Artem Voloskovets

Artem Voloskovets

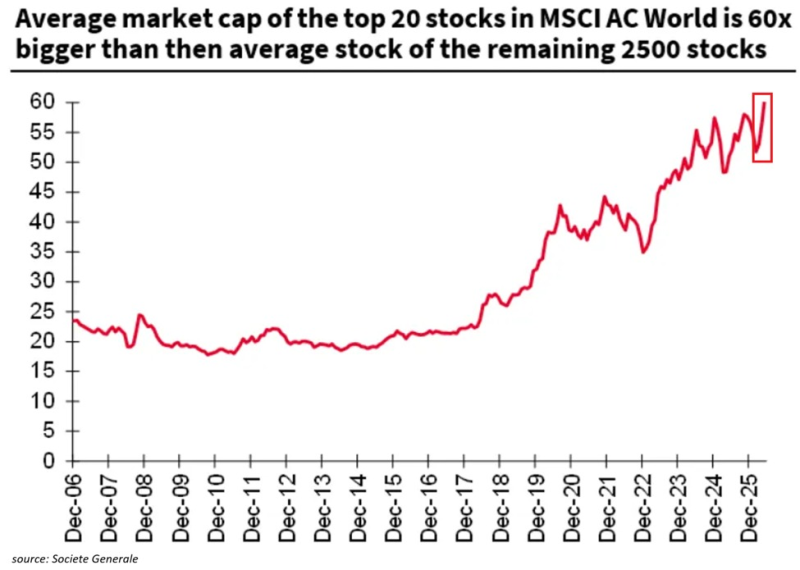

The gap between the world's largest companies and everyone else has widened dramatically.

According to Société Générale, the average member of the 20 largest companies in the MSCI All Country World Index is now roughly 60 times larger than the average company among the remaining 2,500 constituents. For most of the period between 2006 and 2017, that figure fluctuated around 20 times.

The chart is often interpreted as evidence of stock-market concentration. It is also evidence of something broader: the economic advantages of scale have become stronger than at any point in recent decades.

Global Reach Without Geographic Limits

The largest businesses no longer expand country by country. Software, cloud infrastructure, digital advertising, e-commerce networks and AI services can be deployed across dozens of markets simultaneously. Once a platform reaches sufficient scale, every additional user becomes cheaper to serve than the previous one.

That creates a powerful asymmetry. A successful company can grow globally without increasing costs at the same pace. The result is visible in market capitalizations, but the underlying force is operational rather than financial.

Where Influence Is Concentrated

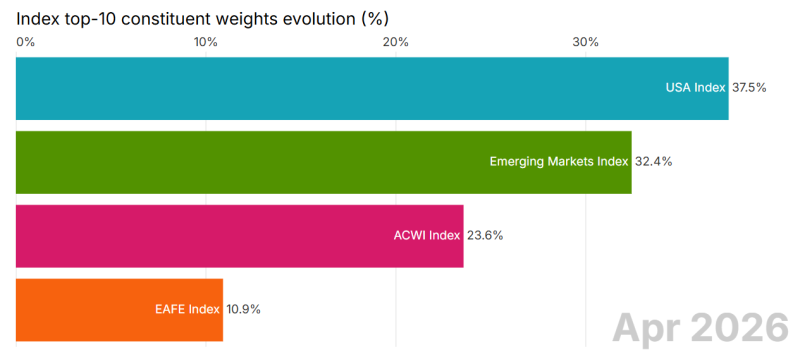

Concentration appears across most major equity benchmarks.

The ten largest companies account for 37.5% of the USA Index, 32.4% of the Emerging Markets Index and 23.6% of the MSCI ACWI Index. Only the EAFE Index remains relatively dispersed, with the top ten representing 10.9% of the benchmark.

The numbers suggest that economic influence is accumulating faster than the number of companies capable of competing at a global level.

Many industries still contain thousands of participants. Far fewer control the infrastructure, data, distribution channels and technological ecosystems on which those industries increasingly depend.

Scale Alone Is Not Enough

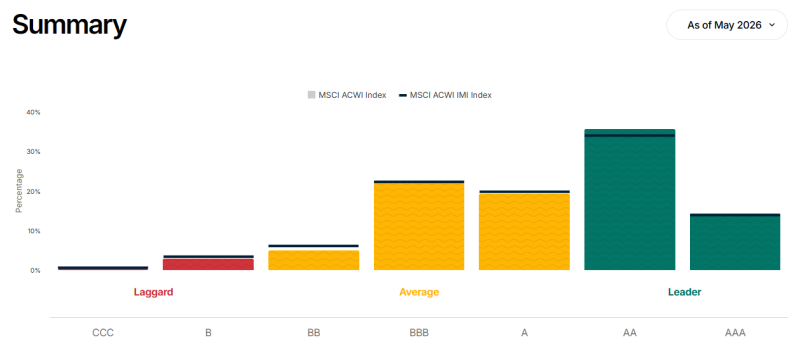

The concentration trend is often described as a race toward the largest companies. The credit-quality data points to a more specific pattern.

The highest weights in MSCI ACWI are concentrated among AA-, A- and AAA-rated businesses. Lower-rated issuers occupy only a small portion of the index.

Size matters, but financial resilience matters just as much. Companies with stronger balance sheets can invest through economic slowdowns, fund large-scale research programs and absorb technological shifts that smaller competitors struggle to finance.

That advantage compounds over time.

Thousands of Companies, One Direction

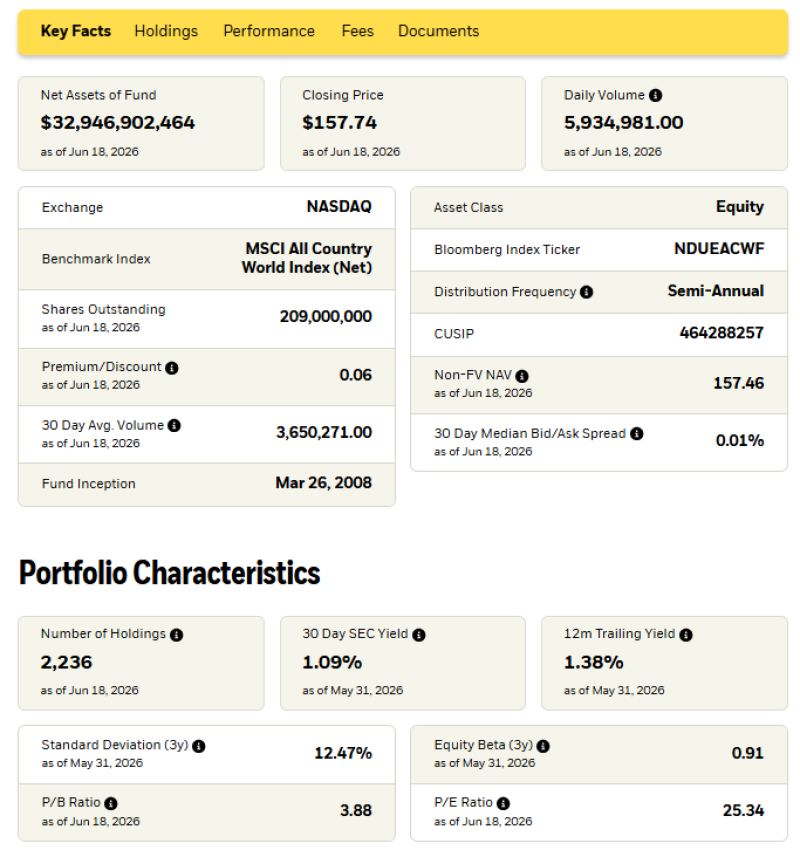

The MSCI ACWI ETF owns 2,236 companies and provides exposure to virtually every major region of the world. Yet the portfolio's overall behavior is increasingly shaped by a narrow group of dominant firms.

This pattern extends beyond financial markets. Consumers encounter thousands of products, applications and services, but many are built on the same cloud infrastructure, distributed through the same digital platforms and monetized through the same advertising networks.

Competition remains widespread. Control over critical systems is not.

An Economy Built Around Platforms

For much of the twentieth century, size was constrained by geography, manufacturing capacity and distribution networks. Digital businesses operate under different rules. Data, software and artificial intelligence scale across borders with minimal friction, allowing a handful of companies to serve markets that once required thousands of local competitors.

The widening gap between the largest firms and the rest of the market reflects that shift. The story behind the chart is not simply that large companies are becoming larger.

It is that modern economic activity increasingly flows through a small number of platforms that connect businesses, consumers and information on a global scale.

Artem Voloskovets

Artem Voloskovets