Marina Lubimova

Marina Lubimova

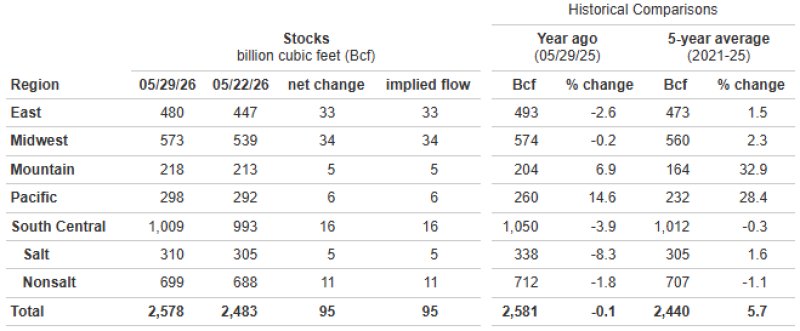

U.S. natural gas futures jumped 4.1% after the latest EIA storage report, despite inventories rising by 95 Bcf during the week ending May 29.

At first glance, the move looks contradictory. More gas in storage usually means weaker prices. But the market wasn't focused on the inventory increase itself—it was focused on the fact that traders expected an even larger build.

The latest report lifted total U.S. gas inventories to 2,578 Bcf, almost identical to last year's level and 5.7% above the five-year average. That hardly looks like a supply shortage.

| Metric | Value |

| Weekly Injection | +95 Bcf |

| Total Storage | 2,578 Bcf |

| vs. Last Year | -0.1% |

| vs. 5-Year Average | +5.7% |

The largest injections came from the Midwest (+34 Bcf) and East (+33 Bcf), which together accounted for more than two-thirds of the weekly increase. Still, the market rallied.

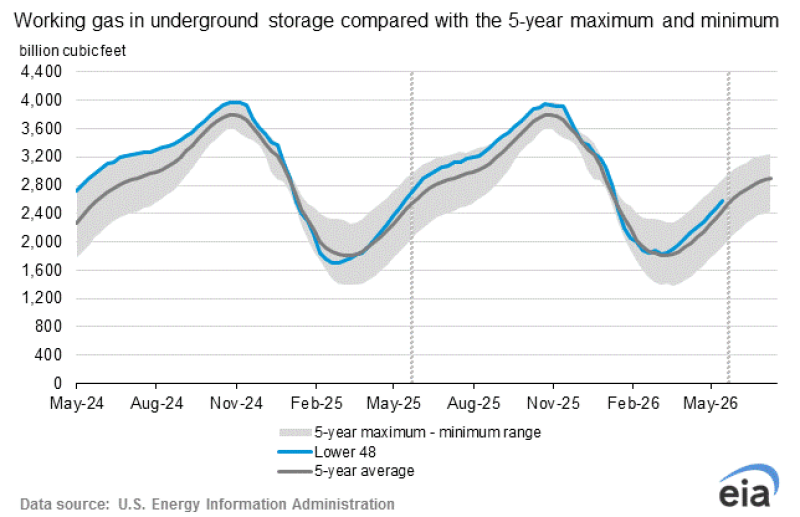

The storage chart also shows that inventories remain comfortably within historical norms. Stocks are above the five-year average but nowhere near record highs. In other words, the market is well supplied, but not oversupplied.

That shifts attention away from current inventories and toward what happens next. With summer approaching, traders are increasingly focused on cooling demand, LNG exports, and production growth. If hot weather boosts electricity consumption or exports remain strong, weekly injections may begin to shrink further.

The latest EIA report does not signal a shortage. What it signals is that the supply cushion may not be growing as quickly as some participants expected. That's enough to trigger a sharp move in a market where sentiment had become heavily skewed toward abundant supply.

Marina Lubimova

Marina Lubimova