Marina Lubimova

Marina Lubimova

memory manufacturers were valued as cyclical suppliers tied to PC and smartphone demand. Today, investors are increasingly treating them as builders of the infrastructure powering artificial intelligence.

The shift reflects a new reality. Every advanced AI accelerator requires enormous amounts of high-bandwidth memory (HBM), turning memory chips into one of the most strategically important components inside modern data centers. As a result, companies leading this segment are attracting capital that once flowed almost exclusively toward GPU designers.

Reuters reports that SK Hynix's U.S. offering was more than seven times oversubscribed, highlighting exceptionally strong institutional demand ahead of its Nasdaq debut.

Memory Has Become an AI Infrastructure Business

The AI boom is transforming the economics of the semiconductor industry. Cloud providers continue expanding AI infrastructure, requiring not only faster processors but also dramatically larger memory capacity. High-bandwidth memory has become a critical bottleneck for AI performance, placing suppliers such as SK Hynix at the center of the industry's fastest-growing segment.

The broader market reflects that transformation.

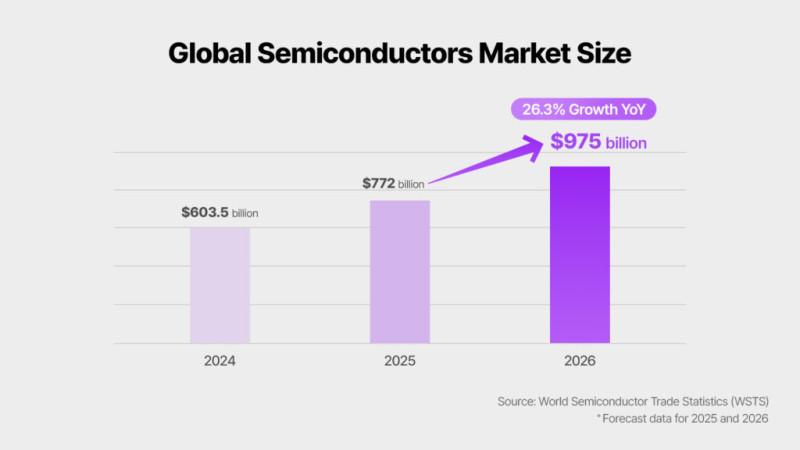

Figure 1. World Semiconductor Trade Statistics (WSTS) estimates the global semiconductor market will expand from $603.5 billion in 2024 to $772 billion in 2025, before reaching $975 billion in 2026, representing 26.3% annual growth.

The numbers illustrate that semiconductor growth is increasingly being driven by AI infrastructure rather than traditional consumer electronics cycles.

Nasdaq Opens a New Investor Base

The ADR is equally important from a capital-markets perspective. Although SK Hynix has long been one of the world's largest memory manufacturers, investing directly in Korean equities remains outside the mandate of many global institutional portfolios. A Nasdaq-listed ADR removes much of that friction, making the company significantly easier to access for U.S.-based investors.

According to Reuters, proceeds from the offering will help finance new fabrication facilities and advanced manufacturing equipment needed to support expanding AI memory production. At the same time, the listing could help reduce the valuation discount that has historically separated Korean semiconductor companies from comparable U.S. peers.

Rather than funding a new consumer product, the company is investing in additional production capacity for one of the fastest-growing hardware markets in the world.

The Market Is Rewarding Technology Leadership

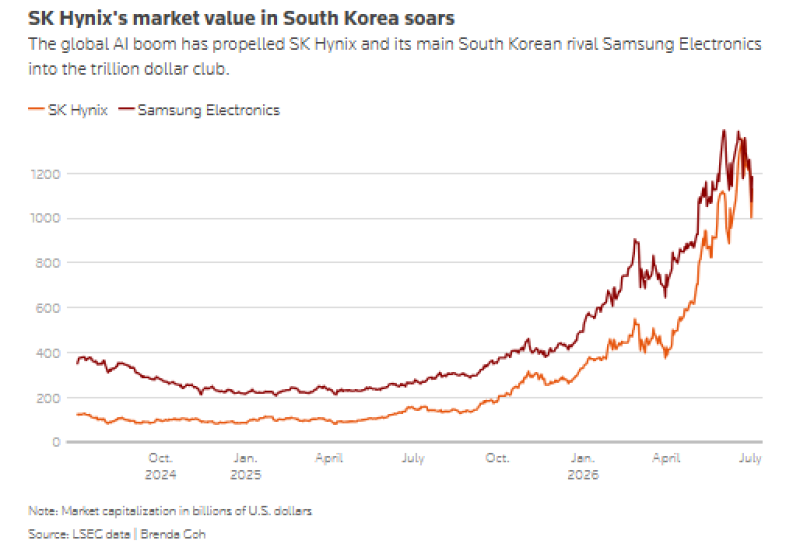

The change in investor sentiment is already visible in SK Hynix's valuation. While Samsung Electronics remains the world's largest memory manufacturer by volume, the market has increasingly rewarded companies with leadership in AI-focused products rather than overall production scale.

Figure 2. SK Hynix's market capitalization has risen sharply during the AI cycle, substantially narrowing the gap with Samsung Electronics as investors assign higher valuations to companies leading the HBM market.

That divergence reflects changing priorities. Instead of focusing primarily on commodity DRAM pricing, investors are placing greater emphasis on premium AI memory, long-term supply agreements and technological leadership. SK Hynix's position as a major supplier of HBM for advanced AI processors has made the company one of the clearest beneficiaries of this shift.

A Signal for the Semiconductor Sector

The ADR may ultimately prove more significant for the industry than for SK Hynix itself. If the listing succeeds, it will reinforce the idea that semiconductor companies occupying strategic positions in the AI supply chain can command valuation multiples traditionally reserved for software or platform businesses. It could also encourage additional Asian chipmakers to seek broader access to U.S. capital markets.

The flow of capital within technology is changing. Investors are no longer focusing exclusively on companies developing AI models. Increasingly, they are allocating capital to businesses supplying the hardware that makes those models possible.

Conclusion

The $149 ADR pricing is a reflection of a broader market transition rather than a standalone corporate event. Memory is no longer viewed solely as a cyclical commodity business. As AI infrastructure spending accelerates, advanced memory has become a strategic asset, and companies capable of delivering it are being valued accordingly.

Marina Lubimova

Marina Lubimova