Marina Lubimova

Marina Lubimova

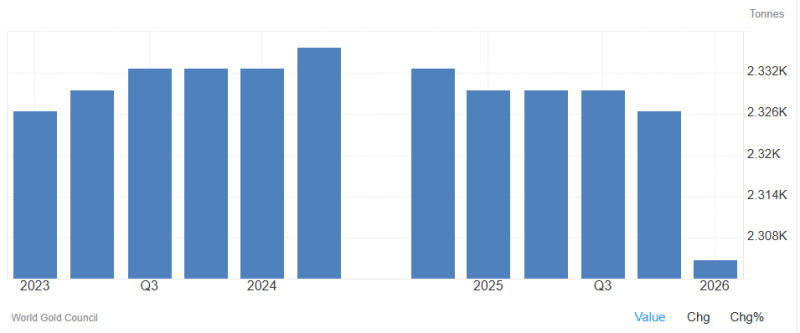

Russia's central bank reduced gold reserves by 6 tonnes in April, bringing total sales this year to 28 tonnes and leaving official holdings at 2,299 tonnes.

The reduction is modest. Russia still owns one of the world's largest official gold stockpiles. At current market prices near $3,300 per ounce, the country's remaining holdings are worth roughly $240–245 billion.

That figure becomes more interesting when compared with Russia's fiscal position.

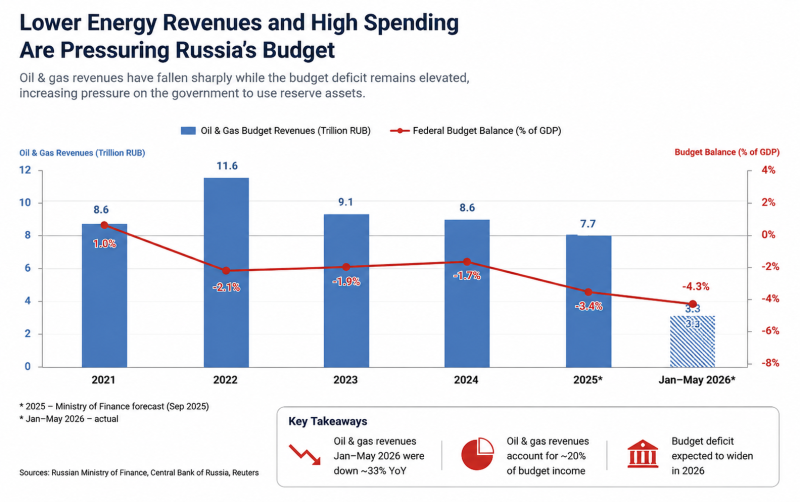

The second chart shows why reserve assets are attracting attention. Oil and gas budget revenues fell to 3.3 trillion rubles in January–May 2026, down roughly 33% year-over-year, while the federal budget deficit widened to approximately 4.3% of GDP.

Under those conditions, gold becomes more than a reserve asset. It becomes a source of financial flexibility. The 28 tonnes sold since the beginning of the year represent approximately 900,000 troy ounces of gold. At current prices, that equals roughly $3 billion in liquidity.

That amount is small relative to Russia's total reserve stockpile but large enough to demonstrate how gold can be converted into funding when budget pressures increase.

The key takeaway is scale. A $3 billion reduction barely dents a gold reserve base worth more than $240 billion. Russia could continue using gold as a supplementary funding source for years without materially exhausting its holdings.

That does not mean gold can permanently solve fiscal challenges. Sustained deficits ultimately require stronger revenues, lower spending, or additional borrowing. But the reserve stockpile gives policymakers valuable breathing room while those adjustments are made.

The latest reduction therefore, says less about immediate financial stress and more about capacity. Even after selling 28 tonnes this year, Russia retains one of the world's largest gold buffers, a reserve large enough to support government finances long after smaller sources of liquidity have been exhausted.

Marina Lubimova

Marina Lubimova