Marina Lubimova

Marina Lubimova

The move follows several weeks of range-bound trading and returns the market to the upper boundary that has repeatedly acted as resistance this year.

European TTF natural gas prices over the past 12 months.

The annual chart shows two distinct phases. Prices drifted lower from roughly €35/MWh last summer to around €27/MWh in December as mild weather and healthy inventories eased supply concerns. Momentum reversed early in 2026. TTF rallied toward €40/MWh in January before briefly exceeding €60/MWh in March, its highest point on the chart.

Since April, the benchmark has largely traded between €40 and €50/MWh, making today's return above €50 significant from a technical perspective. Rather than establishing a new trend, the move places prices back near the top of a four-month trading range where previous rallies have struggled to extend.

Europe's supply picture is considerably stronger than it was several years ago, but pricing remains highly responsive to future risks rather than current shortages. LNG has become the region's primary balancing source, leaving European prices increasingly linked to global cargo availability, Asian demand, shipping conditions and geopolitical uncertainty.

Seasonality also supports a more cautious market. Summer is when storage facilities are replenished for winter consumption, meaning traders often price potential supply risks well before physical balances begin to tighten. Any indication that injections could slow is reflected in forward prices almost immediately.

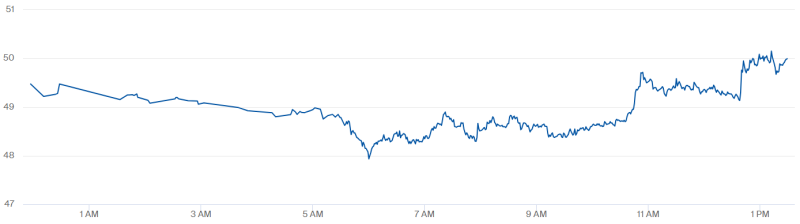

Intraday move back above €50/MWh.

The intraday chart highlights a steady shift in sentiment rather than a single spike. After opening near €49.5/MWh, prices slipped below €48/MWh during the early morning before gradually recovering. Buying accelerated around 11:00 AM, lifting TTF through €49.5/MWh, while afternoon trading pushed the contract to approximately €50.05/MWh.

The session finished close to its daily high, suggesting that buying interest strengthened into the close instead of fading after the initial breakout.

For European industry, the difference between €35 and €50/MWh is meaningful. Energy-intensive sectors including chemicals, fertilizers, metals and glass become noticeably more exposed to higher production costs as gas prices approach the upper end of this range. Utilities also face more expensive storage injections if elevated prices persist through the remainder of the summer.

The latest advance is not comparable to the extreme volatility of 2022. Instead, it reflects a market that has rebuilt its supply base while continuing to assign a premium to uncertainty. Whether prices remain above €50/MWh will largely depend on LNG arrivals, storage progress, weather patterns and geopolitical developments during the coming weeks.

Marina Lubimova

Marina Lubimova