Marina Lubimova

Marina Lubimova

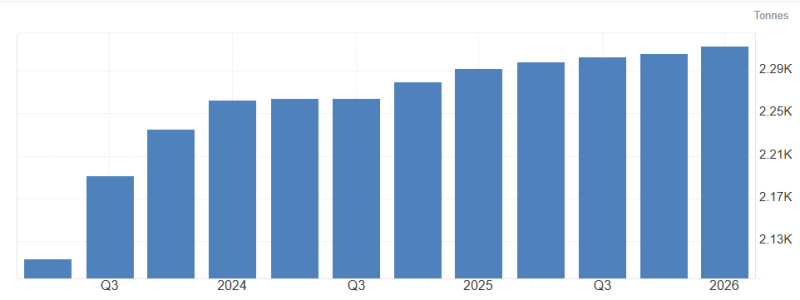

New data shows the People’s Bank of China purchased another 8 tonnes of gold in April - the largest monthly addition since December 2024. That follows 5 tonnes added in March, making this the second-largest two-month accumulation period since early 2024. More importantly, April marked China’s 18th consecutive month of official gold purchases.

Total reported reserves have now climbed to a record 2,322 tonnes.

China Gold Reserves Continue Rising

China’s official gold reserves have steadily climbed to record highs as the country continues long-term reserve diversification and strategic accumulation.

At first glance, the purchases may appear relatively modest compared to the size of global financial markets. But central bank gold accumulation has historically mattered less because of size and more because of signaling.

And China’s signal is becoming increasingly difficult to ignore.

China Is Buying Gold While Others Chase Momentum

The broader market narrative in 2026 has centered around:

- AI-driven equities

- technology megacaps

- crypto speculation

- aggressive risk appetite

- expectations of monetary easing

Gold, meanwhile, has increasingly been treated as a slower-moving defensive asset. That is precisely why China’s continued accumulation stands out. Rather than chasing momentum trades, the country appears to be steadily increasing exposure to a monetary asset with no counterparty risk.

Since 2022, China has officially increased its gold reserves by roughly 372 tonnes - a 19% increase in just a few years. That makes the country one of the strongest sovereign gold buyers globally.

And despite gold remaining near historically elevated levels, Beijing appears to be using pullbacks as accumulation opportunities rather than reasons to reduce exposure.

In other words: China is buying the dip in gold while much of the market focuses elsewhere.

The Bigger Trend Is De-Dollarization

China’s gold accumulation is not occurring in isolation. Over the past several years, central banks globally have accelerated reserve diversification away from traditional dollar-heavy holdings.

The trend has been driven by multiple factors:

- geopolitical fragmentation

- sanctions risk

- rising sovereign debt concerns

- currency volatility

- long-term monetary uncertainty

Gold benefits from all of them.

Unlike sovereign bonds or foreign reserves held in another country’s currency, physical gold remains politically neutral collateral. That characteristic becomes increasingly attractive in a world where financial systems are becoming more fragmented. China’s persistent buying suggests the country may be preparing for a more multipolar reserve system over the long term.

Why Central Bank Buying Matters for Gold

Retail investor sentiment often swings rapidly with interest rates, inflation data, or short-term price action. Central banks operate differently.

They buy with multi-year strategic horizons.

That makes sustained official accumulation particularly important because it creates structural demand largely disconnected from speculative trading cycles.

China’s current pace of buying now puts the country on track for its largest annual gold accumulation since 2023. And because central bank demand tends to be less price-sensitive, continued sovereign buying can help tighten global physical supply even during periods of weaker investor enthusiasm. This dynamic is increasingly creating a floor underneath the gold market.

Markets May Be Underestimating the Signal

Many investors still view gold primarily as an inflation hedge.

But central bank accumulation suggests something broader may be happening: a gradual repricing of monetary trust itself. The world’s largest economies continue carrying historically elevated debt burdens, while geopolitical fragmentation keeps increasing pressure on the global financial system.

Against that backdrop, China appears to be treating gold less like a commodity and more like strategic monetary infrastructure.

That distinction matters. Because if sovereign reserve diversification accelerates further, the long-term gold bull case may become less dependent on retail demand and more tied to structural changes inside the global monetary system itself.

And while much of the market remains focused on chasing the next AI or crypto rally, one of the world’s largest central banks keeps quietly accumulating hard assets instead.

Marina Lubimova

Marina Lubimova