Marina Lubimova

Marina Lubimova

The latest U.S. Energy Information Administration (EIA) report delivered a set of figures that would typically support higher oil prices.

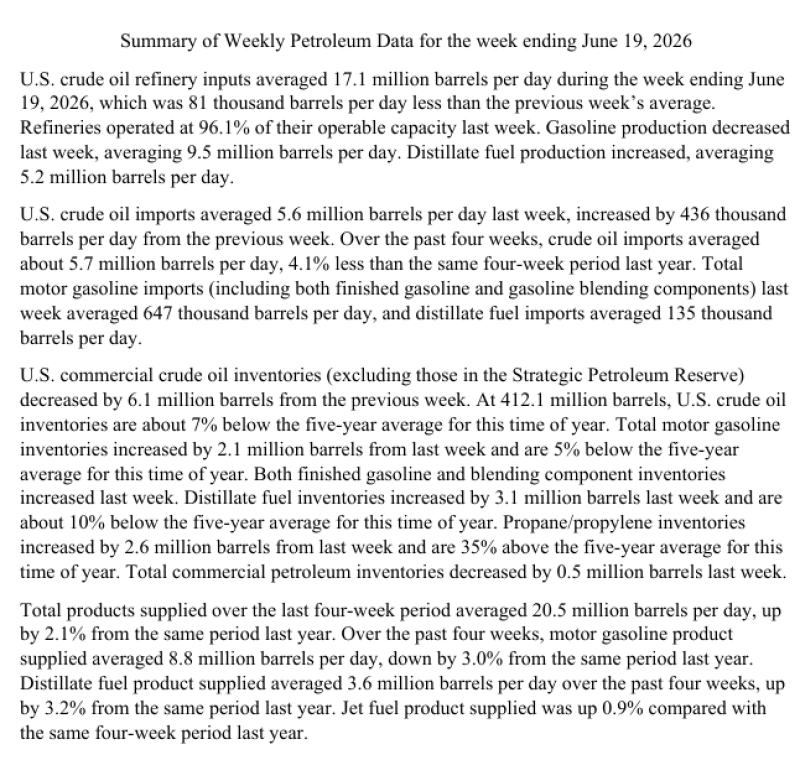

Commercial crude inventories fell by 6.1 million barrels, leaving stockpiles at 412.1 million barrels, around 7% below the five-year seasonal average. U.S. refiners processed 17.1 million barrels per day, operating at 96.1% of available capacity, one of the strongest utilization rates of the year.

These numbers point to a physical market that remains tight. Refiners are consuming crude aggressively, and inventories continue to trend below historical norms.

Show current inventories (412.1M barrels), previous week, five-year average, and highlight the weekly draw of 6.1M barrels.

The Market Focused on Refined Products Instead

The bullish signal from crude inventories was offset by developments further down the supply chain. Gasoline inventories increased by 2.1 million barrels, while distillate stocks—including diesel and heating oil rose by 3.1 million barrels. At the same time, gasoline production eased to 9.5 million barrels per day, even as refinery utilization remained exceptionally high.

The combination suggests that refiners are producing enough fuel to replenish inventories faster than demand is absorbing it. As a result, the crude shortage reflected in storage tanks has not translated into the same degree of tightness for finished products.

| Product | Weekly Change |

| Crude Oil | −6.1M |

| Gasoline | +2.1M |

| Distillates | +3.1M |

Demand Remains Firm, but Expectations Have Changed

The broader consumption picture remains constructive. Over the past four weeks, total petroleum products supplied averaged 20.5 million barrels per day, up 2.1% from a year earlier. Distillate demand increased 3.2%, while jet fuel demand rose 0.9%, indicating continued strength in freight activity and air travel.

Crude imports also climbed by 436,000 barrels per day to 5.6 million barrels per day, providing additional supply without preventing the large inventory draw. None of these figures point to a weakening physical market. Instead, they show a market that remains balanced but is no longer reacting to inventory data in isolation.

Include:

- Total products supplied: 20.5M bpd (+2.1% YoY)

- Distillate demand: +3.2% YoY

- Jet fuel demand: +0.9% YoY

Why the Reaction Was Muted

The price action suggests that the market has become more selective about what qualifies as bullish.

A few months ago, a 6.1 million barrel inventory draw would likely have triggered a stronger rally. Today, traders appear more concerned with whether global fuel consumption can keep pace with rising refinery output.

Upcoming inflation data, central bank policy, manufacturing activity and broader economic indicators are likely to have a greater influence on oil prices than a single weekly inventory report. Supply remains supportive, but expectations for demand have become the dominant variable.

The Bigger Signal

Brent's decline was small, but its significance lies in the market's response rather than the price change itself.

The latest EIA report confirmed that crude supplies remain tight and refinery activity is robust. Yet investors chose to look beyond those fundamentals, focusing instead on whether demand will remain strong enough to justify higher prices later this year.

That shift matters. It suggests the oil market is moving away from trading individual supply headlines and toward pricing a broader macroeconomic outlook—one where the direction of demand may carry more weight than the size of the next inventory draw.

Marina Lubimova

Marina Lubimova