into the market’s primary liquidity engine.

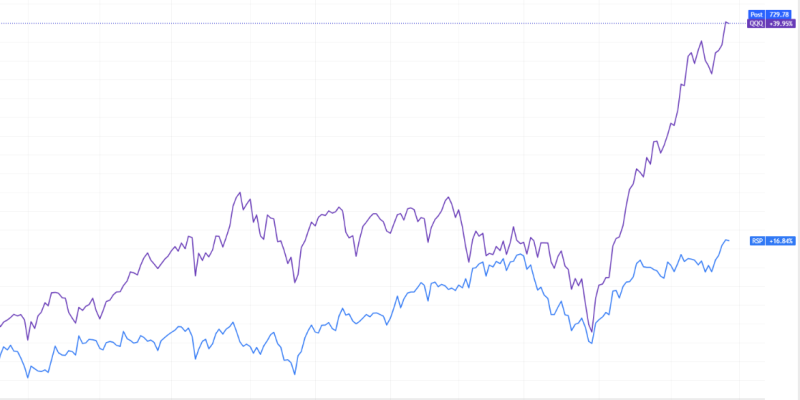

Over the past year, QQQ dramatically outperformed the equal-weight S&P 500, highlighting how heavily U.S. equity gains depended on a narrow cluster of AI-linked mega-cap stocks.

Once positioning becomes too consensus-heavy, relatively small macro shifts can trigger synchronized selling across:

- hedge funds,

- ETFs,

- passive flows,

- quant strategies,

- and long-only institutional portfolios.

At that point, liquidity deterioration becomes nonlinear because too many portfolios effectively hold variations of the same trade. Goldman’s desk activity suggests that the process may already be starting.

Institutions Are Selling More Than Tech

The selling inside Energy may be one of the most important details in the entire flow picture. Under a typical rotation environment, institutional money leaving high-duration Tech exposure would usually migrate toward:

- commodities,

- defensives,

- inflation-linked sectors,

- or cyclicals benefiting from higher yields.

Instead, desks are seeing active selling pressure across Energy alongside aggressive Tech supply. In other words, institutions may not simply be repositioning portfolios. They may be reducing overall balance-sheet risk.

Higher Yields Are Starting to Break the AI Momentum Trade

The timing of the sale is also important. Treasury yields have started drifting higher again, even as equity indexes remain heavily dependent on AI-related leadership.

Historically, that combination creates stress for crowded growth positioning because higher yields raise discount-rate pressure on long-duration equity trades precisely when positioning is already stretched.

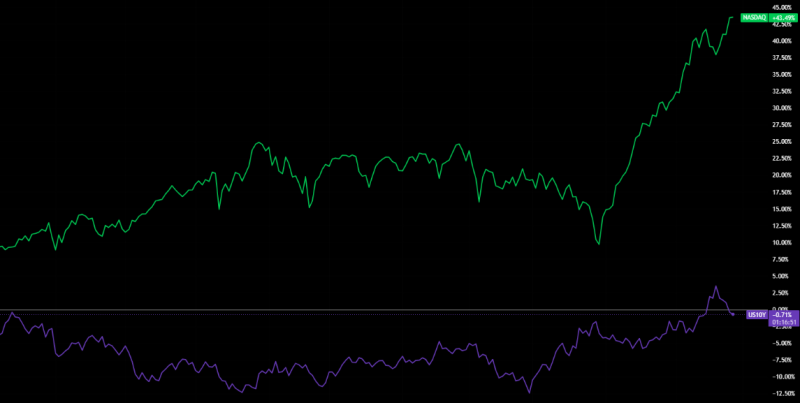

Nasdaq gains accelerated even as the U.S. 10-year Treasury yield stopped falling and began moving higher again - a divergence that historically creates pressure on crowded growth positioning. Industrials' selling may be an even more important warning sign than weakness in software or semiconductors.

Over the past year, Industrials quietly became one of Wall Street’s preferred second-order AI trades through:

- electrification,

- grid expansion,

- automation,

- datacenter infrastructure,

- and power demand expectations.

If institutions are trimming exposure there as well, markets may be starting to question the timing and scale of the broader AI capex cycle rather than simply taking profits in software winners.

Crowded Markets Tend to Unwind All at Once

For large portfolio managers, crowded positioning rarely becomes dangerous because fundamentals suddenly collapse. The real risk emerges when liquidity disappears during synchronized de-risking.

Passive flows amplified the concentration to a much higher. The same mechanism can accelerate downside volatility once institutional investors begin reducing exposure simultaneously.

But three consecutive sessions of unusually aggressive institutional selling, from both hedge funds and long-only accounts, suggest the market may be shifting away from momentum concentration and toward capital preservation. Historically, those transitions tend to last longer than traders initially expect.

Sergey Diakov

Sergey Diakov