Marina Lubimova

Marina Lubimova

That was expected. The more important detail was buried in the ECB's statement. Policymakers refused to commit to a future rate path, leaving the door open for additional tightening if inflation remains elevated.

The IMF took the same position, warning that more rate hikes may still be necessary after Thursday's decision. The debate is no longer about this rate increase. It is about whether inflation is becoming a bigger problem than policymakers anticipated.

But Inflation Is Moving in the Wrong Direction

The ECB now expects inflation to average 3.0% in 2026, 2.3% in 2027 and only return to its 2% target in 2028. Recent Eurostat data shows the trend is moving away from that target rather than toward it.

Inflation bottomed at 1.7% in January and has climbed every month since. Energy prices remain the main driver, but core inflation is also expected to average 2.5% next year. That leaves little room for the ECB to declare victory.

The Economy Is Already Slowing

While inflation accelerates, growth is weakening.

The latest eurozone data shows:

- Inflation: 3.2%

- GDP growth (Q1 2026): -0.2%

- Unemployment: 6.3%

The ECB has already cut its growth outlook for 2026 to 0.8%.

| Indicator | Value |

| Inflation | 3.2% |

| GDP Growth | -0.2% |

Higher rates normally slow demand and reduce inflation. The problem is that economic activity is already contracting while inflation remains well above target. That combination limits the ECB's options.

Markets Don't Believe the ECB Story

If investors expected a long series of additional rate hikes, the euro would likely have strengthened after the announcement.

Instead, EUR/USD fell.

The move suggests investors are paying more attention to growth risks than to higher rates. Bond markets sent a similar signal.

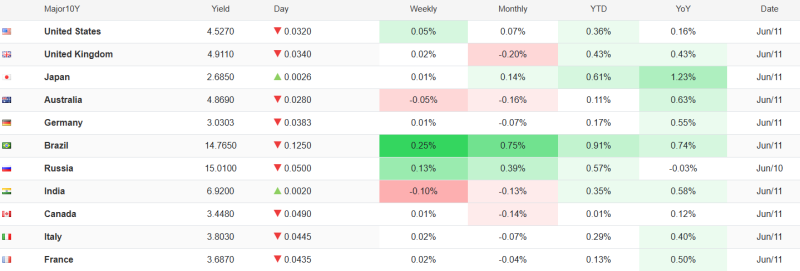

| Country | 10Y Yield | Daily Change |

| Germany | 3.03% | -0.038 |

| France | 3.69% | -0.044 |

| Italy | 3.80% | -0.045 |

Falling yields typically reflect expectations of weaker growth and lower long-term inflation pressure. That is not the market reaction associated with a new tightening cycle.

The Stagflation Risk Nobody Wants to Discuss

Europe is not facing classic inflation. It is facing inflation that is rising while growth slows. Inflation has increased from 1.7% to 3.2% in four months. GDP has already turned negative. Energy prices remain volatile, and the ECB expects the impact of higher commodity costs to continue.

This is the environment central banks struggle with most. Raising rates risks worsening the slowdown. Pausing too early risks allowing inflation to become entrenched. Neither choice is attractive.

Why IMF Could Be Right — and Why That Matters

The IMF's warning is based on one assumption: inflation will remain stubborn. The ECB's own forecasts support that view. Inflation is projected above target for the next two years, while core inflation remains elevated.

If those forecasts prove accurate, policymakers may have to keep rates higher for longer than markets expect. That would increase borrowing costs for households, businesses and governments at a time when growth is already losing momentum. The consequence would not be another rate hike. It would be a longer period of weak growth combined with restrictive monetary policy.

Marina Lubimova

Marina Lubimova