Marina Lubimova

Marina Lubimova

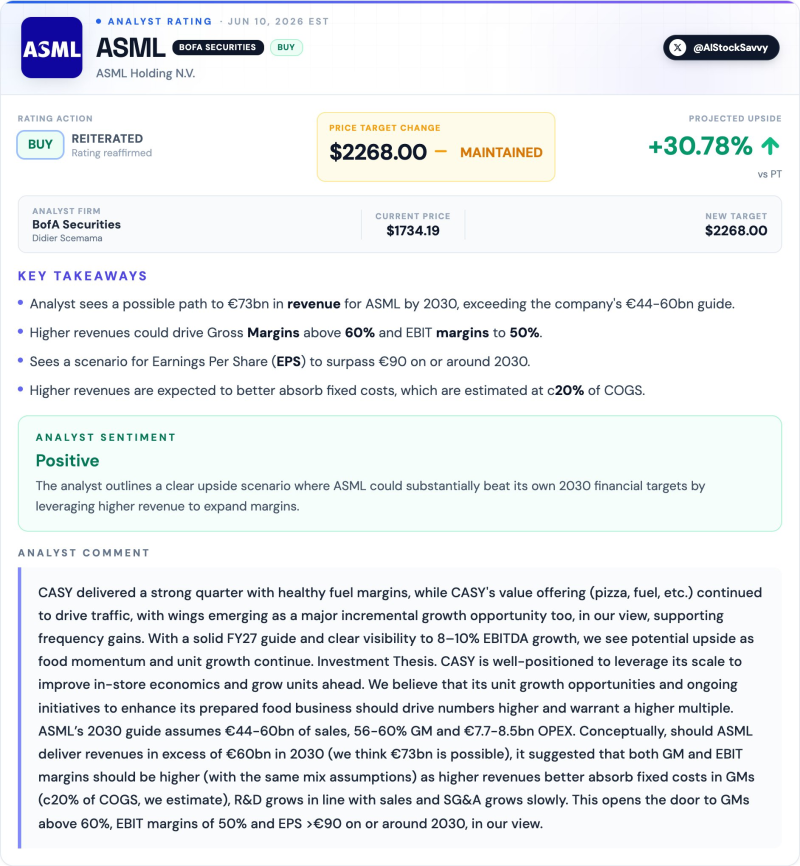

The bank reiterated its Buy rating and maintained a $2,268 price target, implying roughly 31% upside from the current share price of $1,734. More importantly, analysts outlined a scenario in which ASML generates approximately €73 billion in annual revenue by 2030, exceeding the company's official guidance range of €44–60 billion.

The gap between those numbers raises a broader question: what would have to happen for ASML to outperform its own expectations?

The Starting Point

ASML enters the second half of the decade from a position of financial strength.

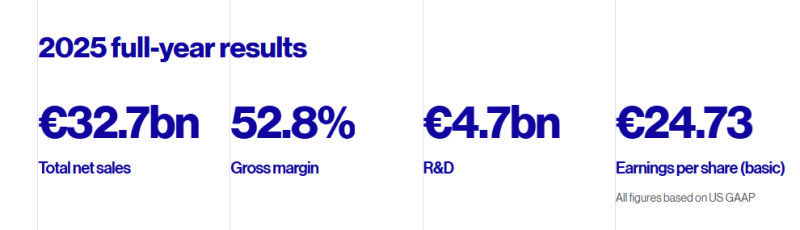

Its 2025 results showed:

- €32.7 billion in net sales

- 52.8% gross margin

- €4.7 billion in R&D spending

- €24.73 earnings per share

ASML 2025 Full-Year Results

- Revenue: €32.7bn

- Gross Margin: 52.8%

- R&D: €4.7bn

- EPS: €24.73

These figures matter because they establish the baseline from which future growth will be measured. To reach €73 billion in annual revenue, ASML would need to more than double its current sales within five years.

Beyond the Company's Own Forecast

Management's long-term outlook calls for annual revenue between €44 billion and €60 billion by 2030. Bank of America's estimate sits significantly above that range.

2030 Revenue Scenarios

| Scenario | Revenue |

| ASML Guidance (Low) | €44bn |

| ASML Guidance (High) | €60bn |

| BofA Scenario | €73bn |

The difference is not simply a matter of stronger sales. It reflects a view that demand for advanced semiconductor manufacturing equipment may remain elevated for longer than management currently assumes.

For ASML, even modest changes in industry spending can have an outsized impact because of the company's dominant position in lithography systems.

Where the Earnings Expansion Comes From

The most important part of BofA's thesis is not revenue. It is margin expansion. According to the bank, higher volumes would allow ASML to absorb fixed costs more efficiently. Analysts estimate those fixed costs account for roughly 20% of cost of goods sold. That creates a straightforward operating leverage story.

Under BofA's assumptions:

- Gross margins could exceed 60%

- EBIT margins could approach 50%

- Earnings growth could outpace revenue growth

The comparison with current results is notable. Gross margin was already 52.8% in 2025. A move beyond 60% would place ASML among the most profitable large-scale industrial technology companies globally.

The EPS Projection That Changes the Equation

Bank of America sees a path toward earnings per share exceeding €90 by 2030. That compares with €24.73 reported in 2025.

EPS Scenario

| Year | EPS |

| 2025 | €24.73 |

| 2030 (BofA Estimate) | €90+ |

The significance of that forecast is not the number itself. It is what it implies about the business. Revenue would be growing, margins would be expanding, and a larger share of each additional euro of sales would reach the bottom line. In other words, the earnings story becomes more powerful than the revenue story.

What the Stock's History Suggests

ASML's long-term share-price performance provides context for why analysts continue to focus on the company.

ASML Share Price Since 2010

Use the supplied long-term stock chart.

Key observations:

- Shares rose from roughly $40 in 2010 to more than $1,600 in 2025.

- The stock delivered gains exceeding 4,000%.

- Major advances were typically linked to increases in semiconductor capital spending.

The chart also highlights another pattern: ASML's strongest periods have often occurred when industry demand exceeded prevailing expectations. That is effectively the argument behind BofA's latest outlook.

A Different Way to Read the Forecast

Most discussions around price targets focus on the target itself. The more relevant takeaway may be the assumptions underneath it. For ASML to generate €73 billion in annual revenue, the semiconductor industry would need to continue investing heavily in manufacturing capacity throughout the decade. Higher volumes would then improve cost absorption, pushing margins above historical levels and creating a disproportionate increase in earnings.

Viewed through that lens, the forecast is less about a price target and more about the possibility that ASML's current long-term guidance understates the earnings potential of the business.

Marina Lubimova

Marina Lubimova