Marina Lubimova

Marina Lubimova

The U.S. consumer is still spending aggressively. Retail activity remains relatively resilient, unemployment is still low by historical standards, and consumer-driven growth continues to support the broader economy. But underneath those headline numbers, household balance sheets are deteriorating.

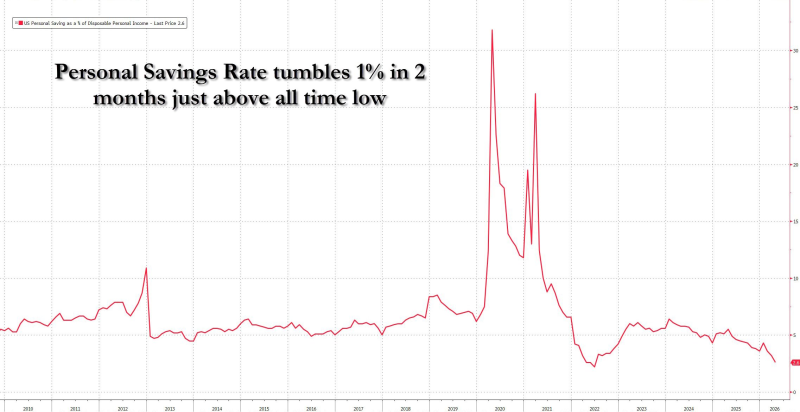

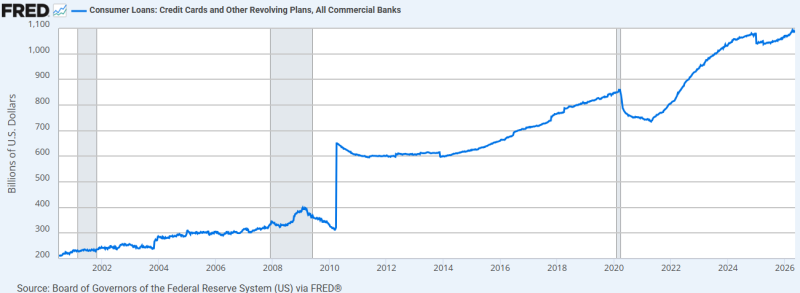

America’s personal savings rate fell to 2.6% in the latest reading, down from 4.3% in January and one of the sharpest short-term declines since the post-pandemic normalization period began. At the same time, revolving consumer credit, primarily credit card debt has climbed above $1 trillion, reaching fresh record highs.

Together, the two trends suggest the strength of the U.S. consumer is increasingly being financed through depleted savings and rising debt rather than improving financial health.

The Consumer Still Looks Strong, but the Quality of Growth Is Changing

Consumer spending remains one of the main pillars supporting U.S. economic growth in 2026.

That resilience has helped:

- stabilize GDP expectations,

- support corporate earnings,

- and reduce immediate recession fears.

However, the latest savings data changes the quality of that narrative. Households appear to be maintaining spending levels despite:

- elevated interest rates,

- persistent inflation pressure,

- slower real wage growth,

- and the disappearance of pandemic-era excess savings.

In other words, spending remains strong, but the financial foundation supporting it is becoming weaker.

Credit Card Debt Is Sending the Same Warning Signal

The collapse in savings is occurring alongside another major trend: a surge in revolving consumer debt.

Americans now hold more than $1 trillion in credit card debt, the highest level on record. Historically, falling savings paired with rising consumer debt tends to signal that households are increasingly financing consumption through borrowing rather than income growth or accumulated liquidity.

That dynamic can support economic activity temporarily, but it often leaves consumers more vulnerable later in the cycle if:

- unemployment rises,

- credit conditions tighten,

- or debt servicing costs remain elevated.

The Pandemic Savings Cushion Has Effectively Disappeared

During the pandemic stimulus era, U.S. households accumulated unusually large cash reserves. Savings rates briefly surged above 30% as stimulus checks, lockdowns, and reduced discretionary spending boosted liquidity across the economy. That cushion has now largely vanished. Instead of rebuilding savings as inflation moderates, many households continue drawing down reserves while simultaneously relying more heavily on credit to maintain spending behavior. The trend suggests consumers have not fully adjusted to the higher-rate environment created by the Federal Reserve’s tightening cycle.

Why Markets May Be Underestimating the Risk

One of the key risks for investors is that headline consumption data can remain strong even while underlying household finances weaken. That creates a potentially misleading macro picture: economic growth appears stable in the short term, while financial stress quietly builds underneath.

Markets typically focus on:

- retail sales,

- payrolls,

- and GDP growth.

But balance-sheet deterioration tends to become visible later in the cycle - often after spending momentum already begins slowing. If savings continue falling while debt burdens rise, consumer resilience could weaken much faster than headline economic data currently suggests.

Key Numbers

| Indicator | Latest Reading |

| US Personal Savings Rate | 2.6% |

| Savings Rate in January | 4.3% |

| US Credit Card Debt | Above $1 trillion |

| Main Macro Risk | Consumption increasingly debt-driven |

The broader message from the data is becoming harder to ignore: the U.S. consumer is still supporting economic growth, but increasingly by exhausting savings and relying on debt rather than through stronger household finances.

Marina Lubimova

Marina Lubimova