Marina Lubimova

Marina Lubimova

The August NYMEX Natural Gas contract settled at $3.220/MMBtu, down 5.5 cents for the session. Prices opened at $3.256, climbed to an intraday high of $3.271, then reversed sharply after the release of the storage report, touching $3.195 before closing just above the $3.20 mark.

The EIA report erased early gains, sending futures back toward the day's low.

Nearly 123,000 contracts changed hands during the session, while open interest remained above 223,000 contracts, suggesting that market participation stayed elevated even as prices weakened.

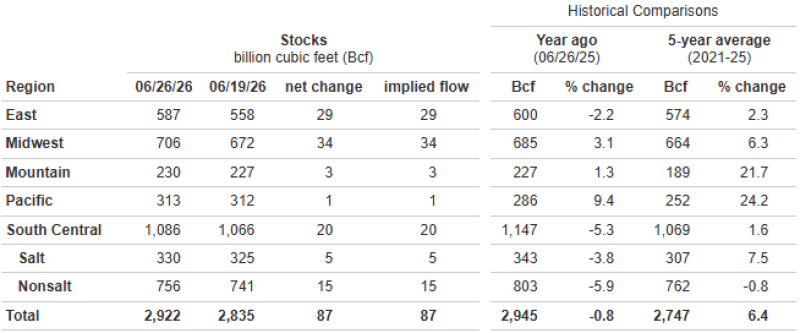

The move lower followed the Energy Information Administration's weekly storage report. Underground inventories increased by 87 Bcf, raising total working gas storage to 2,922 Bcf.

The numbers point to a market that remains comfortably supplied. Storage now stands 6.4% above the five-year average, while the deficit versus last year has narrowed to just 0.8%. Instead of tightening, inventories continue to move toward historically normal levels despite the onset of peak cooling demand.

Inventories remain slightly below last year's level but comfortably above the seasonal norm.

Regional data tells the same story. The Midwest accounted for the largest weekly build with 34 Bcf, followed by the East at 29 Bcf and the South Central region at 20 Bcf. Smaller injections across the remaining regions underline that storage growth is broad rather than concentrated in a single part of the country.

The latest report highlights the balance currently shaping the market. Electricity demand remains elevated as high temperatures increase air-conditioning use, yet production continues to replenish storage faster than consumption can reduce it. That combination limits the probability of a near-term supply squeeze and reduces the urgency for buyers to chase prices higher.

Price action reflects that balance. The market continues to find buyers near $3.20/MMBtu, but attempts to extend the rally above $3.30 have repeatedly stalled. Without a material change in weather forecasts, LNG exports, or domestic production, futures are likely to remain driven by weekly storage data rather than by expectations of tightening fundamentals.

Attention now shifts to next week's EIA report and updated temperature forecasts. Another above-average storage build would reinforce the view that inventories are rebuilding comfortably ahead of winter, while a meaningful slowdown in injections could quickly shift sentiment back in favor of higher prices.

Marina Lubimova

Marina Lubimova