Artem Voloskovets

Artem Voloskovets

The latest data from the Japanese yen market point to exactly that situation. Leveraged funds have rebuilt one of the largest bearish positions in nearly twenty years, while trading activity in CME futures and options has accelerated. Neither development says where the yen will trade next. Together, they reveal a market becoming increasingly dependent on a single macro narrative.

A Consensus That Has Already Been Priced

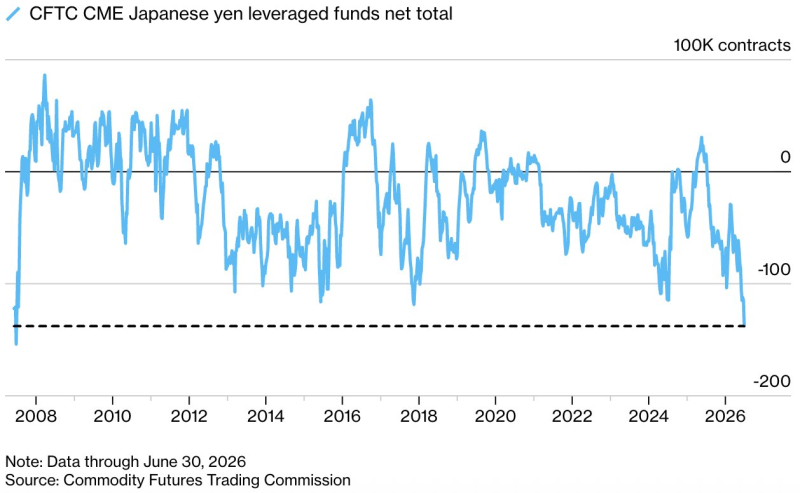

Leveraged funds' net position has fallen to roughly -140,000 contracts, returning to levels last seen during previous episodes of extreme bearish sentiment. Over the past eighteen years, positioning has rarely remained this negative for long without triggering periods of heightened volatility.

Positioning data answers a different question than price. Exchange rates show what has happened. Positioning shows how many investors have already committed to expecting more of the same.

The prevailing narrative remains familiar. U.S. interest rates continue to exceed Japanese yields by a wide margin, the Federal Reserve maintains relatively restrictive policy, and the Bank of Japan continues to normalize cautiously. As long as this interest-rate gap persists, borrowing yen to finance investments elsewhere remains attractive.

That story is already well understood. The positioning data suggest it has also become widely owned.

Trading Activity Is Picking Up

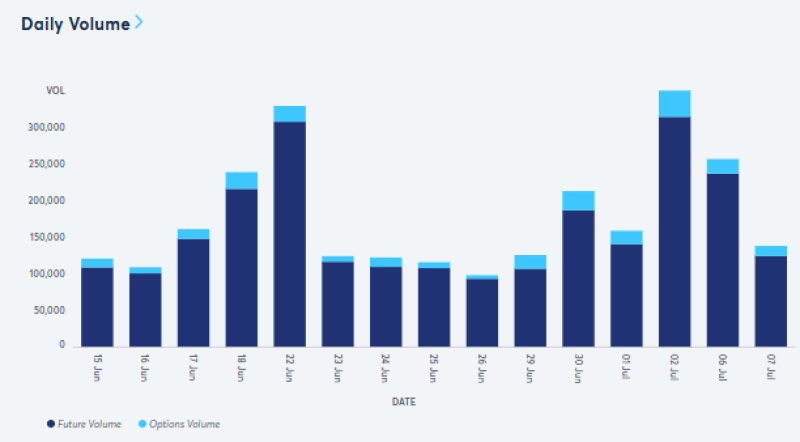

Market participation has increased alongside bearish positioning. Daily turnover exceeded 300,000 combined contracts during the busiest session in early July, while several other trading days approached or surpassed 250,000 contracts. Even quieter sessions remained comfortably above 100,000 contracts, highlighting sustained participation instead of a one-day spike.

The composition of that activity is equally important. Options volume expanded together with futures volume rather than remaining flat. Directional exposure is increasing, but so is demand for protection. Investors continue expressing conviction while allocating more capital to hedging potential volatility. That combination typically reflects growing uncertainty, not growing confidence.

Crowded Trades Obey Different Rules

A crowded position does not become dangerous because the underlying thesis suddenly fails. It becomes dangerous because market balance changes. When most participants already share the same view, additional selling power gradually disappears. New information no longer needs to overturn the macro narrative to move prices. It only needs to challenge expectations enough for investors to reduce risk simultaneously.

A modest decline in Treasury yields, a more hawkish signal from the Bank of Japan, renewed speculation about currency intervention or softer U.S. inflation could all force the same trade to unwind at once.

Liquidity becomes thinner precisely when everyone believes they are positioned correctly. This pattern has appeared repeatedly across asset classes. Technology stocks in the late 1990s, volatility-selling strategies before the 2018 volatility shock, and leveraged bond trades during the UK pension crisis all shared one characteristic: concentration. The investment thesis survived longer than many expected. The positioning did not.

The Market Is Preparing for Movement

The two charts describe different aspects of the same environment. One shows speculative positioning approaching historical extremes. The other shows participation accelerating as those positions become increasingly concentrated. Neither chart argues that the yen is about to reverse. Both suggest that market sensitivity is rising. Large directional bets supported by expanding trading volumes often create conditions where future price moves are driven less by new economic information and more by portfolio adjustments, liquidity, and risk management. Consensus gradually becomes the market's largest source of risk.

Why Positioning Deserves Attention

Economic data explain why investors entered the trade. Positioning reveals how much room remains for that trade to expand. Those are separate questions.

The Japanese yen has become one of the clearest examples of this distinction. Bearish positioning has approached -140,000 contracts, while daily trading activity has repeatedly climbed toward 300,000–330,000 contracts.

Neither figure predicts the next move in the currency. Together, however, they show a market where conviction has become unusually concentrated and participation continues to grow. That combination rarely eliminates uncertainty. More often, it magnifies the market's reaction when uncertainty finally arrives.

Artem Voloskovets

Artem Voloskovets