Artem Voloskovets

Artem Voloskovets

As the Federal Reserve keeps interest rates well above those in Japan, global capital continues flowing toward dollar-denominated assets, lifting the U.S. currency to 161.93 yen, its strongest level in nearly two years. The exchange rate itself is only part of the story. More important is what it reveals about global liquidity, capital allocation and the growing divergence between the world's two largest developed economies.

Higher U.S. Yields Continue to Redirect Global Capital

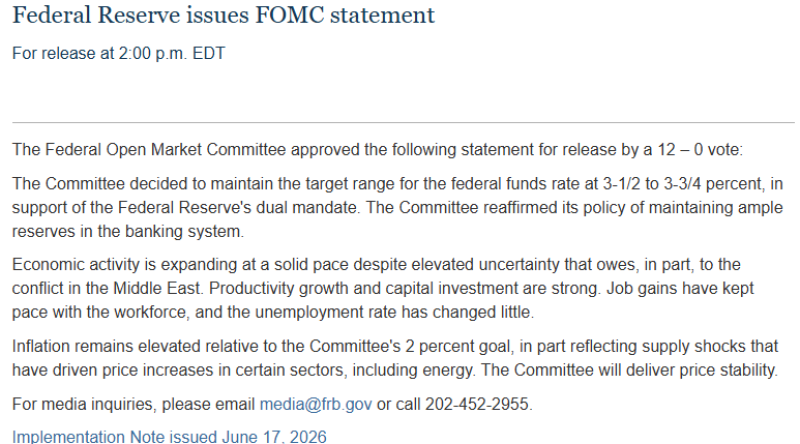

The Federal Reserve left the federal funds rate unchanged at 3.50%–3.75%, but the accompanying statement reinforced the market's higher-for-longer narrative.

Officials acknowledged that inflation remains above target while describing economic activity as expanding at a solid pace and labor-market conditions as resilient. Taken together, those signals suggest that U.S. interest rates are likely to remain restrictive for longer than markets expected only a few months ago.

Insert the supplied FOMC statement image. Suggested caption The Federal Reserve maintained rates at 3.50%–3.75% while reiterating that inflation remains elevated and economic activity continues to expand. Higher policy rates continue to support Treasury yields, making U.S. assets increasingly attractive relative to most developed markets. Currency appreciation is becoming a consequence of that capital migration rather than its primary driver.

Cheap Yen Funding Is Fueling Global Risk Allocation

Japan remains on the opposite side of the policy spectrum. Although the Bank of Japan has gradually moved away from ultra-loose monetary policy, domestic interest rates remain well below U.S. levels. That gap continues to make the yen one of the cheapest funding currencies in global markets.

Borrowing in yen to purchase higher-yielding overseas assets, the classic carry trade, becomes increasingly attractive as long as exchange-rate volatility remains contained. The wider the yield differential becomes, the stronger the incentive to finance global investments with inexpensive Japanese capital while accumulating dollar assets.

Investors Are Buying Yield, Not Dollars

The current rally is often described as dollar strength. A more accurate description is that investors continue to favor higher real returns.

Dollar demand reflects the premium offered by U.S. fixed-income markets rather than a purely directional view on the currency itself. As long as Treasury yields remain substantially above Japanese government bond yields, the dollar remains the preferred destination for international capital.

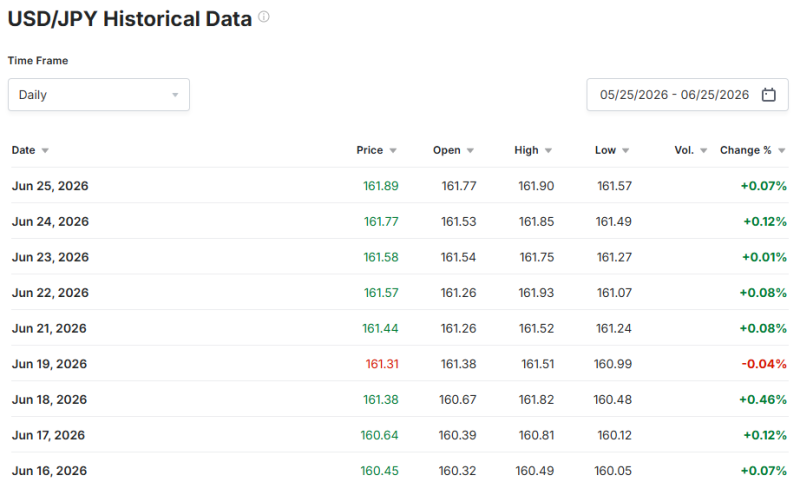

That relationship explains why USD/JPY has continued climbing despite repeated discussions about possible intervention by Japanese authorities. Use the supplied USD/JPY chart.

USD/JPY has advanced steadily throughout the past week, pointing to sustained institutional positioning rather than a short-lived speculative spike.

The pattern is notable because the advance has been orderly. Markets are gradually repricing the persistent divergence between U.S. and Japanese monetary policy rather than reacting to a single economic release or central-bank headline.

Why 162 Has Become an Important Level

Round numbers attract attention only when policymakers begin watching them. USD/JPY is approaching that stage. Japanese officials continue to emphasize that excessive volatility, not any specific exchange rate, would justify intervention. Even so, every move toward new multi-year highs increases pressure on authorities to demonstrate that currency stability remains a policy priority.

Whether intervention ultimately occurs is less important than the uncertainty surrounding it, which tends to increase volatility across currency markets.

The Next Story May Be in the Bond Market

Currency intervention would address the symptom, not the underlying imbalance. The more important question is whether higher Japanese yields eventually encourage domestic institutions to shift capital back home.

Japan remains one of the world's largest overseas investors, holding substantial positions in U.S. Treasuries and other foreign assets. Even a gradual repatriation of capital could reduce demand for overseas bonds, pushing yields higher and tightening global financial conditions.

The transmission mechanism is straightforward:

Higher Japanese yields → Less incentive to invest abroad → Lower demand for foreign bonds → Higher global bond yields → Higher financing costs across financial markets

This is where a foreign-exchange story begins to evolve into a broader macroeconomic one.

What Markets Will Watch Next

Attention is likely to shift toward three indicators. First, Treasury yields will determine whether the interest-rate advantage supporting the dollar remains intact. Second, investors will look for signs that the Bank of Japan is prepared to accelerate policy normalization.

Finally, markets will closely monitor official rhetoric from Tokyo for any indication that authorities are becoming increasingly uncomfortable with the pace of yen depreciation. Together, these factors will determine whether USD/JPY stabilizes below 162 or continues its march toward new cycle highs.

Artem Voloskovets

Artem Voloskovets