Artem Voloskovets

Artem Voloskovets

A 3% increase in oil prices does not usually trigger concern about the global economy. A change of that size is often dismissed as normal market volatility. Yet the latest energy forecasts suggest investors may be looking at the wrong number.

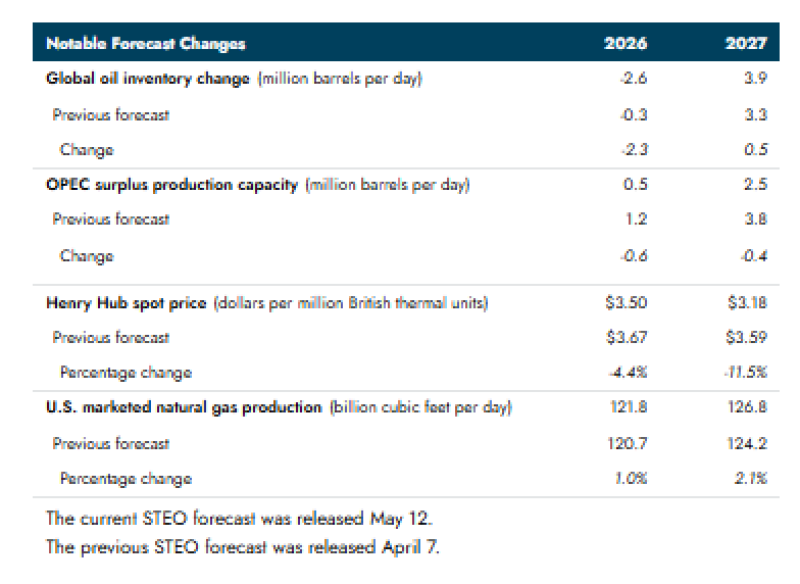

The real development is happening beneath the surface of the oil market. In its latest Short-Term Energy Outlook, the U.S. Energy Information Administration dramatically revised its expectations for global oil inventories. Just a month ago, the agency expected inventories to decline by only 0.3 million barrels per day in 2026. It now expects a drawdown of 2.6 million barrels per day.

That is not a marginal adjustment. It is a signal that the market could be tightening much faster than policymakers and investors anticipated earlier this spring. At the same time, global oil prices are running roughly 3% above the assumptions used in April's baseline forecast for 3.1% global economic growth. Neither figure is alarming on its own. Together, they deserve attention.

The Inventory Revision Is the Real Story

Oil markets rarely move because of today's supply. They move because traders start reassessing future supply. The EIA's latest forecast suggests that the expected decline in global inventories for 2026 is now more than eight times larger than previously projected.

- Global Oil Inventory Change: 2026

- Previous Forecast: -0.3 mb/d

- Latest Forecast: -2.6 mb/d

A drawdown of this size does not mean the world is running out of oil. It does mean there is less room for error.

When inventories fall quickly, markets become more sensitive to unexpected disruptions. A production outage, geopolitical conflict, refinery issue, or shipping bottleneck can have a larger impact on prices because fewer запасов remain available to absorb shocks.

That is how relatively small price increases can become more significant macroeconomic signals.

What the Futures Market Is Actually Saying

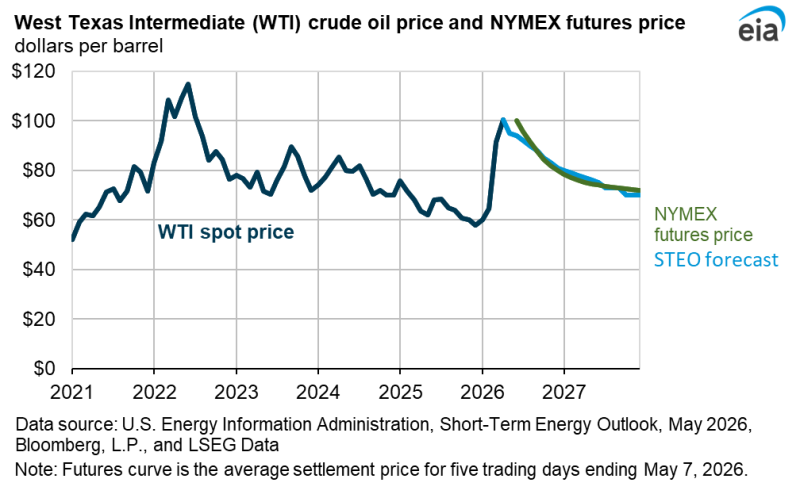

Interestingly, the futures market is not forecasting permanently high oil prices. According to EIA data, WTI crude briefly approached $100 per barrel during the latest rally. However, both NYMEX futures and the agency's own forecast point toward a gradual decline over the next two years.

The projected path looks roughly like this:

- Around $100 per barrel in mid-2026

- Around $80 by early 2027

- Near $70–72 by the end of 2027

The market is therefore not pricing an energy crisis. It is pricing a temporary period of tightness. That distinction matters because investors often confuse high prices with structural shortages. Current futures pricing suggests traders still expect additional supply, weaker demand growth, or both. The question is whether those expectations prove correct.

Why Growth Forecasts Become More Fragile

Economic forecasts are built on assumptions. If oil prices remain above those assumptions for long enough, the consequences spread beyond the energy sector.

Transport becomes more expensive. Manufacturing costs rise. Import-dependent economies face larger energy bills. Consumer spending power weakens as fuel and logistics costs work their way through the economy.

None of these effects immediately derail global growth. But they reduce the margin for error. The current debate is not whether a 3% increase in oil prices will destroy the 3.1% growth forecast. It will not.

The more important question is whether tighter inventories make further price increases more likely later in the year. If inventory drawdowns continue at the pace now projected by the EIA, the next move in oil could matter far more than the first 3%.

The Signal Investors Should Watch

The most important number in the latest outlook is not the oil price. It is the inventory forecast. Prices tell investors what happened. Inventories often provide clues about what could happen next.

For now, futures traders are betting that the current tightness fades and prices gradually retreat toward the low $70s. The latest inventory projections suggest the market may have less breathing room than that scenario assumes.

That does not guarantee higher oil prices. It does mean the risk is no longer coming from today's crude market. It is coming from how quickly the global supply cushion is shrinking underneath it.

Artem Voloskovets

Artem Voloskovets