Artem Voloskovets

Artem Voloskovets

The yield on the U.S. two-year Treasury note rose to 4.147%, its highest level since February 2025. That number looks like another bond-market statistic. In reality, short-term Treasury yields often reveal changes in expectations before they become visible elsewhere in the financial system. The latest move suggests investors are becoming less convinced that borrowing costs will continue falling at the pace many expected earlier this year.

Why a Bond Yield Is Suddenly a Stock Market Story

The two-year Treasury is closely tied to expectations for Federal Reserve policy. When investors expect fewer rate cuts, or believe rates will remain elevated for longer, yields on short-term government debt tend to rise. That shift affects equities because higher yields increase the return available from low-risk assets and raise the discount rate used to value future corporate earnings.

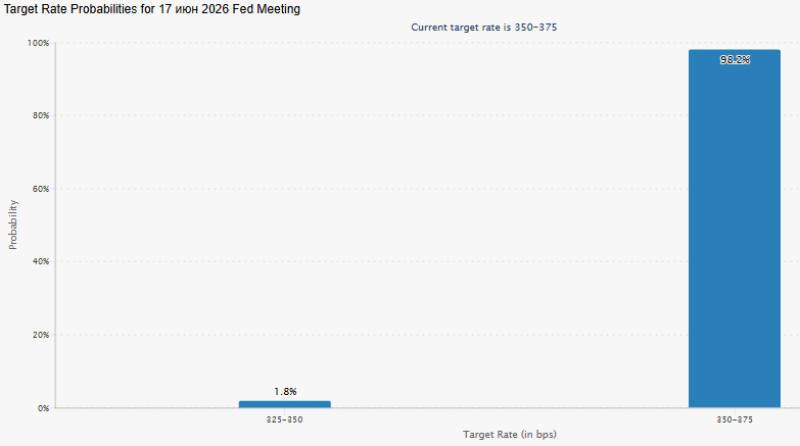

CME FedWatch data shows a 98.2% probability that the Federal Reserve will leave rates unchanged at its June 2026 meeting.

A 98.2% Vote for Patience

Current FedWatch data shows a 98.2% probability that policymakers will keep rates unchanged at the June meeting. Only 1.8% of market participants expect a cut. Several months ago, expectations were different. Investors anticipated a series of rate reductions through 2026.

The pricing has changed. Treasury traders now appear to be preparing for a slower path of monetary easing, which helps explain why short-term yields continue moving higher.

Growth Stocks Lose Part of Their Advantage

Technology companies are often the first to react when Treasury yields rise. Much of their valuation depends on profits expected years into the future. Higher yields reduce the present value of those future earnings.

That makes yield movements particularly relevant for companies such as Nvidia, Microsoft, Amazon and other firms tied to artificial intelligence and long-term growth themes. If Treasury yields continue rising, investors may become more selective about how much they are willing to pay for future growth.

Banks Are Playing a Different Game

Banks operate under a different set of dynamics. Higher yields can support lending margins and improve profitability in parts of the banking sector, especially when economic activity remains stable. The benefit is not automatic, but financial companies generally face less valuation pressure from rising yields than growth-oriented sectors. As a result, investors often rotate toward financial stocks during periods when Treasury markets reprice interest-rate expectations.

Treasuries Are Competing for Income Investors

Income investors compare opportunities across asset classes. When short-term Treasuries offer yields above 4%, government debt becomes a direct competitor to dividend-paying stocks. Utilities, real estate investment trusts and other income-focused sectors often feel the impact first. The comparison is straightforward: investors can earn a comparable yield from U.S. government securities without taking equity risk.

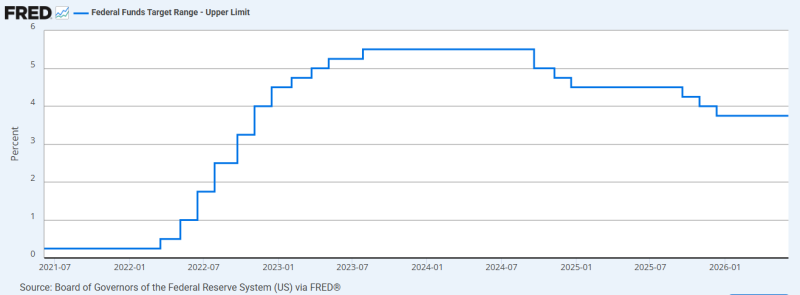

The Federal Funds Target Rate has already fallen from the 5.5% peak reached in 2023–2024 to approximately 3.75%, yet short-term Treasury yields are moving higher.

The Message Hidden Behind a 4.147% Yield

The Federal Reserve has already reduced rates substantially from the peak of the tightening cycle. The upper bound of the federal funds rate climbed to 5.50% in 2023 before gradually declining to around 3.75%.

Under normal circumstances, lower policy rates would ease pressure on short-term Treasury yields. Instead, the two-year yield has climbed to its highest level in more than a year. That divergence points to changing expectations among investors. Inflation remains a concern, economic data has stayed relatively firm, and confidence in rapid rate cuts has weakened.

The market is no longer debating whether rates have peaked. The debate has shifted to how long they will remain elevated.

Where the Pressure Could Show Up First

The next move in Treasury yields may matter more than the next move in the federal funds rate itself. If short-term yields continue rising, pressure on technology and income-oriented sectors could increase. Financial stocks may remain comparatively resilient.

The message from the Treasury market is clear: investors are demanding higher compensation to lend money to the U.S. government, even after the Federal Reserve has already started lowering rates. That is not the behavior of a market expecting cheap money to return anytime soon.

Artem Voloskovets

Artem Voloskovets