Artem Voloskovets

Artem Voloskovets

The figure is large, but the number itself is not the most interesting part of the story. Defaults accumulated during years in which payment requirements, reporting rules, and collection practices changed repeatedly. What matters now is that the repayment system is becoming active again.

Millions of borrowers who spent several years outside the collection process are being pushed back into it at a time when housing costs, insurance costs, and consumer debt burdens are substantially higher than they were before the pandemic.

The result is likely to be felt not only in student lending data but across household finances more broadly.

Delinquencies Are Rising Faster Than in Other Consumer Credit Categories

The sharpest deterioration in consumer credit is currently occurring in student loans.

According to New York Fed data, the share of student loan balances moving into serious delinquency rose from 8.04% in the first quarter of 2025 to 10.86% in the first quarter of 2026.

By comparison, credit card delinquencies increased only marginally, while auto loans and mortgages showed relatively small changes.

| Category | Q1 2025 | Q1 2026 |

| Student Loans | 8.04% | 10.86% |

| Credit Cards | 7.04% | 7.10% |

| Auto Loans | 2.94% | 2.97% |

| Mortgages | 1.22% | 1.48% |

The gap is notable because student debt represents only one component of household borrowing, yet it accounts for the largest increase in payment distress.

The issue is not the size of outstanding balances. Student debt totals approximately $1.66 trillion, a figure that has actually declined modestly over the past year. The issue is repayment performance.

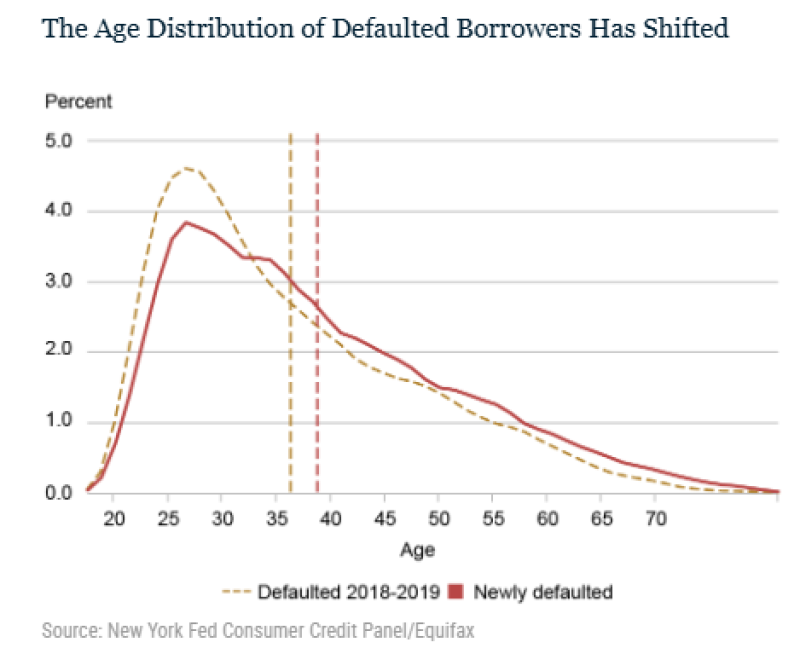

Defaults Are Moving Up the Age Curve

The profile of borrowers entering default is changing. Before the pandemic, defaults were concentrated more heavily among borrowers in their twenties and early thirties. Recent data show a noticeable shift toward older age groups.

The average age of newly defaulted borrowers has increased from roughly 36 to 39 years old, while the distribution extends further into the 40–60 age range than it did in 2018–2019.

This matters because financial behavior changes with age. A borrower in their late twenties is often deciding whether to rent an apartment, purchase a vehicle, or relocate for work. A borrower in their forties or fifties is more likely to be managing a mortgage, supporting children, building retirement savings, or caring for aging parents.

The same monthly payment carries different economic consequences.

Disposable Income Is Being Reallocated

Student loan collections do not create a new liability. The debt already exists. What changes is the destination of household cash flow. Money that might otherwise be directed toward consumption, savings, home improvements, travel, or debt reduction elsewhere is redirected toward repayment.

For an individual borrower, the adjustment may appear manageable. Across millions of households, however, the effect becomes large enough to influence aggregate spending patterns.

The impact is unlikely to appear in a single economic release. It is more likely to emerge gradually through slower discretionary spending growth and weaker household balance-sheet improvement.

Housing Sits in the Middle of the Adjustment

The age distribution data point toward housing as one of the areas most exposed to renewed repayment obligations.

The borrowers increasingly represented among new defaults are in the same demographic groups that typically drive first-home purchases, move-up purchases, and mortgage refinancing activity.

Higher monthly debt obligations can affect mortgage qualification, down-payment accumulation, and housing affordability calculations.

None of these effects need to be dramatic to matter. Housing activity is often driven by marginal affordability decisions, particularly when mortgage rates remain elevated.

A Different Form of Financial Tightening

Financial conditions are usually discussed through the lens of Federal Reserve policy. Interest rates, credit spreads, and lending standards receive most of the attention because they directly affect borrowing costs.

The resumption of student loan collections works through a different channel. Rather than increasing the cost of new borrowing, it increases the share of existing income devoted to debt service.

For affected households, the outcome is similar: less financial flexibility and less discretionary cash flow. The mechanism is different, but the economic effect moves in the same direction.

Artem Voloskovets

Artem Voloskovets