Artem Voloskovets

Artem Voloskovets

Consumers are not expecting stronger wage growth. They are not expecting a spending boom. Markets barely reacted. The disconnect suggests that households see inflation settling above the Fed's target without reigniting the forces that drove prices sharply higher in recent years.

Inflation Expectations Stay Elevated

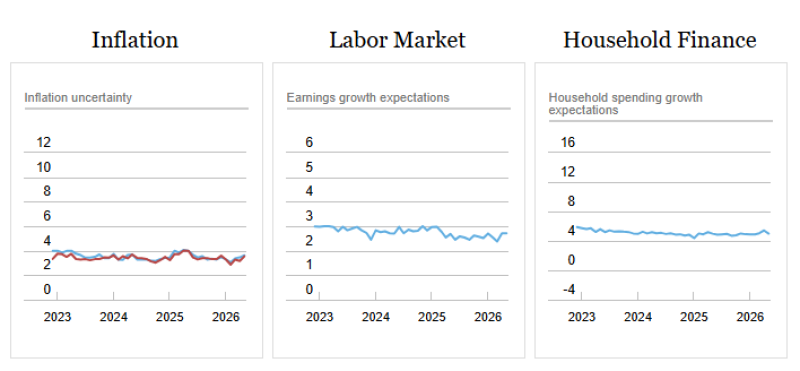

Five-year inflation expectations held at 3.0% in May. More notable than the level is the lack of movement. Inflation uncertainty has remained broadly stable, with no sign of a renewed surge in concern about future price growth.

Stable expectations matter more than the difference between 2% and 3%. Rising expectations can fuel higher wages, stronger spending, and ultimately higher inflation. The latest survey does not show that dynamic.

Spending Expectations Are Going Nowhere

Household spending growth expectations remain close to 4%, where they have spent most of the past two years.

Consumers still expect spending to grow, but there is no acceleration. If households believed another inflation wave was approaching, spending expectations would likely be moving higher as people rushed purchases forward. That is not happening. The survey points to steady demand rather than overheating demand.

Wage Growth Expectations Remain Contained

The labor market data tells a similar story. Expected earnings growth remains around 2.5% to 3.0%, with only minor month-to-month fluctuations.

Higher inflation becomes harder to control when workers expect larger pay increases and businesses pass those costs on to consumers. Current expectations do not suggest that cycle is building. Consumers appear to expect modest income growth and a labor market that continues to cool gradually rather than abruptly.

The Dollar Barely Moved

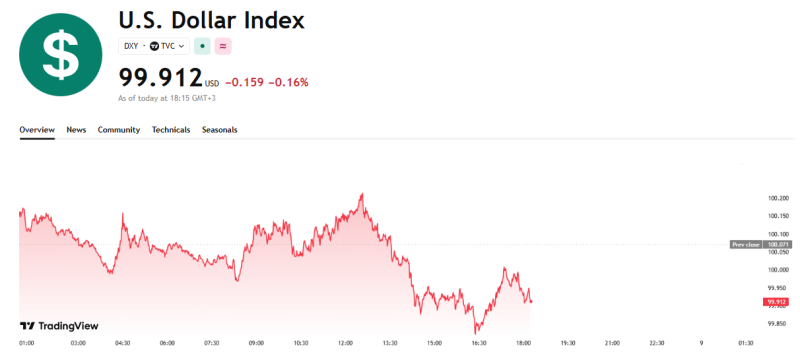

Financial markets treated the report as a non-event. The U.S. Dollar Index traded near 99.91 after the release, down roughly 0.16% on the day.

The move suggests investors saw nothing in the survey that changes the interest-rate outlook. A report showing rising inflation expectations, stronger spending plans, or accelerating wage expectations would likely have triggered a larger reaction across currencies and bond markets. Instead, the data reinforced existing assumptions.

What the Survey Actually Says

The headline number is 3%. The more important takeaway is that consumers expect 3% inflation without expecting the behavior that typically keeps inflation rising. Spending plans are stable. Wage expectations are stable. Inflation uncertainty is stable.

That combination helps explain why markets paid little attention to the report and why the Federal Reserve is unlikely to view the survey as evidence of renewed inflation pressure.

Artem Voloskovets

Artem Voloskovets