Marina Lubimova

Marina Lubimova

The decline itself is relatively small, but it comes as several housing indicators suggest that the improvement seen over the past year is beginning to lose momentum.

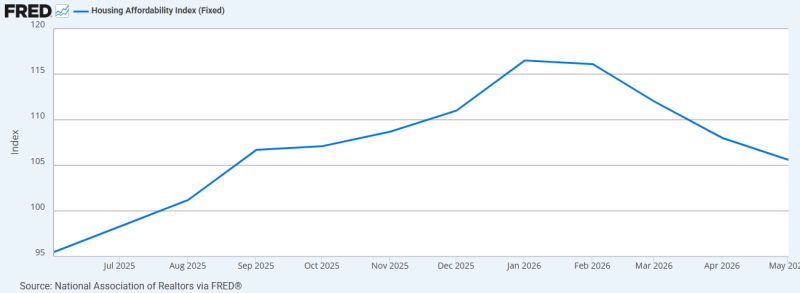

The affordability trend has shifted noticeably. The National Association of Realtors' Housing Affordability Index rose from roughly 95 in June 2025 to a cycle high of 116 in January 2026, reflecting stronger household purchasing power as incomes gradually caught up with financing costs.

That recovery has since stalled. The index eased to about 116 in February, dropped to 112 in March, slipped again to around 108 in April, and reached approximately 105 in May.

The reversal matters because affordability typically drives mortgage demand. As monthly payments consume a larger share of household income, more buyers postpone purchases or lower their budgets. Even without a surge in mortgage rates, weaker affordability reduces the number of households that can comfortably qualify for a loan.

Mortgage applications tend to lead housing activity by several weeks, making them one of the earliest signals of changes in buyer sentiment.

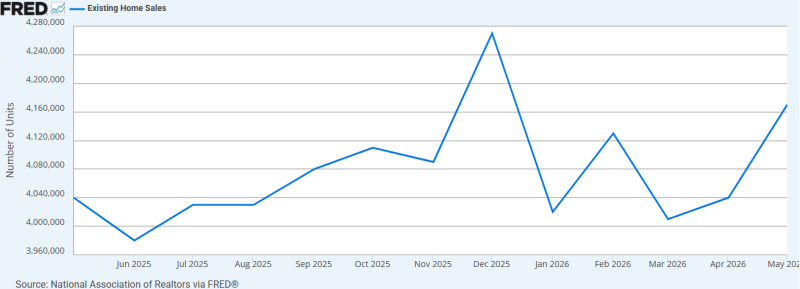

Completed transactions tell a more balanced story. Existing home sales have remained close to an annualized pace of 4 million units despite elevated borrowing costs. Sales climbed to approximately 4.26 million in December 2025 before falling to about 4.01 million in January. Activity recovered to roughly 4.12 million in February, softened again in March, and then accelerated to nearly 4.16 million units in May.

The gap between applications and completed sales reflects a market that continues to function, but with less flexibility. Buyers are still purchasing homes, yet financing decisions have become far more sensitive to affordability than during the low-rate environment of previous years.

Supply constraints reinforce that pattern. Many homeowners remain locked into mortgages originated during 2020–2022 at historically low interest rates, reducing their incentive to sell. Limited inventory has helped support home prices even as mortgage demand fluctuates from week to week.

The latest MBA figures therefore point to a housing market that is slowing at the margin rather than contracting sharply. Sales remain relatively stable, but declining affordability is beginning to weigh on new borrowing. Unless financing costs ease or household income growth accelerates, mortgage demand is likely to remain uneven through the second half of the year.

Marina Lubimova

Marina Lubimova