Marina Lubimova

Marina Lubimova

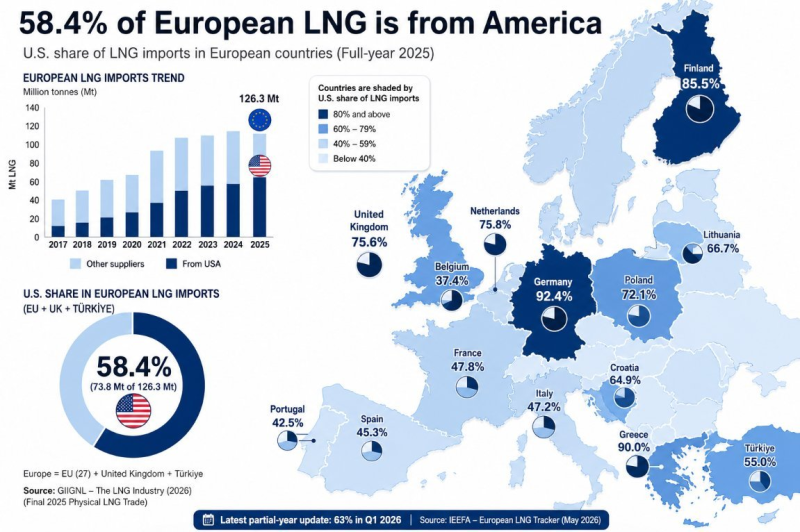

In 2025, Europe imported 126.3 million tonnes of LNG. The United States supplied 73.8 million tonnes, or 58.4% of the total.

Germany sourced 92.4% of its LNG imports from the U.S. Greece reached 90%, Finland 85.5%, while the Netherlands, Poland and the United Kingdom all remained above 70%.

Before 2022, LNG supplemented pipeline imports. Today it performs the opposite role. LNG has become the primary mechanism through which Europe balances its gas market.

The change reduced dependence on Russian pipeline infrastructure, but it also tied European energy security more closely to global LNG supply chains.

Gas is becoming a global commodity

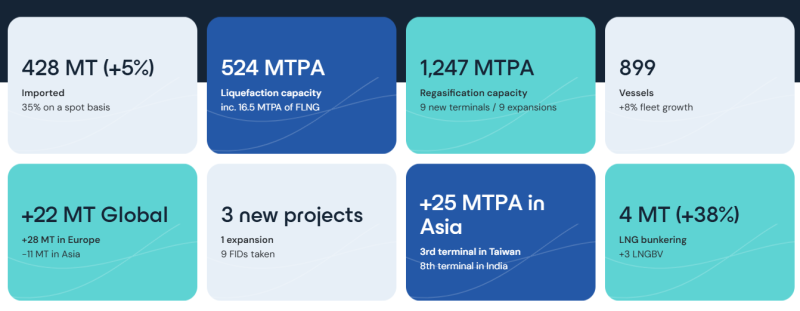

The LNG market continued expanding in 2025.

- Global LNG imports reached 428 million tonnes.

- Liquefaction capacity rose to 524 MTPA.

- Regasification capacity reached 1,247 MTPA.

- The LNG carrier fleet expanded to 899 vessels.

- Global LNG supply increased by 22 million tonnes.

Europe absorbed most of the additional supply, increasing imports by roughly 28 million tonnes, while Asian demand declined by around 11 million tonnes.

The result is a gas market that increasingly resembles the oil market. Supply, demand and pricing are becoming global rather than regional. A disruption in one part of the system can now affect buyers thousands of miles away.

Europe's exposure has shifted

Russian gas created a concentration risk. LNG creates market risk. Europe now depends on a broader network of suppliers and transport routes, but that network introduces new variables:

- U.S. export capacity

- LNG vessel availability

- Shipping lanes

- Weather-related disruptions

- Competition from Asia

The supply base is more diversified than it was before 2022. The pricing mechanism is less predictable.

Asia is the swing factor

Europe's ability to attract LNG cargoes in 2025 was helped by weaker Asian demand. Asian LNG imports fell by roughly 11 million tonnes during the year, freeing cargoes for Europe.

That backdrop may not persist. India continues expanding LNG infrastructure. Additional regasification capacity entered service in 2025, while China's gas consumption remains one of the largest sources of future demand growth.

If Asian LNG demand returns to pre-slowdown growth rates, Europe will face stronger competition for available cargoes. The balance of the LNG market would tighten quickly.

Hormuz matters more than ever

Pipeline gas linked Europe to Eastern European transit routes. LNG links Europe to maritime chokepoints. According to ACER, a full-year closure of the Strait of Hormuz could remove approximately 27 bcm of LNG supply from global markets.

The direct impact would extend far beyond the Gulf region. Lower LNG availability would increase competition for cargoes, tighten supply conditions and place upward pressure on European gas prices.

Europe reduced one geopolitical exposure while increasing another.

Supply stabilized faster than prices

The LNG buildout helped prevent physical shortages. Price volatility remains.

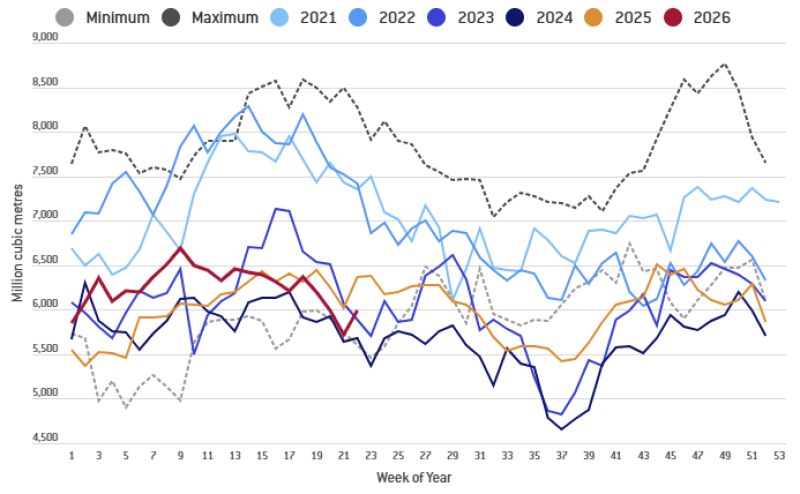

TTF prices remain well below the extremes reached during the energy crisis, but market sensitivity has not disappeared.

Geopolitical events, LNG outages, shipping disruptions and weather patterns continue to influence pricing. The market no longer fears running out of gas. It still reacts sharply to changes in expected supply.

The next constraint is affordability

Global LNG production increased by 36 bcm in 2025, the strongest annual increase since 2022. Developers approved roughly 90 bcm of additional export capacity, signaling expectations of sustained demand growth. Those investments improve supply availability. They do not guarantee lower prices. As LNG becomes the dominant source of marginal gas supply, Europe's main challenge shifts from access to affordability.

Conclusion

Europe's gas market is no longer organized around Russian pipelines. It is organized around LNG.

That shift improved supply security and reduced concentration risk. It also connected Europe more closely to global energy trade, shipping routes and international competition for cargoes.

The continent is less vulnerable to a single supplier than it was three years ago. It is more exposed to the dynamics of the global LNG market.

Marina Lubimova

Marina Lubimova