Marina Lubimova

Marina Lubimova

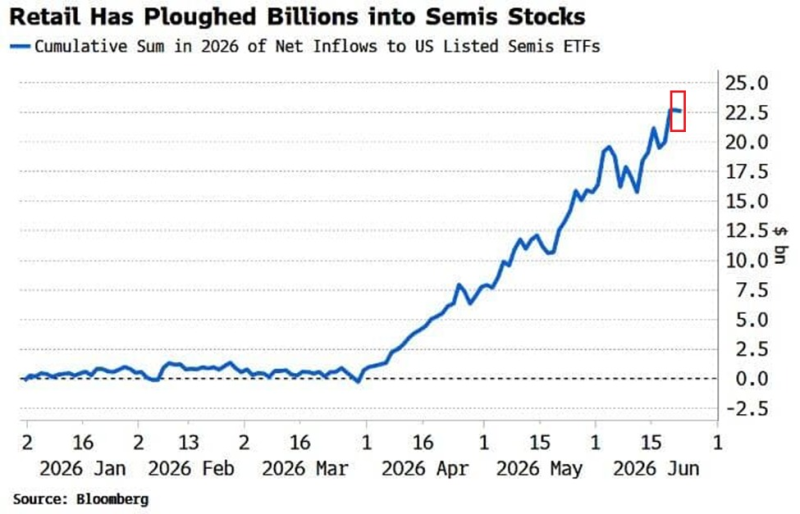

At first glance, the chart appears to illustrate another momentum-driven rally. Retail capital typically arrives after institutional investors have established positions, reinforcing an existing trend rather than creating a new one.

This cycle appears more complex. The inflows coincide with record semiconductor sales, accelerating AI infrastructure investment, and corporate earnings that continue to exceed expectations. Rather than simply reflecting optimism, passive capital is becoming an increasingly important mechanism through which capital is allocated across the semiconductor ecosystem.

The timing of the flows is notable. For most of January and February, cumulative inflows remained close to zero. Activity accelerated sharply during March before turning into a persistent upward trend throughout April and May. By late May, cumulative inflows had exceeded $22 billion, an unusually large figure for a single industry group within such a short period.

The significance lies less in the size of the inflows than in how that capital enters the market. Unlike previous technology cycles, investors are increasingly choosing broad semiconductor exposure instead of attempting to identify individual winners. The investment decision has shifted from company selection to ecosystem allocation.

Capital Has Shifted From Stock Picking to Ecosystem Exposure

Sector ETFs fundamentally change how capital reaches the semiconductor industry. Each new dollar entering these funds is automatically distributed across chip designers, foundries, memory manufacturers, equipment suppliers, networking companies, and analog semiconductor producers according to an index methodology.

Capital, therefore, follows benchmark construction rather than discretionary security selection. This broadens participation across the supply chain. Companies that might previously have attracted little retail attention increasingly benefit from systematic ETF allocations alongside industry leaders.

As passive ownership expands, incremental allocation begins influencing prices alongside earnings revisions and company-specific news. Index composition itself becomes an increasingly important pricing variable. This represents a structural change in how the market finances AI infrastructure.

Revenue Growth Is Catching Up With Valuations

Rapid ETF inflows would normally raise concerns if industry fundamentals were deteriorating. Instead, operational performance continues to strengthen.

According to the Semiconductor Industry Association, global semiconductor sales reached $110.5 billion in April 2026, representing:

- 11% month-over-month growth

- 93.9% year-over-year growth

- the 14th consecutive monthly increase in global sales.

| Period | Global Sales |

| April 2025 | $56.9B |

| March 2026 | $99.5B |

| April 2026 | $110.5B |

Regional performance illustrates how broad the expansion has become. Sales increased 115.8% across the Americas, 114.9% across Asia Pacific, 78.6% in China and 54.7% in Europe.

Growth is no longer concentrated in consumer electronics or smartphones. AI data centers, cloud infrastructure, enterprise computing, industrial automation and automotive electronics now contribute simultaneously to semiconductor demand.

The industry's forward outlook reinforces that picture. The World Semiconductor Trade Statistics organization projects global semiconductor revenue will approach $1.5 trillion during 2026, before exceeding $1.9 trillion in 2027. These forecasts suggest that current revenue growth is expected to continue rather than peak.

AI Infrastructure Is Already Visible in Financial Statements

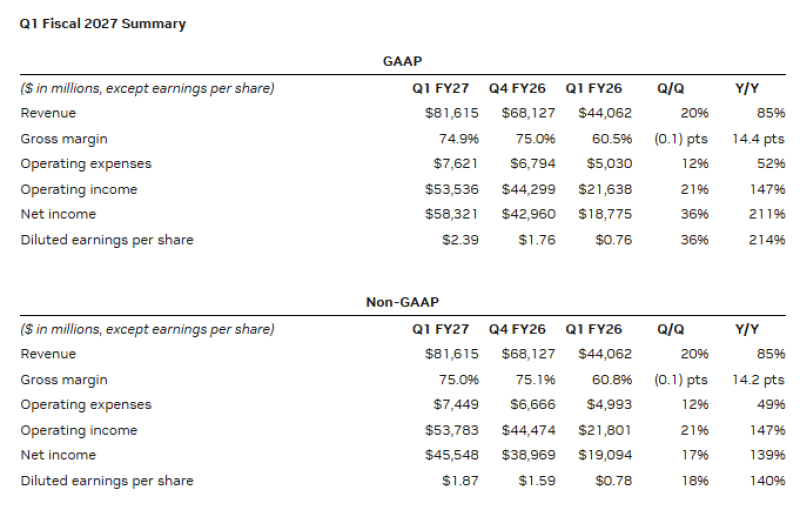

The industry's largest companies continue producing financial results consistent with that outlook. NVIDIA reported quarterly revenue of $81.6 billion, an increase of 85% compared with the same quarter a year earlier. Operating income climbed 147%, while diluted earnings per share increased from $0.76 to $2.39.

Results of this magnitude influence the market beyond a single company. Strong earnings reduce uncertainty surrounding future AI infrastructure spending, making it easier for investors to justify additional exposure to semiconductor ETFs.

Positive earnings reinforce ETF inflows, while ETF inflows support valuations across companies that participate in the broader semiconductor supply chain. Capital and fundamentals increasingly reinforce one another.

Index Flows Are Becoming a Pricing Variable

Semiconductor valuations are traditionally driven by earnings expectations, technology leadership and product cycles. Passive investment introduces another factor. As ETF ownership expands, allocation decisions increasingly influence price formation alongside traditional fundamental analysis.

Large inflows require funds to purchase underlying constituents regardless of short-term valuation differences between individual companies. That process creates persistent demand across the sector, reducing the importance of company-specific capital allocation decisions while increasing the influence of benchmark composition.

Semiconductors are gradually evolving from a collection of individual technology businesses into a single institutional allocation theme.

Capital Is Emerging as the Next Competitive Advantage

The next constraint facing the semiconductor industry may not be manufacturing capacity alone. Access to capital is becoming equally important. Higher equity valuations reduce financing costs, facilitate expansion, support research investment and strengthen balance sheets.

As passive capital continues entering semiconductor funds, the industry's ability to finance future production capacity improves alongside demand growth. Capital markets therefore become an additional competitive advantage rather than simply a reflection of existing business performance.

This creates a feedback mechanism in which industry growth attracts investment, while investment itself improves the industry's ability to expand.

Concentration, Not Demand, Is the Primary Vulnerability

Demand currently appears robust across nearly every major semiconductor segment. The larger risk lies elsewhere. Passive ownership naturally concentrates investor positioning. Should AI infrastructure spending moderate or hyperscale capital expenditures slow, ETF outflows would likely affect nearly every major semiconductor company simultaneously.

The same mechanism currently reinforcing the industry's performance could amplify downside volatility if expectations begin to reset. That does not undermine the long-term investment case. It simply changes where market risk originates.

Conclusion

The recent surge in semiconductor ETF inflows represents more than another period of retail enthusiasm. It reflects a broader change in how financial markets allocate capital to AI infrastructure. Investors are increasingly treating the semiconductor industry as a strategic allocation rather than a collection of individual stock opportunities.

At the same time, industry fundamentals continue supporting that shift through record sales, expanding AI demand and exceptionally strong corporate earnings. The significance of today's ETF inflows therefore extends well beyond short-term market sentiment.

If semiconductor revenue continues expanding along its current trajectory, passive investment flows may become one of the industry's most important structural tailwinds—not because they predict demand, but because they increasingly reinforce it.

Marina Lubimova

Marina Lubimova