Artem Voloskovets

Artem Voloskovets

Capital wasn't flowing into the largest AI winners. It was spreading across the broader semiconductor and infrastructure ecosystem.

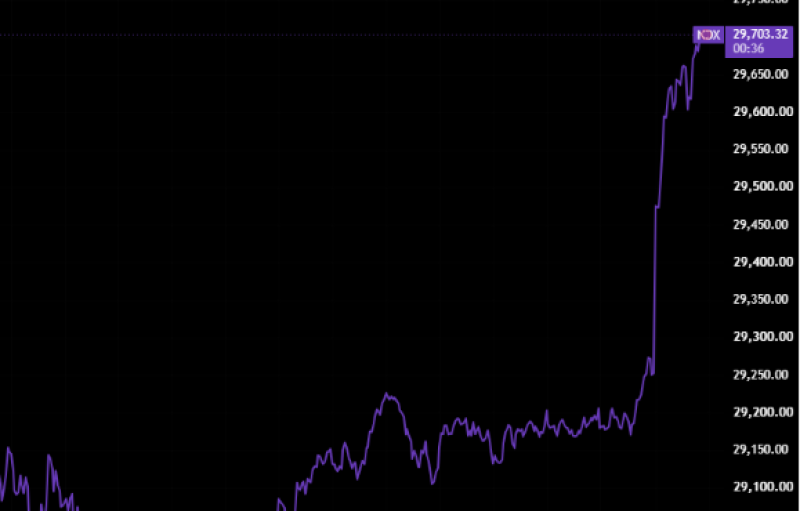

For most of the day, the Nasdaq-100 traded quietly between roughly 29,150 and 29,220, showing little directional conviction. That changed within a short period as buyers pushed the index almost 500 points higher to approximately 29,703, setting a new intraday high.

The timing of the breakout is significant. Instead of fading after an early rally, buying pressure intensified late in the session. Such price action typically reflects large institutional orders entering the market after hours of consolidation rather than short-term speculative momentum.

The rally unfolded despite weakness among the market's largest technology companies.

Nvidia fell 1.26%, Microsoft lost 1.16%, Apple declined 0.81%, Alphabet dropped 1.40%, while Meta slid 2.06%. Under normal conditions, simultaneous declines in companies with such heavy index weightings would make it difficult for the Nasdaq-100 to reach a new session high.

Instead, leadership shifted deeper into the AI supply chain.

Micron surged 8.85%, AMD jumped 7.76%, Oracle gained 6.49%, Intel added 4.90%, Applied Materials rose 4.63%, while Lam Research, KLA, and Teradyne advanced 9.09%, 10.83%, and 8.04%, respectively. Western Digital climbed 6.82%, and Synopsys added 6.67%.

The distribution of gains suggests investors are widening exposure rather than increasing concentration. Earlier stages of the AI rally were driven largely by a handful of mega-cap companies. This session looked different. Money flowed into memory manufacturers, chip-equipment suppliers, design software developers and enterprise infrastructure providers—the companies positioned to benefit as AI investment expands beyond GPU deployment.

Oracle's strong advance, combined with sharp gains across semiconductor equipment manufacturers, points to renewed confidence in infrastructure spending. The moves in Micron and AMD indicate growing expectations for the next phase of AI demand, where memory, networking, storage, and manufacturing capacity become increasingly important.

Perhaps the most notable feature of the session is that the Nasdaq-100 reached a fresh high without support from its largest constituents. Breadth improved enough for gains across second-tier technology names to offset declines in several companies that typically dominate index performance.

That shift changes the market narrative. Investors are no longer allocating capital solely to the companies that built the first phase of the AI trade. They are increasingly targeting businesses expected to supply the hardware, manufacturing tools, and enterprise platforms required for the next stage of industry expansion.

If this rotation continues, market leadership could become significantly broader than it has been over the past year. Historically, rallies supported by wider participation tend to prove more durable than advances dependent on only a few mega-cap stocks.

The latest session suggests that technology leadership is expanding rather than weakening. The AI investment cycle is no longer defined by a small group of dominant companies; it is beginning to encompass the broader ecosystem that enables them.

Artem Voloskovets

Artem Voloskovets