Artem Voloskovets

Artem Voloskovets

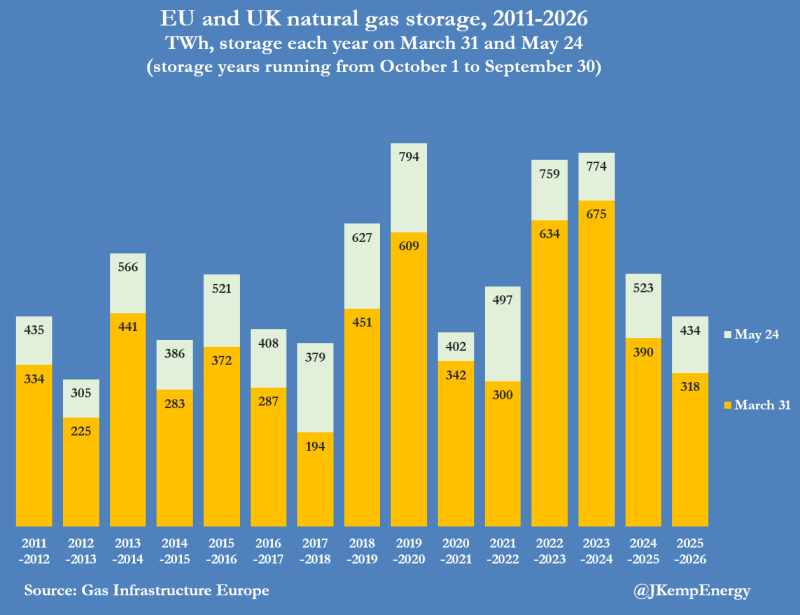

Europe is entering the summer refill season with its weakest gas inventory position in four years. EU and UK storage facilities held 434 TWh of natural gas on May 24, according to Gas Infrastructure Europe data. That compares with 523 TWh a year earlier and 774 TWh in May 2023.

EU and UK Natural Gas Storage, 2011–2026 Source: Gas Infrastructure Europe

The deficit originates from winter withdrawals. Storage levels stood at 318 TWh on March 31, versus 390 TWh in 2024 and 675 TWh in 2023, leaving operators with significantly more gas to inject before next winter. The tighter storage picture is already reflected in prices.

Dutch TTF Natural Gas Futures, 1-Year Performance Source: Trading Economics

Dutch TTF gas futures trade near €47/MWh, almost double the levels seen at the end of 2025. While far below the peaks of 2022, prices indicate the market is assigning a premium to refill-season risks.

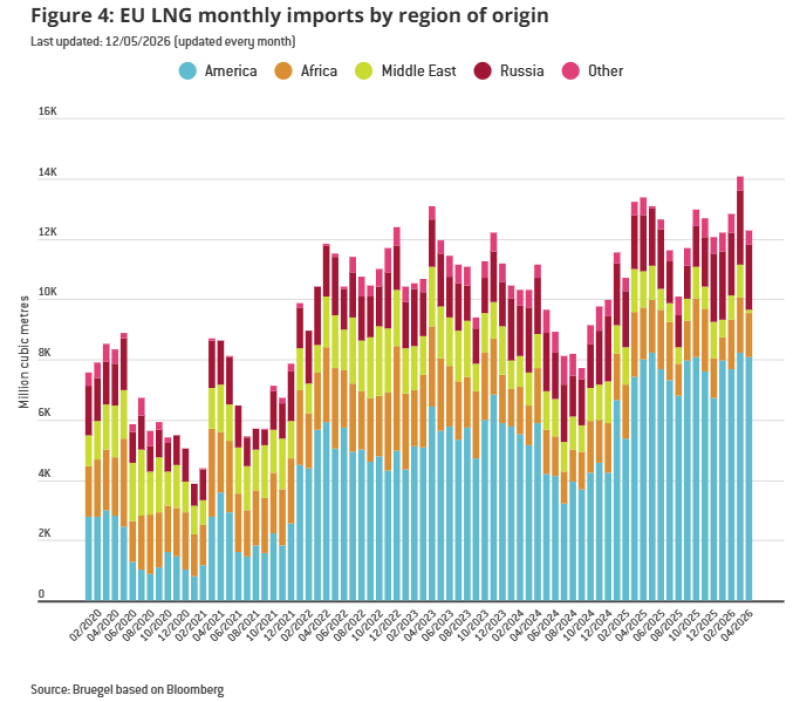

Europe is not lacking supply. LNG imports remain near historical highs as the region continues to rely on seaborne cargoes to replace lost Russian pipeline volumes.

EU LNG Imports by Region of Origin Source: Bruegel

Imports from the Americas account for the largest share of LNG arrivals, helping keep total inflows close to record levels. Even so, inventories remain below the levels reached during the previous three refill seasons.

That leaves Europe more exposed to supply disruptions and stronger Asian LNG demand than it was a year ago. The challenge is straightforward: storage operators must rebuild inventories from a lower starting point while competing for cargoes in the global market.

The latest data do not point to an energy crisis. They do show that Europe's gas market is entering summer with a smaller buffer and less room for error than in recent years.

Artem Voloskovets

Artem Voloskovets