Marina Lubimova

Marina Lubimova

According to Reuters, more than half of the capital has already been pledged by companies from the United States, Gulf countries, Asia, South America and Africa. No government money would be involved.

The figure itself is what makes the proposal remarkable. For a country that has spent decades largely cut off from global capital markets, $300 billion is not simply another investment package. It is an amount that exceeds many years of foreign investment combined.

Four Decades of Missing Capital

Iran possesses some of the world's largest hydrocarbon reserves and a population of more than 92 million people, yet international investment has remained limited for most of the last forty years.

The country's isolation from Western financial systems and repeated rounds of sanctions prevented it from attracting capital on a scale seen in other major emerging markets.

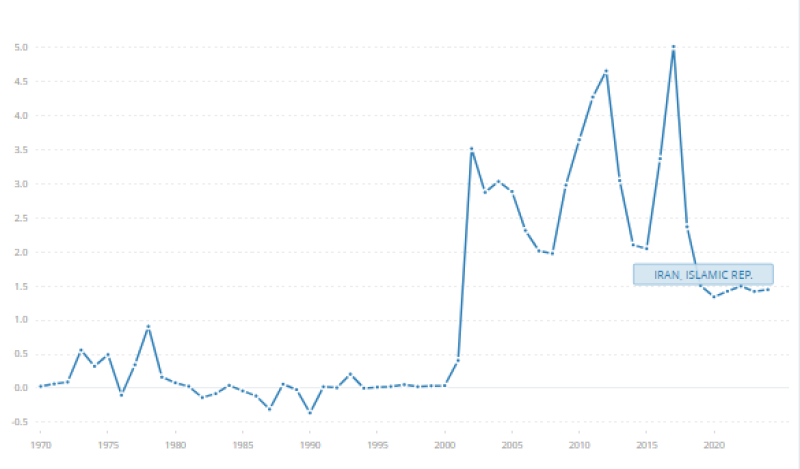

Foreign Direct Investment in Iran, 1970–2024 The historical FDI data tells the story clearly. For most of the period after the 1979 revolution, foreign investment remained negligible. Even during stronger years, annual inflows generally fluctuated between $2 billion and $5 billion.

The largest peaks on record barely approached the $5 billion mark. Against that backdrop, a proposed $300 billion fund is not a marginal increase. It represents a completely different order of magnitude.

Why Investors Are Looking at Iran

The attraction is not difficult to understand. Iran holds the world's second-largest proven natural gas reserves and the fourth-largest proven oil reserves. It also has a large domestic market, an established industrial base and sectors that have received relatively little international investment over the past several decades.

The opportunity lies less in discovering new assets than in gaining access to assets that have long been unavailable. Energy infrastructure, petrochemicals, logistics, mining and transportation are among the sectors expected to attract the strongest interest if restrictions are eased.

A Fund Without a Deal Is Just a Proposal

The headline figure may be large, but the project remains theoretical. The current document is a 60-day memorandum rather than a final agreement. During that period, negotiators are expected to work on separate tracks covering nuclear issues, sanctions and regional security.

Reuters reports that the investment vehicle will not be established until a final agreement is signed. Questions regarding governance, administration and project allocation have yet to be resolved. In other words, the market is currently pricing a possibility rather than a completed transaction.

Separate Tracks, Different Timelines

The investment fund is not tied directly to negotiations over frozen Iranian assets or sanctions relief. Those discussions are proceeding in parallel, according to people familiar with the talks.

That distinction matters because private investors can express interest today while still waiting for legal and regulatory barriers to be removed before committing capital. Even if political negotiations progress smoothly, actual deployment of funds could take years.

The Scale Gap

The most striking aspect of the proposal is not the number itself but its relationship to Iran's investment history. The chart highlights the gap between historical reality and the proposed framework. Iran's annual foreign investment inflows have generally remained below $5 billion. The proposed fund is approximately sixty times larger than the strongest annual inflows recorded in recent decades.

Very few countries move from attracting a few billion dollars per year to having access to hundreds of billions in committed capital. That is why the proposal has drawn attention far beyond diplomatic circles.

Marina Lubimova

Marina Lubimova