Marina Lubimova

Marina Lubimova

The debate usually focuses on whether there is enough oil to offset potential supply disruptions. The more important question is where that spare capacity sits. Today, most of the world's emergency oil buffer is concentrated in just a handful of countries. At the same time, economic growth is already slowing across major economies, leaving markets with less room to absorb another energy shock.

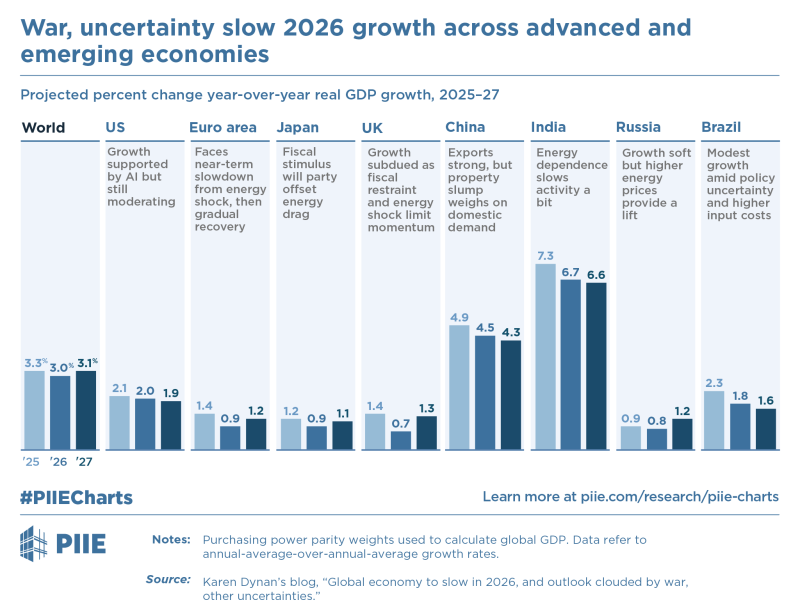

Growth Was Weakening Before Any Major Supply Crisis

The Peterson Institute for International Economics (PIIE) shows that global GDP growth is expected to slow from 3.3% in 2025 to 3.0% in 2026. The slowdown is visible across both developed and emerging markets.

U.S. growth is forecast to ease from 2.1% to 2.0%. The euro area is expected to expand by just 0.9%, while UK growth falls to 0.7%. China slows from 4.9% to 4.5%. India remains the fastest-growing major economy but is still projected to decelerate from 7.3% to 6.7%.

These are not recession numbers. But they do show an economy entering 2026 with less momentum than it had a year earlier. That matters because slower economies are more vulnerable to commodity shocks.

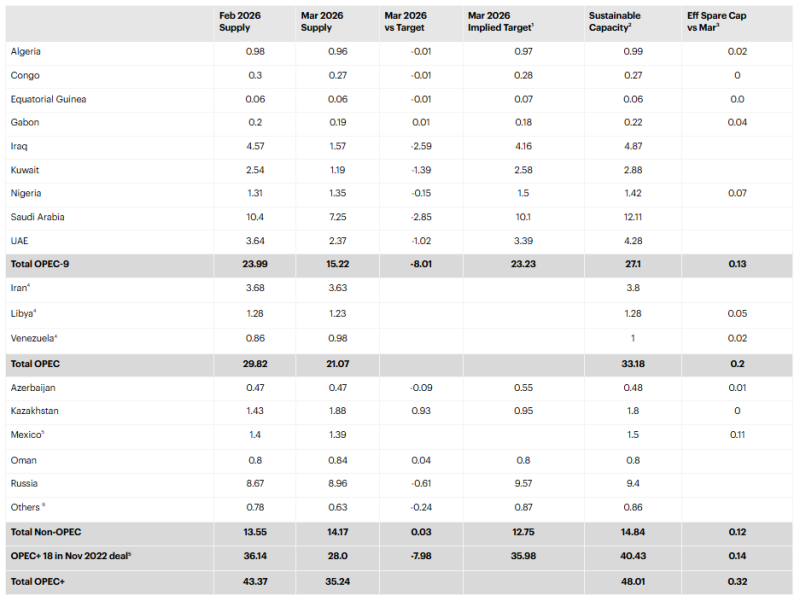

OPEC+ Has Plenty of Spare Capacity on Paper

At first glance, the oil market looks well protected. OPEC+ sustainable production capacity stands at 48.01 million barrels per day, while current output is 35.24 million barrels per day. That suggests nearly 13 million barrels per day of unused capacity. The headline number, however, hides a much more concentrated reality.

Saudi Arabia alone has sustainable capacity of 12.11 million barrels per day but currently produces around 7.25 million. The UAE can produce 4.28 million barrels per day while currently pumping 2.37 million. Those two countries account for the overwhelming majority of immediately available supply.

The Rest of OPEC+ Has Very Little Room Left

Outside the Gulf producers, spare capacity becomes surprisingly thin. Algeria has roughly 20,000 barrels per day available. Nigeria has around 70,000 barrels. Libya has approximately 50,000 barrels. Several members effectively have no spare production left at all.

This means that what appears to be a diversified supply cushion is actually a highly concentrated one. The market is not relying on OPEC+ as a group. It is relying primarily on Saudi Arabia and the UAE.

Why This Matters for Growth

The PIIE forecasts show an economy already losing speed before any major oil disruption occurs. Europe is barely growing. China is slowing. India remains strong but is becoming more energy-dependent as industrial demand rises.

If a geopolitical event removes significant supply from the market, the burden of stabilization falls on a very small number of producers. That creates a different type of risk than a traditional supply shortage. The issue is not whether spare capacity exists. The issue is whether enough capacity can be mobilized quickly enough if markets suddenly need it.

Markets Are Pricing Supply. They May Be Underpricing Concentration.

Oil traders typically focus on total production, inventories, and demand forecasts. The latest OPEC+ figures suggest another metric deserves attention: concentration risk. Global growth forecasts already point to slower expansion in 2026. At the same time, most of the oil market's emergency buffer sits in two Gulf states. As long as that buffer remains available, the market can absorb shocks. The closer it gets to being tested, the more important its concentration becomes.

Marina Lubimova

Marina Lubimova