Artem Voloskovets

Artem Voloskovets

The size of the cut naturally attracts attention, but the more important signal lies elsewhere. Saudi Arabia is responding to a market that no longer justifies the geopolitical premium embedded in Middle Eastern crude only weeks ago. At the same time, slowing demand growth and expanding supply have shifted competition back toward pricing rather than availability.

The decision says less about where oil prices are today than about how producers expect the market to behave over the coming months.

A Pricing Tool, Not a Price Forecast

Official Selling Prices are frequently confused with benchmark oil prices. Brent and WTI reflect financial markets, while OSPs determine the price refiners pay for physical cargoes delivered under long-term contracts. Because Saudi Arabia remains the largest crude supplier to Asia, changes in its OSP often influence pricing decisions across the Gulf.

An $11 reduction is therefore a commercial decision rather than a directional forecast for crude futures. Instead, it reflects a simple reality: buyers currently have more negotiating power than they did earlier this year.

The Risk Premium Has Already Been Repriced

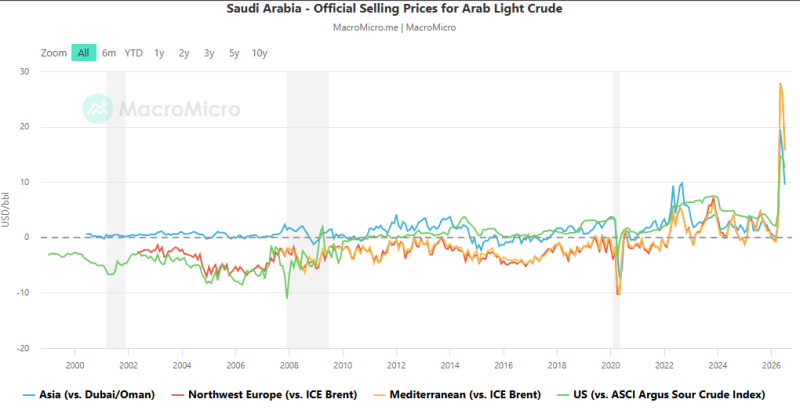

The historical pricing data illustrates how unusual recent market conditions have been. For most of the past two decades, the premium of Arab Light over the Dubai/Oman benchmark fluctuated close to neutral, typically ranging between 0 and 5 dollars per barrel.

That relationship broke down during the recent Middle East tensions. Saudi export premiums briefly surged to almost $28 per barrel, reflecting fears that shipping through the Strait of Hormuz could be disrupted for an extended period.

Those concerns have faded quickly. The latest reduction effectively removes a significant portion of that emergency premium and brings pricing closer to historical norms. Physical crude markets have been moving in the same direction for several weeks. Cash premiums for Dubai crude have fallen sharply while additional Gulf cargoes returned to the market as shipping risks eased. Saudi Arabia's decision follows that trend rather than initiating it.

Demand Is No Longer Absorbing Additional Supply

Supply is only one side of the equation. The demand picture has become less supportive, particularly in Asia. The latest trade figures show Saudi crude exports declining by 1 million barrels per day, while China's crude imports fell by approximately 2.4 million barrels per day. Italy, by comparison, increased imports by only 451,000 barrels per day, insufficient to offset weaker Asian demand.

China remains the world's largest crude importer and the primary destination for incremental Middle Eastern exports. When Chinese refiners reduce purchases, producers compete more aggressively for the remaining demand. That competitive pressure is now becoming visible in official pricing.

Supply Has Become Easier to Replace

The oil market has also become materially better supplied. OPEC+ continues restoring production, exports through the Strait of Hormuz have normalized, and additional barrels from the United States, Brazil, Guyana, and other producers continue entering international markets. This combination reduces the pricing power of any single exporter. Rather than relying on tight supply to support premiums, producers increasingly compete by improving commercial terms for refiners. Saudi Arabia's latest pricing decision fits that environment.

Futures Are Consistent With Physical Markets

The futures market reflects the same message. Brent continues trading around $72 per barrel, while WTI remains near $68 despite weeks of geopolitical uncertainty. If traders expected a prolonged disruption to Middle Eastern exports, benchmark prices would likely be substantially higher. Instead, futures indicate that additional production and recovering export flows are expected to offset remaining geopolitical risks. Saudi Arabia's OSP adjustment therefore aligns with broader market expectations rather than challenging them.

Periods of tight supply allow exporters to defend higher premiums. Periods of abundant supply reward competitive pricing. Current market conditions increasingly resemble the second environment. Russian crude remains available at discounted prices, the UAE and Iraq continue expanding exports, and Atlantic Basin producers are competing for Asian refinery demand. Against that backdrop, protecting customer relationships becomes as important as maximizing the price received for each barrel.

What This Move Actually Signals

The significance of Saudi Arabia's decision extends beyond a single monthly pricing adjustment. It indicates that the market is placing less weight on geopolitical disruption and more weight on underlying fundamentals: expanding supply, softer import demand, and intensifying competition among exporters. Rather than marking the beginning of a new price cycle, the August OSP adjustment acknowledges a shift that has already been developing across physical crude markets.

Artem Voloskovets

Artem Voloskovets