Artem Voloskovets

Artem Voloskovets

It made Japanese exports cheaper abroad, lifted overseas earnings when converted back into yen, and supported the image of Japan as an industrial powerhouse. That logic still exists, but it is weaker than before.

With the yen falling to 161.97 per dollar, its weakest level since 1986, Japan is facing a harder question: how much currency weakness can the economy absorb before the costs outweigh the benefits?

The yen’s decline is no longer temporary

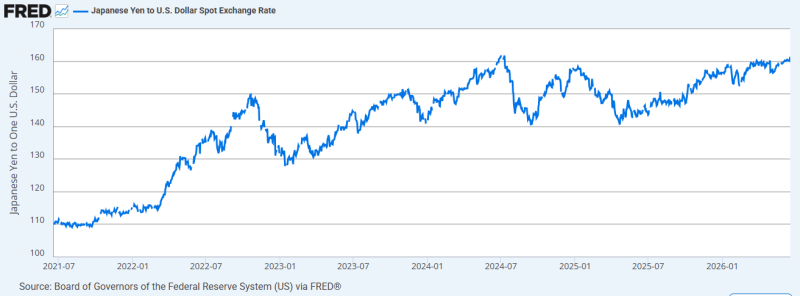

The chart shows a clear break from the pre-2022 range. In mid-2021, one dollar bought roughly 109 yen. Now it buys nearly 160 yen. That is a rise of about 46% in USD/JPY.

The important detail is not only the size of the move. It is the persistence. Each pullback, in late 2022, mid-2024, and early 2025, failed to change the trend. The pair kept returning toward new highs. This makes the weak yen less of a market episode and more of a new operating condition for Japan.

Export gains are narrower than they used to be

A cheaper yen still helps large exporters. Foreign sales become more valuable in yen terms. Reported profits improve. Global manufacturers get some pricing flexibility. But Japan’s economy is not the same export machine it was in the 1980s. Many companies now produce closer to their customers. Supply chains are more global. Imported energy, parts, food, and materials are built into the cost structure of the whole economy. That means the benefit is concentrated, while the cost is spread widely.

The pressure lands on households first

The weak yen makes imports more expensive. That matters because Japan relies heavily on imported fuel, food, and raw materials. When the currency falls, the price shock moves quickly into electricity bills, gasoline, groceries, and business costs. For households, the exchange rate is no longer a financial-market abstraction. It shows up in daily prices.

Wage growth has improved, but not enough to make currency-driven inflation painless. The result is a squeeze that feels especially sharp in a country used to decades of low inflation.

The Bank of Japan has no clean option

The rate gap explains much of the yen’s weakness. U.S. rates remain far above Japanese rates, making dollar assets more attractive. Investors can borrow cheaply in yen and move money into higher-yielding dollar instruments. The Bank of Japan can raise rates to defend the currency, but that risks hitting domestic demand, mortgages, corporate borrowing, and government financing costs.

It can also move slowly, but then the yen remains exposed. This is the core dilemma: the policy that supports the economy also weakens the currency.

Intervention can interrupt the move, not reverse it

Japan has stepped into the currency market before. The chart should show the sharp drops in USD/JPY around intervention periods, followed by the market’s return toward higher levels. That pattern matters. Intervention can punish short-term speculation and slow disorderly moves. But it cannot erase the reason investors prefer dollars: the yield gap. Without a change in rates, intervention buys time rather than a new trend.

The real risk is a weaker domestic economy

The biggest danger is not the number 161.97 itself. It is the feedback loop behind it. A weak yen raises import costs. Higher costs pressure households. Weaker household demand limits growth. Slower growth makes aggressive rate hikes harder. Low rates keep the yen under pressure.

That loop is difficult to break. It also changes the politics of the currency. A weak yen used to be discussed mainly through exporters and markets. Now it is increasingly a cost-of-living issue.

Conclusion

Japan’s weak yen is no longer just good news for exporters or bad news for currency traders. It has become a national economic trade-off. A cheaper currency still supports some corporate profits, but it also imports inflation, squeezes households, and limits the Bank of Japan’s room to maneuver.

That is why the yen’s fall to 161.97 per dollar matters. It shows that Japan’s old currency model- weak yen, strong exporters, manageable domestic costs — no longer works as cleanly as it once did.

Artem Voloskovets

Artem Voloskovets