Marina Lubimova

Marina Lubimova

Neither is happening. Jet fuel prices have been falling, OPEC+ retains substantial unused production capacity, and European officials continue to describe the market as adequately supplied. The contradiction is only apparent. Inventory and supply are not the same thing.

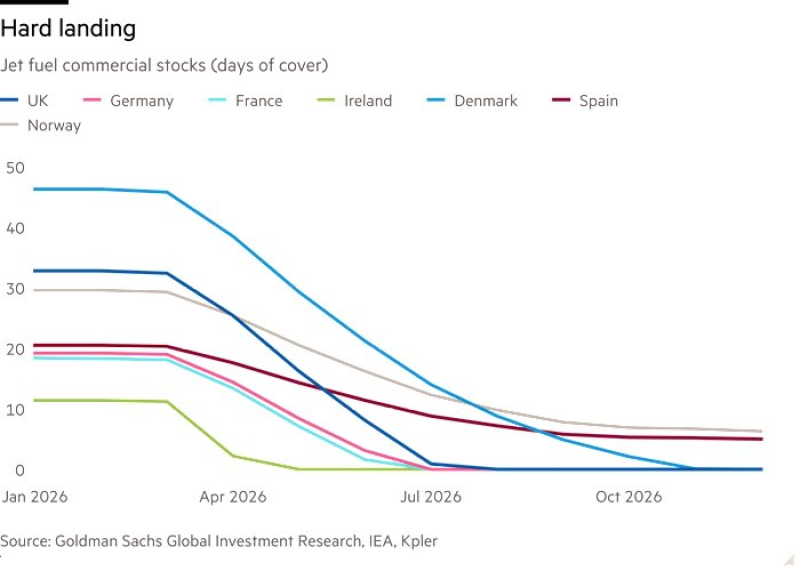

Inventories Are Disappearing

Commercial stock cover is falling across nearly every major European aviation market.

Denmark starts the year with roughly 46 days of cover and ends close to zero. The UK falls from approximately 33 days to almost nothing by mid-year. Germany and France lose most of their inventory protection before the summer travel season reaches its peak. Ireland's decline is even steeper.

By late 2026, several markets shown in the data operate with little meaningful inventory buffer.

The chart looks alarming because inventories traditionally serve as the market's first line of defence against disruption.

Prices Tell A Different Story

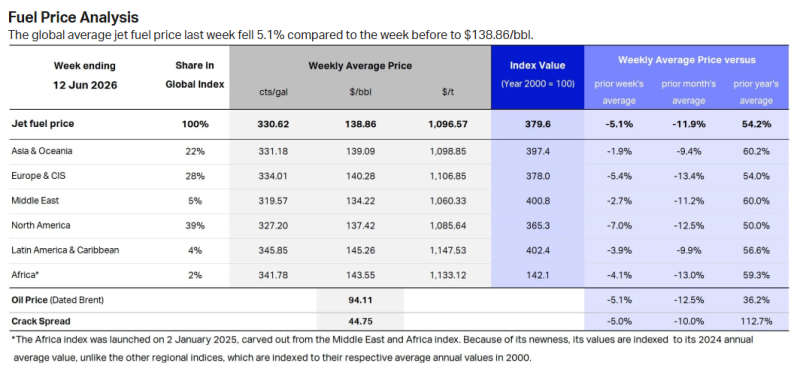

Fuel markets are behaving far more calmly than inventory data would suggest. The global average jet fuel price fell 5.1% in the latest reporting week to $138.86 per barrel. European prices declined 5.4%, while Brent crude traded near $94 per barrel.

Month-over-month declines are even larger, with jet fuel prices down almost 12%. Markets preparing for a physical shortage rarely respond by lowering prices. Current pricing implies that traders remain confident about supply availability despite the drawdown in inventories.

Supply Is Not The Constraint

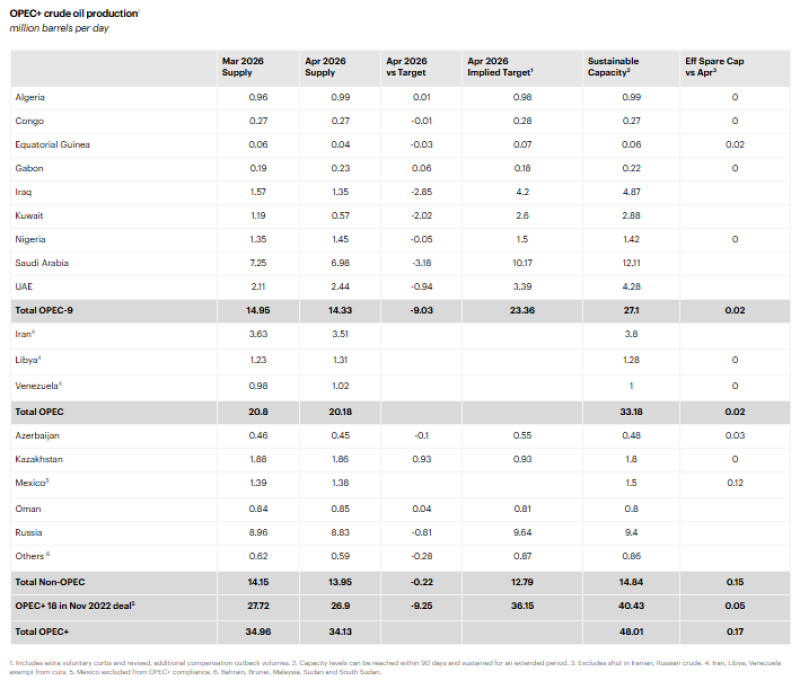

OPEC+ production data helps explain why. The group produced roughly 34.1 million barrels per day in April while maintaining sustainable capacity near 48 million barrels per day.

Saudi Arabia, the UAE, Kuwait and Iraq all remain well below estimated production capability. Collectively, OPEC+ still controls almost 14 million barrels per day of spare capacity.

The market is not confronting a lack of crude supply. Oil remains available. Capacity remains available. The pressure is appearing elsewhere.

A Supply Chain Problem, Not A Resource Problem

European officials are focusing on logistics rather than production.

The latest Oil Coordination Group meeting concluded that there are currently no fuel shortages within the European Union. At the same time, participants identified jet fuel as the segment most exposed to potential disruption if tensions affecting Middle Eastern trade routes persist.

Attention is increasingly centred on transport corridors, refinery output, import flows and storage availability.

As inventories decline, the system becomes more dependent on those channels operating without interruption.

What Low Inventories Change

Inventory is often treated as a simple stock number. In practice, it represents time.

- Time to absorb a refinery outage.

- Time to reroute cargoes.

- Time to replace delayed imports.

- Time to respond when conditions change unexpectedly.

That flexibility becomes harder to find as stock cover approaches minimum levels.

The past two years demonstrate how quickly aviation fuel markets can tighten. Prices moved above $200 per barrel during periods of stress before gradually returning toward current levels.

The difference today is that inventory protection appears significantly thinner. Future disruptions do not need to be larger than previous ones to generate a stronger market reaction.

The Market's Blind Spot

Most discussion remains focused on whether enough fuel exists. Current evidence suggests that it does. A more useful question is how much resilience remains once inventories are depleted. Europe's aviation fuel market is not becoming structurally undersupplied. It is becoming increasingly dependent on uninterrupted execution across the supply chain. That is a subtle shift, but one with significant consequences when volatility returns.

Marina Lubimova

Marina Lubimova