Artem Voloskovets

Artem Voloskovets

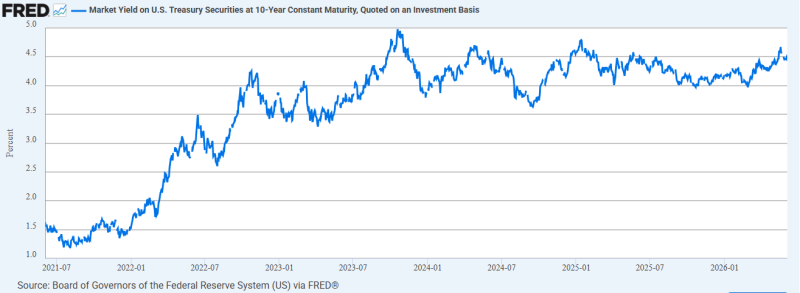

The U.S. 10-year Treasury yield rose to 4.559%, returning to levels that have repeatedly capped equity rallies over the past two years. The move comes as investors continue to push back expectations for aggressive rate cuts and demand higher returns for holding long-term government debt.

Treasury Yield Is Testing an Important Level

The benchmark yield increased from 4.522% to 4.559%, reaching an intraday high of 4.575%. The number matters because yields above 4.5% have historically coincided with weaker risk appetite and pressure on expensive equity sectors.

The broader trend is clear. In 2021, the 10-year yield traded near 1.5%. It later surged to almost 5% during the 2023 bond selloff and is now back near the upper end of its 2025–2026 range. The market has not returned to the low-rate environment investors became accustomed to during the previous decade.

The Bond Market Is Repricing Rate Expectations

Long-term yields tend to rise when investors expect inflation, growth, or government borrowing to remain elevated. That is what current pricing suggests. Despite repeated discussions about future Federal Reserve easing, Treasury yields remain far above levels typically associated with an imminent rate-cut cycle. The bond market is signaling that borrowing costs may stay higher than equity investors would prefer.

Global Bond Markets Are Moving Higher Too

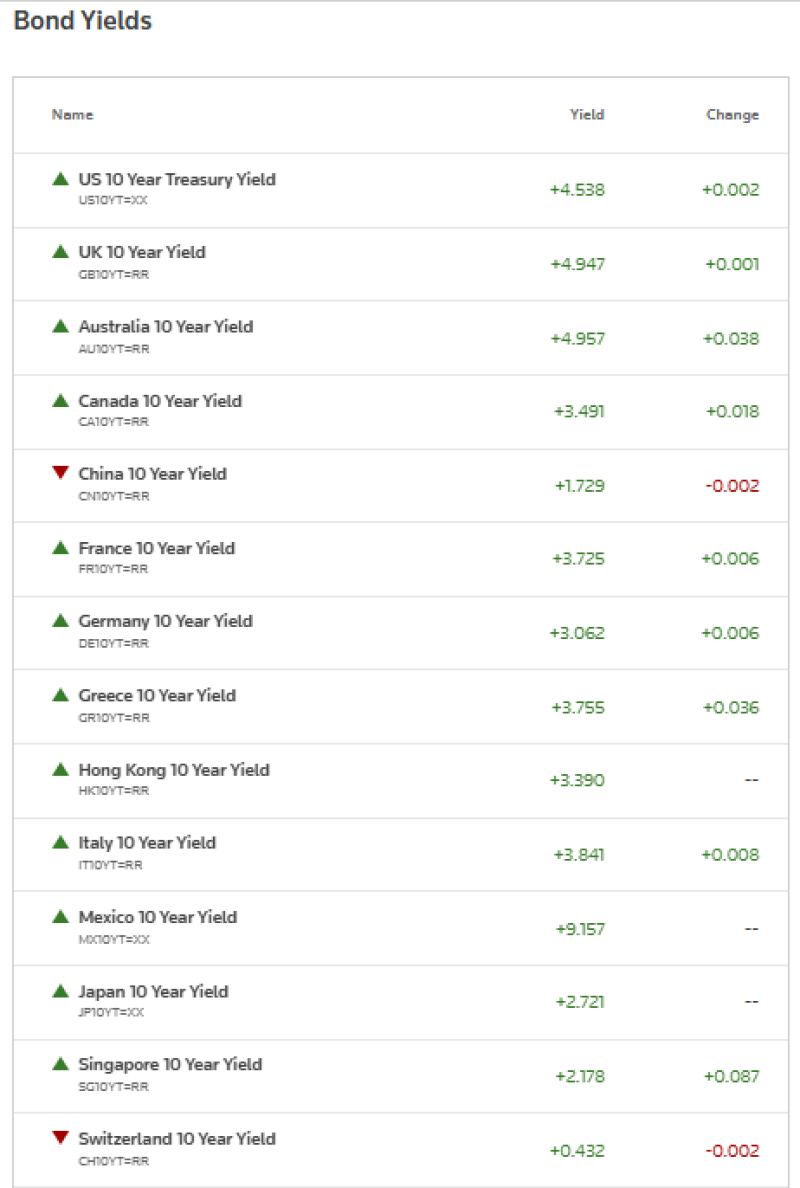

The move is not isolated to the United States.

Australia's 10-year yield stands at 4.957%, the UK at 4.947%, while France, Germany, Italy, Greece and Canada also posted gains. Meanwhile, China's 10-year yield remains at 1.729% and Switzerland's at 0.432%, reflecting weaker growth expectations and a different policy backdrop. The rise across multiple developed markets points to a broader reassessment of long-term interest-rate expectations.

Why Equity Investors Care

Higher Treasury yields directly affect stock valuations. As yields increase, investors can earn more from government bonds, reducing the premium they receive for taking equity risk. The effect is most visible in growth stocks, where valuations depend heavily on future earnings. A yield moving toward 5% forces investors to ask whether current multiples remain justified.

Is 5% Back on the Table?

The current yield remains below the cycle high near 4.9%, but the gap is narrowing. A move back toward that level would tighten financial conditions further and increase pressure on sectors that benefited most from expectations of lower rates. The next major test for markets is whether Treasury yields stabilize near current levels or continue climbing toward the highs reached during the 2023 bond selloff.

Artem Voloskovets

Artem Voloskovets