Marina Lubimova

Marina Lubimova

The increase is negligible on its own. What matters is that mortgage rates remain above 6% despite months of expectations that borrowing costs would ease in 2026. The housing market entered the year expecting relief. Instead, financing costs have settled into a range that continues to limit affordability, suppress transactions, and reshape supply dynamics.

The Market Expected Lower Rates

At the beginning of the year, many forecasts assumed mortgage rates would gradually decline as inflation cooled and the Federal Reserve moved closer to rate cuts. That has not happened.

Rates briefly approached 6% before moving back toward 6.5%. The latest Freddie Mac reading extends a pattern that has dominated the market for months: every decline in borrowing costs has been temporary.

The difference between a 6% mortgage and a 6.5% mortgage is significant. Monthly payments rise, purchasing power falls, and fewer homes fit within budget. The result is not a collapse in demand. It is a market where buyers remain active but increasingly selective.

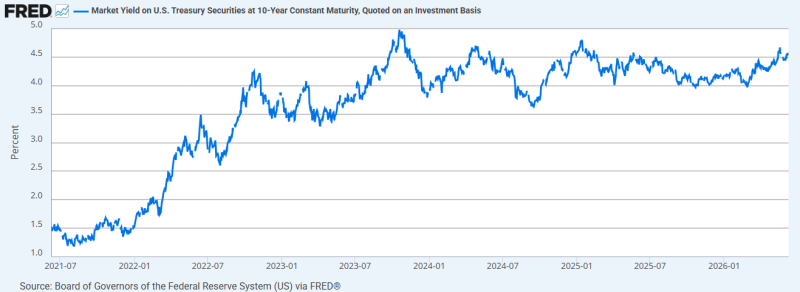

Mortgage Rates Follow Bonds, Not Headlines

Mortgage rates are often discussed through the lens of Federal Reserve policy. In practice, the bond market matters more. Lenders price long-term mortgages against long-term Treasury yields, particularly the 10-year Treasury. Over the last five years, the 10-year yield has climbed from roughly 1.2% to around 4.5%.

The 10-year Treasury yield has returned to roughly 4.5%, remaining near the upper end of its recent range.

The chart shows that yields never returned to pre-inflation levels. After peaking near 5% in late 2023, they stabilized above 4%, keeping pressure on long-term borrowing costs. That is why expectations for lower mortgage rates have repeatedly failed to materialize. The bond market continues to price a higher-rate environment than many investors expected.

The Housing Market's Supply Problem Is Getting Worse

Higher mortgage rates do more than reduce affordability. They discourage existing homeowners from selling. Millions of Americans refinanced during 2020–2021 and secured mortgage rates between 2.5% and 4%. Selling today often means replacing that loan with one above 6.5%. Many choose not to move.

The result is straightforward:

- fewer listings;

- lower turnover;

- tighter inventory;

- persistent price pressure.

The housing market is no longer constrained primarily by demand. In many regions, it is constrained by supply. This dynamic helps explain why home prices have remained resilient despite the sharp increase in borrowing costs over the past several years.

Rates Above 6% Are Starting to Look Structural

Mortgage rates have spent most of 2026 above levels many analysts expected.

- Apr. 23: 6.23%

- Apr. 30: 6.30%

- May 14: 6.36%

- May 21: 6.51%

- May 28: 6.53%

- Jun. 4: 6.48%

- Jun. 11: 6.52%

The trend is more important than the weekly change. Markets spent much of the past year treating elevated mortgage rates as temporary. Current pricing suggests the market is beginning to accept that rates between 6% and 7% may persist longer than previously assumed.

What Investors Should Watch

Mortgage rates influence far more than housing transactions. Higher borrowing costs reduce refinancing activity, slow home sales, limit household mobility, and affect spending tied to moving and homeownership.

Several sectors are particularly sensitive:

- regional banks;

- mortgage lenders;

- real estate brokers;

- home improvement retailers;

- residential REITs.

At the same time, limited housing supply continues to support homebuilders, which have benefited from a market where new construction increasingly fills the gap left by reluctant sellers.

If the 10-year yield moves materially lower, mortgage rates are likely to follow. If yields remain near current levels, borrowing costs may stay elevated regardless of future Federal Reserve decisions.

Marina Lubimova

Marina Lubimova