Artem Voloskovets

Artem Voloskovets

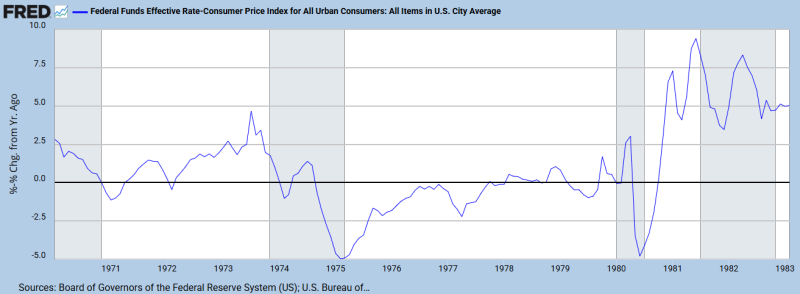

That combination stands out because gold's strongest advances have usually occurred when real rates were falling or below zero.

The long-term chart shows a consistent pattern. Gold performed best during periods when inflation exceeded policy rates, pushing real yields lower. This was visible during the inflation cycle of the 1970s, after the 2008 financial crisis, and during the pandemic-era easing cycle.

The current environment is different. Real rates remain positive, yet gold continues to make new highs.

Gold Is Outperforming Its Traditional Driver

The relationship between gold and real rates has not disappeared, but it has weakened. Since early 2024, gold has appreciated faster than changes in real yields would normally justify. While policy rates remain restrictive, demand for gold has continued to increase.

Recent trading data show gold gaining roughly 2% in a single session, pushing prices above $4,350 per ounce. That move suggests that factors beyond interest rates are influencing the market.

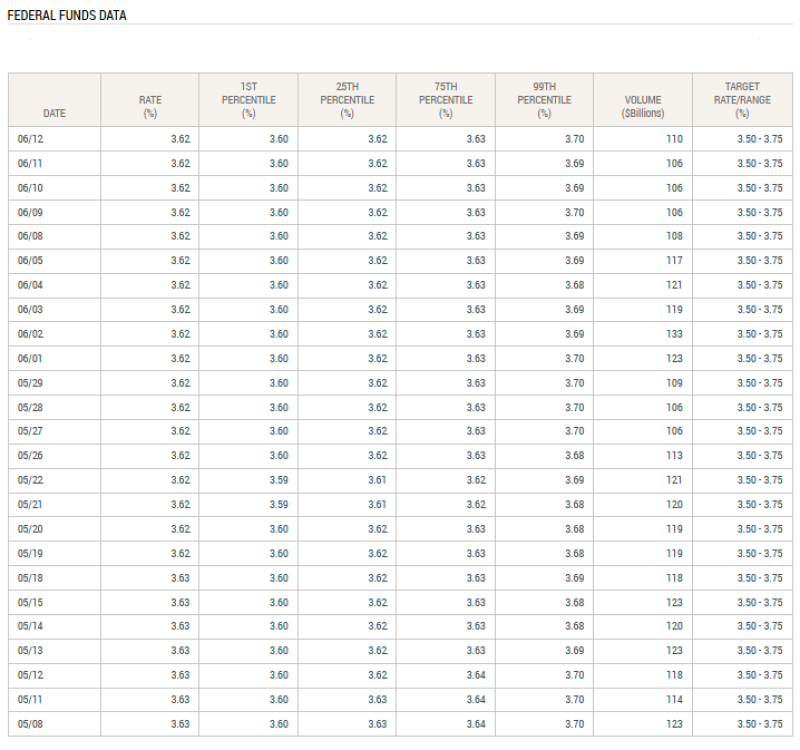

Real Rates Remain Elevated

Federal Reserve data show the Effective Federal Funds Rate holding near 3.62%.

Historically, this level would have supported cash and government bonds rather than gold. Positive real yields increase the return available from interest-bearing assets and typically reduce demand for non-yielding stores of value.

Yet gold continues to attract capital despite those conditions.

The Comparison With the 1970s

The closest historical parallel is not the level of rates but the divergence between policy settings and market expectations.

During the 1970s, real rates turned negative as inflation accelerated faster than the Federal Reserve responded. Gold rallied sharply throughout that period. Today's real rates remain positive, but the market appears to be pricing a future decline in inflation-adjusted returns rather than current conditions.

Gold Miners Tell a Different Story

Not every gold-related asset has followed bullion higher. One major mining stock recently fell from about $209 to $165, despite gold reaching record levels.

The divergence shows that equity investors remain focused on operating costs, production growth and company-specific risks rather than the metal price alone. Historically, sustained increases in gold prices have eventually improved mining margins, but the adjustment is rarely immediate.

What the Data Show

The current setup differs from most previous gold rallies.

- Gold trades above $4,350.

- Effective Fed Funds remain near 3.62%.

- Real rates are still positive.

- Gold mining equities have not fully confirmed the move.

Taken together, the data suggest that gold is responding less to current monetary conditions and more to expectations about future ones. Whether those expectations prove correct will determine if the rally continues through the second half of 2026.

Artem Voloskovets

Artem Voloskovets