Marina Lubimova

Marina Lubimova

That shift has consequences beyond the currency market. Cheaper hedging, lower risk premiums and greater confidence in the macro outlook all influence how investors allocate capital. At the same time, markets that price in very little uncertainty often become more sensitive to unexpected news.

A Currency Pair Trading Without Conviction

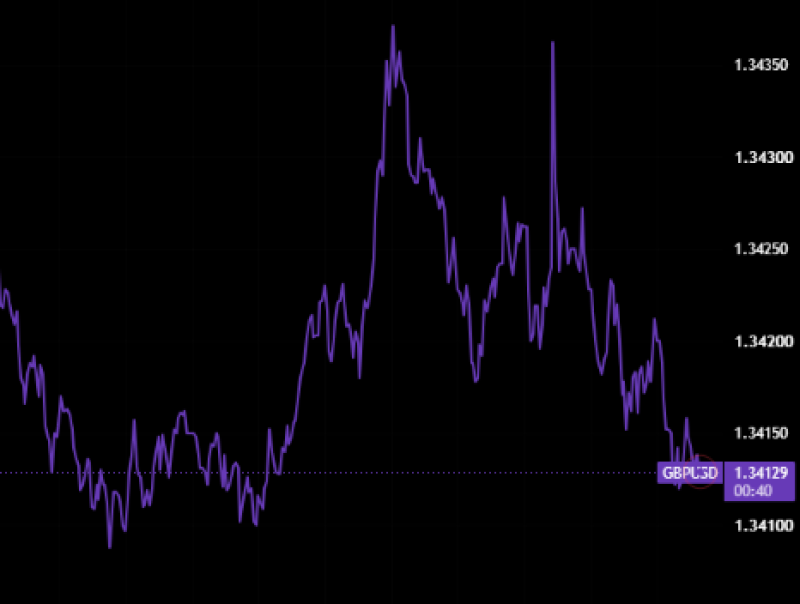

GBP/USD remained largely confined to the 1.341–1.343 range despite continued macroeconomic news.

Recent price action reflects the collapse in implied volatility. Sterling continues to attract steady buying and selling interest, yet neither bulls nor bears have been able to establish a lasting trend. Instead of directional moves, the market has settled into short-lived fluctuations around the 1.3420 area.

This type of price behavior naturally reduces demand for options. When realized volatility remains subdued, investors become less willing to pay high premiums for protection against future moves.

Policy Is No Longer the Main Source of Uncertainty

UK interest rates remain restrictive while inflation has moved significantly closer to the Bank of England's target.

The Bank of England's Bank Rate stands at 3.75%, while UK inflation has slowed to 2.8%, only modestly above the official 2% target. The contrast with the past three years is significant.

Markets are no longer trying to price emergency tightening cycles or rapidly changing inflation forecasts. Instead, investors expect policy adjustments to become incremental, reducing the likelihood of abrupt shifts in interest-rate expectations.

The same transition is taking place in the United States. As both central banks move toward a slower policy cycle, one of the largest historical drivers of GBP/USD volatility has gradually faded.

Trading Activity Has Not Disappeared

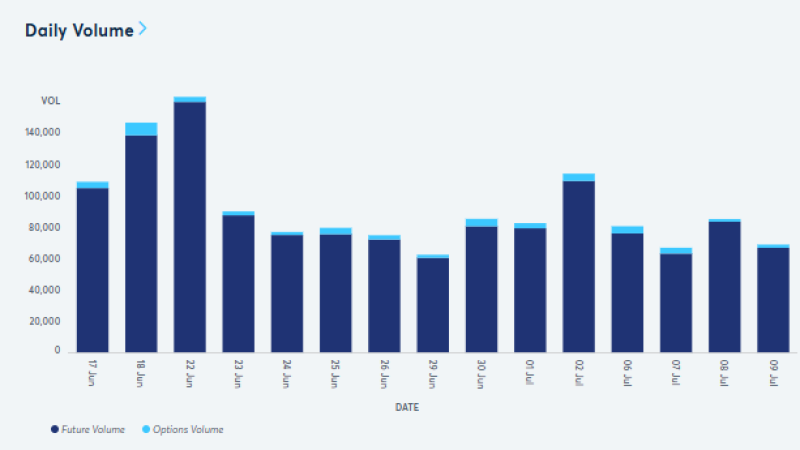

Futures and options activity remains elevated despite record-low implied volatility.

Lower volatility has not translated into lower participation. CME data show futures and options volumes remaining consistently active. Daily turnover exceeded 150,000 contracts during late June and generally fluctuated between 70,000 and 110,000 contracts throughout early July.

That distinction matters. Investors continue to trade sterling actively; they are simply paying far less to insure against large price movements. In other words, liquidity remains healthy even as expectations for future volatility continue to decline.

Cheap Protection Can Encourage Complacency

Periods of low implied volatility often reinforce themselves. As hedging costs decline, investors become more comfortable holding larger positions. Risk models allocate less capital to potential losses, volatility-selling strategies become more attractive, and demand for downside protection continues to weaken.

The result is a market that appears increasingly stable while becoming more dependent on that stability continuing.

This dynamic explains why volatility regimes can reverse quickly. When expectations become concentrated around a single macroeconomic narrative, even relatively modest surprises can trigger disproportionate price adjustments.

Stability Is Now the Consensus Trade

The options market is effectively pricing a world in which inflation continues to moderate, central banks avoid major policy surprises, and interest-rate differentials evolve gradually rather than abruptly.

That consensus explains why one-year GBP/USD implied volatility has fallen to its lowest level in more than five years. Whether it remains justified is another question.

A renewed inflation shock, unexpected policy guidance from either the Bank of England or the Federal Reserve, weaker growth, or geopolitical developments could all force investors to reassess today's unusually calm outlook.

The significance of 6.9275% is therefore not that sterling has become inherently safer. It is that the market has become increasingly confident that the next twelve months will look much like the last few weeks, a view that financial markets have repeatedly shown can change far faster than expected.

Marina Lubimova

Marina Lubimova