Peter Smith

Peter Smith

The US bond market is undergoing a historic downturn that is rewriting long-standing assumptions about fixed income investing. New data shows that the current drawdown in the Bloomberg US Aggregate Bond Index has extended far beyond any previous cycle, both in duration and scale.

For decades, bonds were considered a stabilizing force in portfolios. Today, the data suggests a different reality - one where prolonged losses challenge traditional strategies and force investors to rethink the role of fixed income.

A Drawdown Unlike Anything in Decades

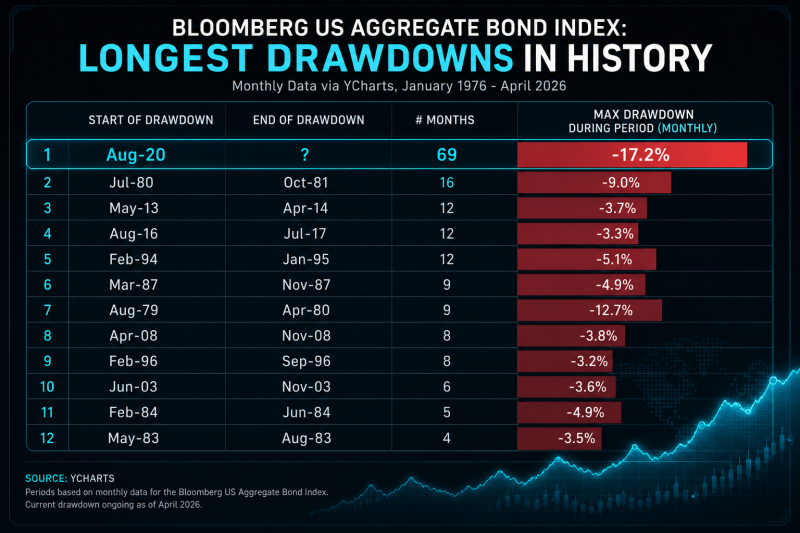

The US bond market is in the middle of its longest drawdown in modern history. According to Bloomberg data, the Bloomberg US Aggregate Bond Index has been declining since August 2020 and has not yet recovered, marking a 69-month downturn as of 2026.

This surpasses previous major drawdowns, including the 1980–1981 period, which lasted 16 months, and multiple shorter cycles that typically ended within a year. The current cycle is not only longer but also deeper, with a maximum drawdown of approximately -17.2%.

Why this drawdown is different

Unlike past bond market declines, which were relatively short-lived, the current downturn has been driven by a prolonged shift in macroeconomic conditions.

The key factor is the rapid increase in interest rates. Bonds move inversely to yields, meaning that as central banks raise rates, bond prices fall. Since 2020, aggressive tightening policies have pushed yields higher across the curve, creating sustained pressure on bond valuations. Inflation has also played a central role. Elevated inflation levels forced policymakers to maintain higher rates for longer, preventing the typical quick recovery seen in previous bond cycles.

How it compares historically

The chart shows that most bond drawdowns since the 1970s lasted between 4 and 12 months. Even during periods of economic stress, such as the early 1980s, declines were relatively short compared to today.

The current 69-month drawdown stands out not only for its duration but also for its consistency. Instead of a sharp drop followed by recovery, the market has experienced a prolonged period of weakness, reflecting structural changes rather than a temporary shock.

What it means for investors

For investors, this shift changes how bonds are perceived. Traditionally considered a “safe” asset, bonds have failed to provide stability during this period, particularly in diversified portfolios.

However, the same dynamics that caused the drawdown may also create future opportunities. Higher yields mean that newly issued bonds offer better income potential, which could support returns once rate cycles stabilize. The key takeaway is that bonds are transitioning from a low-yield environment to a higher-yield regime. This transition is painful in the short term but may reset expectations for long-term investors.

Peter Smith

Peter Smith