Artem Voloskovets

Artem Voloskovets

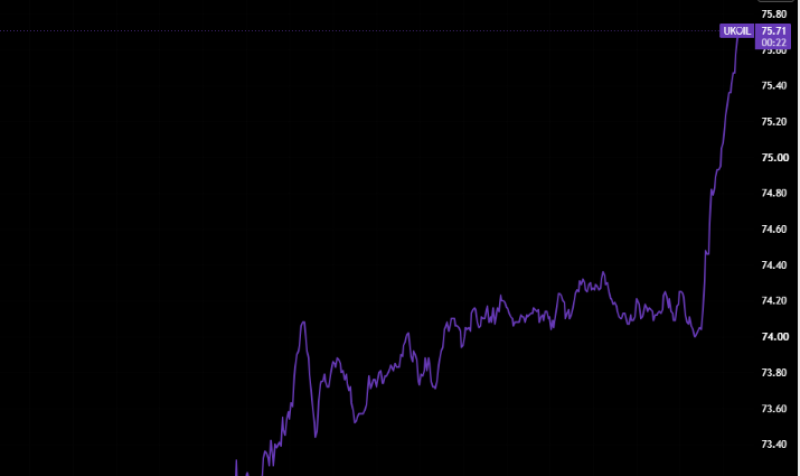

Brent traded close to $74 per barrel for most of the session before buyers stepped in aggressively after the announcement. Prices accelerated to $75.71, producing one of the sharpest intraday moves in recent weeks. The speed of the rally suggests traders were repositioning for higher geopolitical risk rather than responding to an immediate change in global supply.

Brent crude rallied from roughly $74 to $75.71 after the U.S. tightened restrictions on Iranian oil sales.

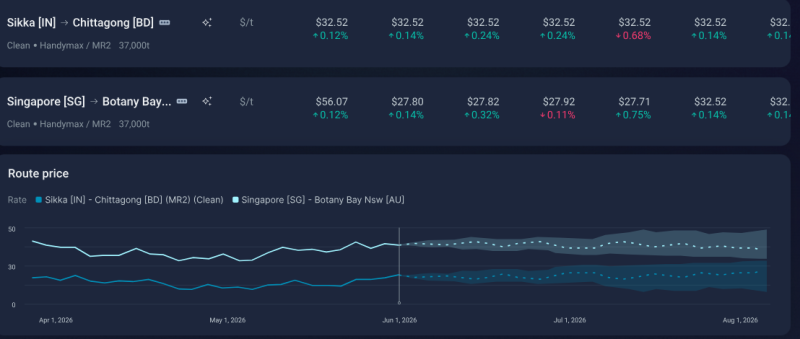

The contrast with shipping markets is striking. Clean tanker freight remains remarkably steady across key Asian routes. Freight from Sikka (India) to Chittagong (Bangladesh) continues to trade near $32.52 per tonne, while the Singapore–Botany Bay route is holding around $32–33 per tonne despite several months of elevated geopolitical tension.

Historical freight data tells the same story. Since April, the Singapore–Australia route has mostly fluctuated between the mid-$30s and low-$40s per tonne, while the India–Bangladesh corridor has remained largely within the $20–27 per tonne range. Even forward projections into August point to gradual movement rather than the surge normally associated with an imminent supply shock.

Tanker freight rates remain stable, indicating that physical oil flows have yet to reflect the jump seen in futures prices.

The disconnect reflects how different parts of the oil market respond to risk. Futures react within seconds because they price expectations. Shipping markets respond only when cargoes change direction, insurance costs rise, or charter demand increases. None of those signals are visible yet.

That makes the latest rally primarily a reassessment of future risk rather than confirmation that Iranian exports are already falling. The next phase depends on enforcement rather than the announcement itself.

Should Washington tighten sanctions aggressively, transporting and financing Iranian crude will become more difficult, increasing costs across the supply chain. Freight rates, insurance premiums and regional crude differentials would likely begin moving higher alongside benchmark prices.

If exports continue through existing trading networks, however, physical flows may remain largely unchanged even as financial markets continue to trade geopolitical headlines.

Crude prices are anticipating tighter supply, while shipping data still points to a market operating under normal conditions. The gap between those two markets will determine whether Brent's rally becomes the start of a sustained uptrend or simply another short-lived geopolitical spike.

Artem Voloskovets

Artem Voloskovets